Rethinking central bankingEU

16 March 2026

With inflation reaching its highest levels since the euro was introduced, ECB officials have been wary of a wage-price spiral. Yet it’s profits, not wages, that are the real culprits in today’s inflation story.

Last Thursday, the ECB raised its interest rates by half a percentage point, amounting to a cumulative three and a half percentage points since July. So far, ECB officials have used two main lines to justify their policy strategy.

The first is that facing an energy price shock, interest rates should be increased to avoid the de-anchoring of inflation expectations, as the latter would lead to a wage-price spiral. The second is that rates need to be increased so as to adjust demand to a new lower level of supply. The role of profits is nowhere to be found in either of these justifications. Instead, ECB officials have constantly warned about the role that wages and low unemployment play in adding inflationary pressures, even though the purchasing power of wages has been falling off a cliff.

One way to appreciate the role of profits in the current inflation surge is to examine the GDP deflator. The GDP deflator is the ratio of nominal GDP (value of final goods produced) to real GDP (volume of final goods produced). Contrary to the HICP, which is the measure of consumer prices that we usually refer to when talking about inflation, the GDP deflator only measures the changes in prices of final goods and services produced domestically.

Let’s illustrate how the GDP deflator works through extreme simplification. Imagine an economy where a single firm exists, which produces only one good. The price of this good is €150, comprising €50 of imported raw materials, €50 of wages and €50 of profits. This means that the nominal GDP of the economy is €100 (the sum of wages and profits). Now imagine that the price of the imported raw materials rises by €15 and that this increase gets passed onto the final price of the good, leaving nominal wages and profits unchanged. Since the final price of the good has changed by 10%, so has the HICP. But since neither wages nor profits have changed, and hence the nominal GDP has remained the same, the GDP deflator hasn’t changed.

The ECB fears a situation in which, facing the situation above, wage and profit earners try to increase their incomes so as to maintain their purchasing power intact or even try to increase it. This would be the so-called ‘second-round effects’ of inflation, which could lead to a wage-price spiral if left unchecked, or so the story goes.

