MacroeconomicsUK

16 March 2026

As governments continue to ignore the social and environmental harms of growth, they may find it more difficult to avoid the reality that growth is becoming increasingly hard to come by.

The impacts on environmental degradation and socio-economic inequality detailed in the first blog in this series ought to remain front and centre of any critical analysis of economic growth, but they are not where the discussion ends. Approaching from a different angle, more and more economists and researchers have also been exploring the question: what level of growth is even possible in so-called ‘developed’ economies of the Global North, in the current historical context? In other words, added to critiques of the desirability of growth, this is a question around the feasibility of growth.

Many people will be familiar with the simplistic but effective argument that you can’t have infinite growth on a planet of finite resources. There is mounting evidence - as we move further into the twenty-first century - that even many governments who discount the negative environmental and social impacts of growth may have to face the reality that the high levels of growth seen in the past are unlikely to return. Accordingly, economic policy must adapt to meet social needs in this new context. The causes of dwindling growth are not reducible to resource scarcity - though it plays a role - but much more broader and complex. A few of the key factors are discussed here.

GDP measures the total monetary value of all goods and services produced within a country across a given time period. Figure 1 displays the UK’s GDP growth rate over the period 1949-2020. As shown by the dotted line, there is a long term downward trend in growth rates, despite major fluctuations reflective of the boom and bust cycles of capitalist economies. Throughout the 1950s to the 1980s, GDP growth frequently topped 4%, 5%, and even 6% on occasion. From the 1990s to the 2010s, growth has averaged much lower than this. Notably, the 2008 global financial crisis brought a significant reduction in GDP, followed by an even larger one in 2020 due to the covid-19 pandemic. Rebound from this unprecedented scenario in 2021 led to a very high growth rate of 8.6%, which has since settled back down at 0.4% in 2023 and 0.9% in 2024.

So what factors are behind this long-term downward trend in growth since the mid-twentieth century?

Figure 1: UK annual GDP growth, 1949-2020. Source: Wikimedia Commons (2021)

One huge part of the picture is the loss of relative environmental stability and the rapidly deteriorating condition of Earth’s critical ecological systems. Not only does growth come with environmental degradation, as discussed in the first blog in this series, but this environmental degradation then also places constraints on further growth, in a kind of feedback loop. On this point, the economist James Meadway has written:

“Collectively, humanity has seen 250 years of industrial, capitalist economic growth, with Britain as the very first country to see it on a sustained basis. That growth is now, in the first decades of this century, running hard into the fundamental barrier that is the end of the Holocene – the stable period in the earth’s geological and environmental history that modern humanity has lived in and, in the last few centuries, built an entire industrial civilisation on the foundations of.”

