UKEU

18 February 2026

It is looking increasingly likely that the Autumn budget will include some changes to the way property is taxed. Instead of focussing plainly on how to raise additional revenue, the government should use this opportunity to dismantle parts of the tax regime which incentivise speculation and financialisation in the property market, as this is key to tackling the affordability crisis in the housing market.

For far too long, the uniquely regressive council tax system, in which it is the occupier rather than the owner who pays, has been the cornerstone of property taxation. Council tax bands are based on valuations made in 1991, and since property values in London and the South have grown far more than in other parts of the country, this has led to a situation in which the occupier of an average home in Hartlepool pays more in council tax than that of a luxury mansion in Westminster. The current discussions surrounding the potential shake-up of the property tax regime are therefore more than welcome, and long overdue.

As we all know, the UK is facing a housing crisis of dystopian proportions. House prices and rents continue to outpace the growth of incomes while the number of people who are homeless, in temporary accommodation, or forced to pay unaffordable private rents continues to soar. In this context, instead of focusing solely on how to raise tax revenue, it is absolutely essential that property tax reform is designed to achieve housing affordability, stabilisation of property values, and a reduction in the obscene levels of speculation and financialisation in the housing market.

Housing currently serves two functions in our economy - that of a home and shelter, and as a vehicle for accumulating wealth. One of the key reasons the housing crisis has reached the catastrophic scale we see today is because government policy has continuously contributed to propping up housing as a speculative asset, thus reducing its availability and accessibility to fulfil housing needs.

This is evident across different areas of policy. For example, the continued shift from supply-side housing subsidies to demand-side subsidies - instead of building genuinely affordable and publicly owned social housing, the government has helped struggling households pay their excruciatingly expensive private rental costs. The result has been a continuous decline in social housing provision, and the government will have transferred £70bn straight into the pockets of landlords between 2021 and 2026, further propping up unaffordable private rents.

However, it is not only through housing policy that successive governments have turned our homes into assets. Tax policy has also played a hugely significant role in terms of driving speculative demand for properties, which in turn is a key contributor to the continuously worsening affordability crisis. Reforming the way property is taxed is therefore a key lever for tackling the housing crisis.