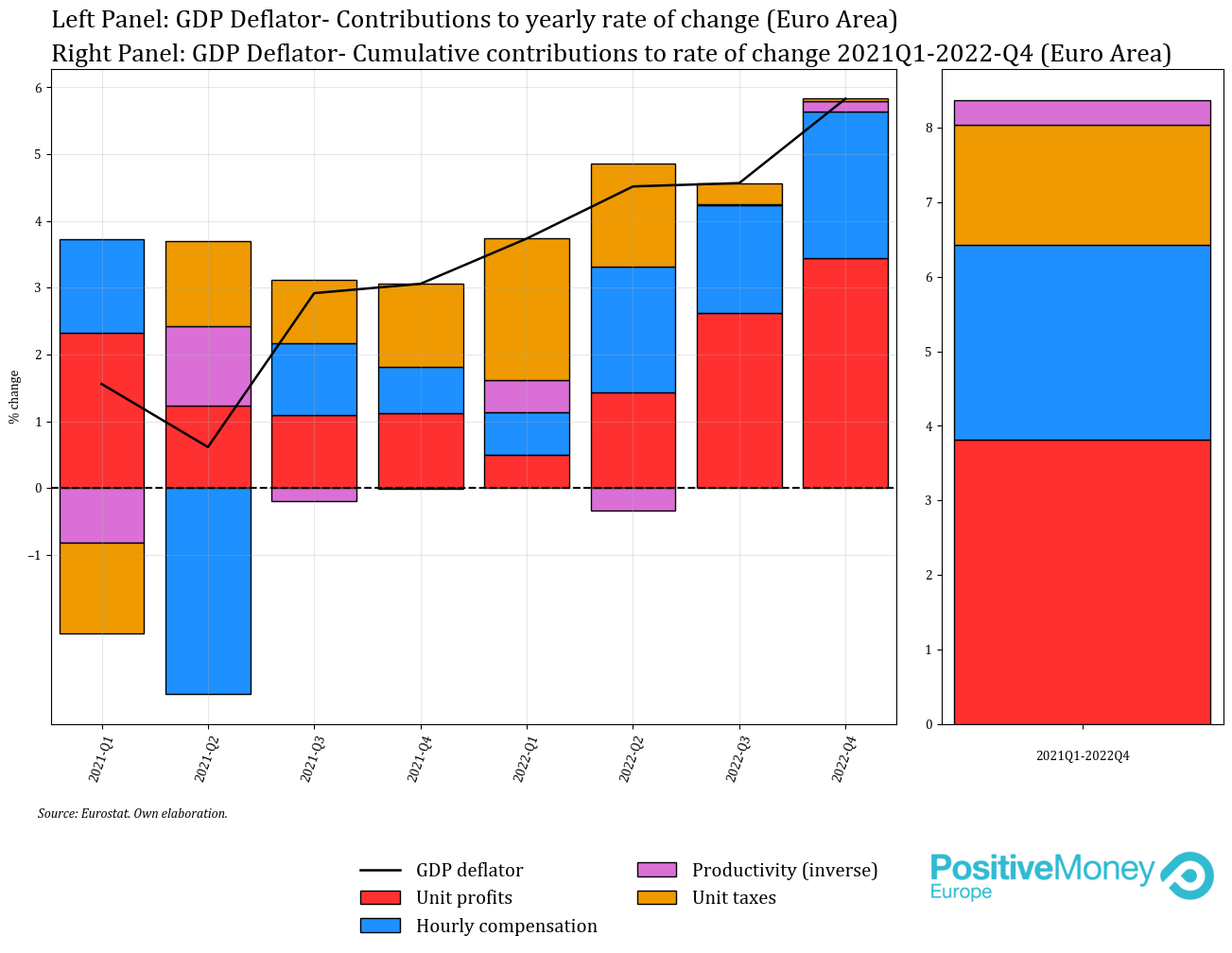

If this is the main concern of ECB officials, it begs the question, how have wages and profits evolved in the euro area? This can be examined by decomposing the GDP deflator into unit profits, hourly employee compensation, productivity, and taxes minus subsidies [1]. Once we apply this decomposition, we can examine which factors have added pressure to domestic prices.

The graph below shows that between the first quarter of 2021, when the HICP started to accelerate, and the last quarter of 2022, the percentage change of the GDP deflator was 8.37%. Half of this change was due to changes in profits, while changes in hourly compensation account for around 30% (right-hand panel). The last two quarters of 2022 are particularly worrying, as the contribution of profits took off, putting extra pressure on domestic prices (left-hand panel).

This shows that the constant talk about wages by ECB officials is entirely misplaced. The reality is that rising profit margins have added additional inflationary pressure in the euro area, at the expense of workers, who have seen the purchasing power of their wages erode.