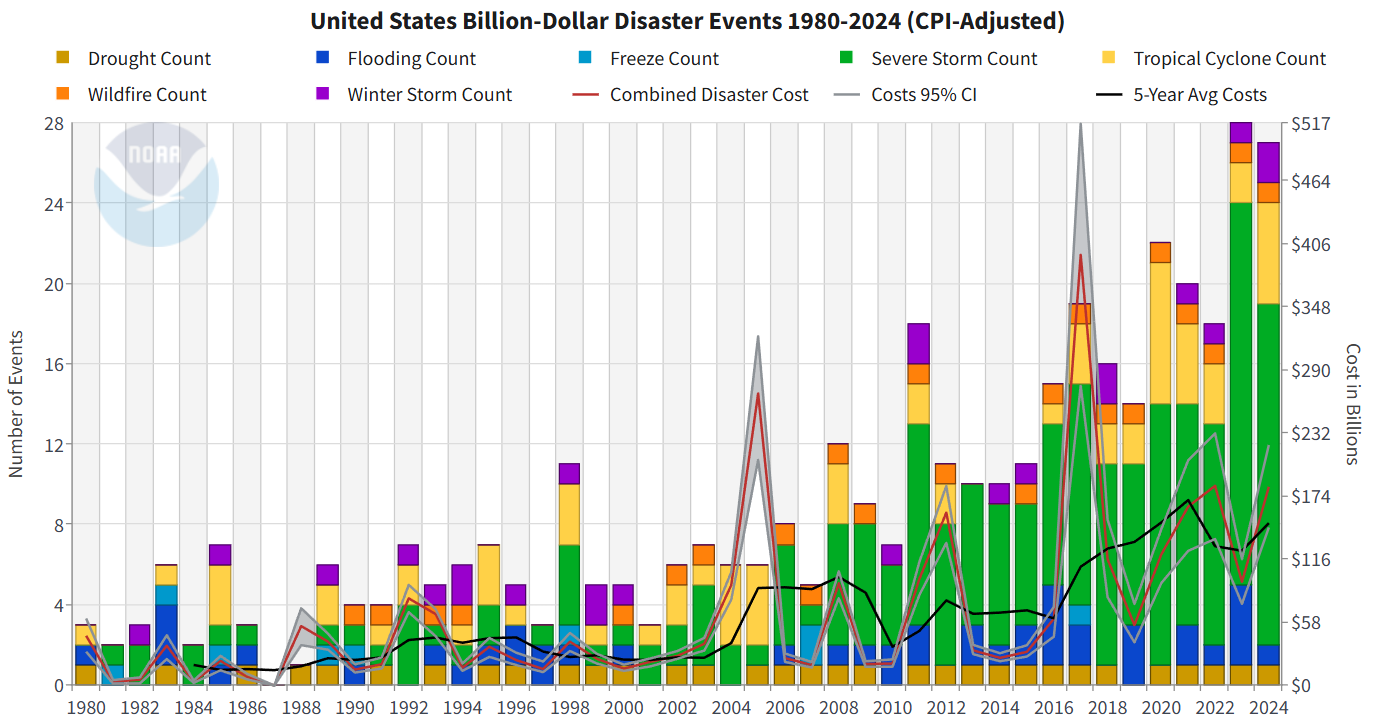

Climate breakdown exemplifies this point. Extreme weather events are becoming more frequent, and alongside tragic loss of life, these come with great economic cost. For example, figure 2 shows the rising number of extreme weather events in the US with damages totalling over $1 billion, between 1980-2024. Elsewhere, the 2022 floods in Pakistan were estimated to have caused economic losses as high as $40 billion. Extreme weather events disrupt economic output through damage to workers’ health, businesses, supply chains, infrastructure, and agriculture. A report published in January 2025 by the Institute and Faculty of Actuaries found that climate disasters could cause a 50% loss to global GDP between 2070 and 2090. At Positive Money, we have conducted research on the increasing extent to which extreme weather events are driving inflation, pushing up the price of basic goods and services, which is usually responded to with higher interest rates, which also place downwards pressure on GDP.

Figure 2: Extreme weather in the US with damages totalling over $1bn, 1980-2024. Source: NOAA National Centers for Environmental Information (NCEI) (2025).

Alongside relative environmental stability, another historically contingent factor upon which strong growth in the Global North previously relied concerns the energy-technological nexus. Many researchers have noted how the development of oil as an energy source, electricity, and road transport were fundamental to the high growth rates of the mid-twentieth century. Oil emerged as a form of ‘cheap energy’ due to its very favorable ratio of production cost to energy density. This ratio becomes less favourable as more easily accessible and plentiful oil deposits are depleted (e.g. in the North Sea, in the UK’s case).

While we urgently need to expedite transition towards renewable energy, this is unlikely to provide the same boon to economic growth as oil did. While the cost of renewable energy generation has been falling, private capital has not thrown its weight behind the likes of solar and wind energy, precisely because their rates of profit are low and unstable. This contrasts with the vast economic opportunities that oil opened up in the twentieth century, in combination with other technological developments. Alongside a currently non-existent renewable energy transition, governments are desperately searching for the next technological frontier of growth, with most eggs seemingly being placed in the dubious basket of artificial intelligence; itself an incredibly ecologically intensive technology, which carries further risks around job displacement and privacy.

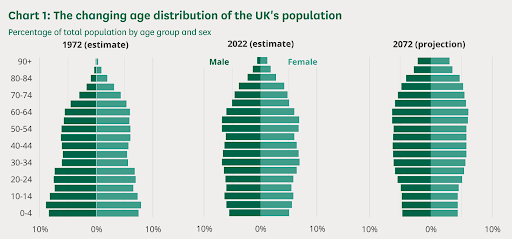

A third set of factors which will make growth increasingly harder to achieve in the Global North relates to demographics. Firstly, there is demographic ageing. Figure 3 shows the UK’s changing demographics over time, shifting from a much more youthful population in 1972, to a much older one by 2022, and even more so by 2072 (based on current projections). A 2013 report commissioned by the House of Lords notes that the UK’s ageing population - and higher ‘dependency ratio’ - will reduce GDP growth, as the proportion of retirees increases relative to the working population. On top of demographic ageing, there is the factor of migration. Alongside growth, another of the current UK government’s key objectives is reducing net migration. The Office for Budget Responsibility - whose analysis the Chancellor Rachel Reeves has ordained with such influence over her economic plans - has itself conducted research which finds that lower net migration will reduce the UK’s GDP.

Figure 3: The UK’s age demographics over time. Source: House of Commons Library (2024).

While the list could go on much further, a final factor important to mention here - which is likely to reduce growth in the coming years - is geopolitical instability. There is a seemingly growing consensus amongst governments across the world - including in the UK - that we are entering an era of increased geopolitical instability. This sentiment is reflected in the large increases in military spending happening in many countries, with the UK government committing to raising its spending to 2.5% of GDP by April 2027.

Russia’s war on Ukraine provides an example of how geopolitical conflicts can hold stark economic consequences internationally. Sanctions and disruptions to supply chains resulting from the war led to inflation in the UK - notably in energy prices - and a household incomes squeeze that has placed downward pressure on GDP growth. If we take the same view as so many current governments - that geopolitical instability is increasing - then we can expect to see further (and continuing) conflicts that have similar suppressing impacts on GDP in the UK and elsewhere. And it is not just the direct military side of geopolitical instability that reduces growth. Protectionist national economic agendas - which tend to proliferate in tense geopolitical environments - can also raise inflation and lower growth. A study by the National Institute of Economic and Social Research found that UK GDP could be reduced by up to 2.5% after three years of President Trump’s regime of tariffs.

So, even as most governments continue to ignore the damaging macro-scale impacts of growth on environmental sustainability and socio-economic inequality, it may become more difficult for those in the Global North specifically (such as the UK) to ignore the reality that growth is - and will be - increasingly hard to come by. Governments that continue to chase growth and promote it as the solution to economic and social problems are therefore likely to lose the support of electorates, much less meaningfully address the major crises of our time. What is needed are new economic policy visions and tools which fit the circumstances of the twenty-first century, sustaining and enhancing social and ecological wellbeing in a context without growth.

This is the second blog in a three part series, read the first on the social and environmental harms of growth here, and the third on the UK government’s confused model of growth here.

Sign-up to our mailing list for regular updates, or donate to support our work to redesign our economic system for social justice and a liveable planet.