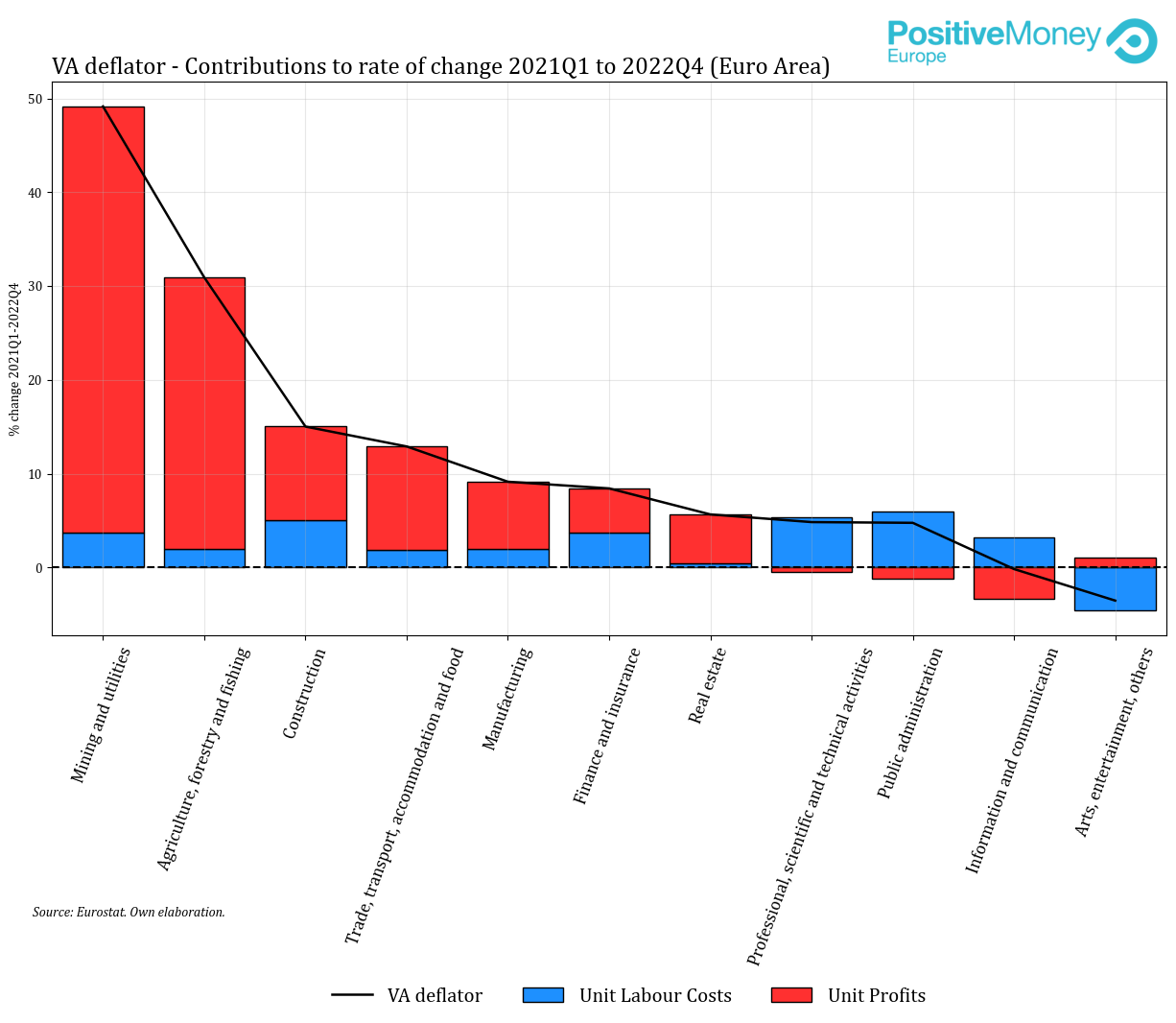

We can also examine how different sectors’ profits have behaved during this high inflation period by decomposing each sector’s deflator between wages and profits [2]. In the graph below we can observe the contribution of each one of them to the rate of change of the price deflator between the first quarter of 2021 and the last quarter of 2022. The sectors related to food and energy—the goods that have seen the largest increase in prices—are the ones that have increased their unit profits the most.

What we observe resembles the mechanism that Isabella Weber and coauthors have identified in the US [3]. There’s an increase in the prices of upstream sector goods, meaning goods that are used for production across other sectors (e.g., electricity). As these goods face international disruptions, domestic producers use this situation as a smokescreen to pump up their profit margins, putting extra pressure on prices. This price increase cascades to downstream sectors—meaning the sectors that use these goods for their own production processes—which experience an increase in costs, and, depending on their market power, are able to further increase their profit margins, leading to rising prices down the line. This ends up resulting in broad-based inflation.

Not all sectors, nor all firms within sectors, will be able to benefit from this environment. For example, certain sectors (e.g. information and communication) have experienced a decrease in profits. Furthermore, smaller firms with less pricing power are less capable of using this situation to increase their profit margins, even if their sector is increasing its profit margins on the aggregate.

In the face of the increasing prices of imported goods, higher interest rates are aimed at ensuring that the spiralling increase in prices does not take place. This is achieved by creating unfavourable labour market conditions so that workers are willing to accept a loss of purchasing power. This is clearly reflected in the words of the most outspoken central bankers, such as the governor of the Dutch central bank, Klaas Knot, who said the quiet part out loud when he asked rhetorically, “why would workers settle for a hit to their purchasing power in current labour market conditions?”.

Last Thursday, profit margins were mentioned for the first time in the ECB Governing Council press meeting. Lagarde argued that there should be a “proper burden sharing of what is a quasi-tax”, the latter referring to the dramatic surge of prices in imported goods. Subsequently, she argued that what ECB officials are concerned about is—regardless of burden sharing—whether this price shock would be followed up by a spiralling increase in prices.

The problem with this framing is that it blatantly sidesteps the distributive role that monetary policy plays in all this by placing the burden of adjustment on the back of workers. While we welcome their newfound recognition of the role that profits play, their policy strategy remains the same. This shows to what extent conventional monetary policy is class-biased. Burden-sharing and monetary policy cannot be detached from one another, as it is precisely monetary policy that creates the playing field on which burden-sharing will be decided, and it does so by increasing unemployment.

The tragic irony is that it is undoubtedly the big corporations which have contributed most to rising prices by increasing their profit margins who will be able to navigate the adverse effects that increased interest rates will cause. On the other hand, workers and small businesses—the ones that have seen their purchasing power deteriorate—will continue to face hardship.

When we put aside the fearmongering of a wage-price spiral hiding on the horizon, it becomes clear that profits are a far bigger driver of today’s inflation. Yet, despite all the innovations that come about in monetary policy whenever the financial sector faces a crisis, the response to inflation—regardless of its sources—remains the draconian approach of throwing people into unemployment. Lagarde said that burden sharing required a societal debate. We agree, this debate starts by questioning the role of the ECB.

[1] Since: P x Y = EC + GOS + TAX. Where P is the GDP deflator, Y is real GDP, EC is nominal employee compensation, GOS is gross operating surplus and mixed-income, and TAX is taxes minus subsidies. By dividing both sides by real GDP, the GDP deflator can be decomposed into unitary labour costs, unit profits, and unit taxes. Finally, unitary labour costs can be broken down into hourly employee compensation and productivity. While gross operating surplus and mixed-income has some downsides as a measure of profits, as it includes self-employed people’s income and the consumption of fixed capital, it is the best proxy for profits in the national accounts.

[2] The sectoral decomposition follows the same pattern as the GDP deflator. The value-added in a sector can be divided into profits and wages.

[3] See Weber, I. M., & Wasner, E. (2023). Sellers’ Inflation, Profits and Conflict: Why can Large Firms Hike Prices in an Emergency? and Weber, I. M., Jauregui, J. L., Teixeira, L., & Nassif Pires, L. (2022). Inflation in times of overlapping emergencies: Systemically significant prices from an input-output perspective.