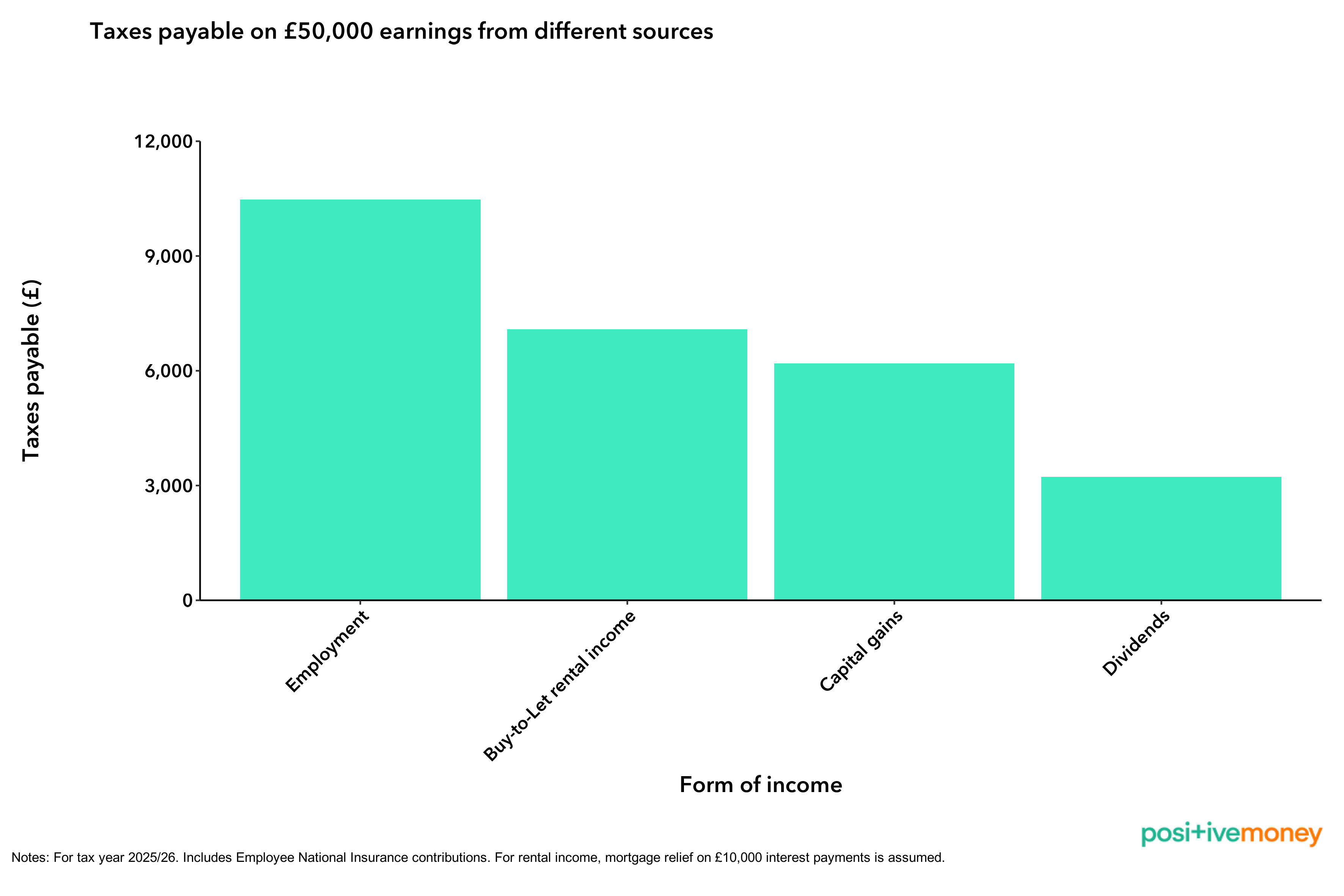

It is certainly the case that the current property tax regime does not sufficiently tax the wealthy. At the same time, it penalises renters, as income from employment is taxed at higher rates than income received through the ownership of assets such as property. The less property wealth, rental income, or capital gains from property speculation are taxed, the more pressure there is to tax income from work. The current imbalance of taxing income from work at higher rates than income from wealth is also economically inefficient, as it discourages productive activity and incentivises speculation and rentierism, acting as a drag on the wider economy.

The structure of the tax system therefore plays an important role in how it channels economic activity. Lower rates of tax on unearned income makes speculative investment comparably more attractive than productive activities. It incentivises both individuals and businesses to engage in financial rather than productive economic activities, and, as a result, more money flows into property speculation than into the real economy, such as manufacturing or services.

Instead of focusing on protecting renters and improving affordability, successive governments have centred their housing policy on boosting homeownership. The result has been a continued increase in the demand to buy property, which is evidently clear from an analysis of bank lending data, as 54% of all lending by banks is now held in mortgages, up from around 40% fifteen years ago.

Research has shown that reducing investment demand for buying property is among the key issues that must be addressed if we are serious about tackling the housing crisis. Although there are various ways in which this can be done, including rent controls and credit policy, changes to some of the highly skewed tax privileges which property investors benefit from are absolutely vital. A well-designed reform of property tax would be able to shift the burden of payment from poorer to wealthier households, while simultaneously incentivising more efficient use of the housing stock.

There are various parts of the tax system that contribute to the housing and affordability crisis by making property a uniquely lucrative investment due to the low tax rates and exemptions property speculators, home-owners, and landlords enjoy.

First, the council tax system is now highly regressive as taxes are not proportional to the values of the property, and in the case of rentals, the cost of paying the tax falls on the tenants rather than the owner of the property. Furthermore, rental income, for no valid economic reason, is completely exempt from National Insurance contributions, meaning it’s taxed at a lower rate than income from employment.

This incentivises the purchasing of properties with the purpose of letting them out and benefitting from the low tax rates on rental income, to such a degree that there are over 2 million Buy-to-Let mortgages in the UK. Not only are the tenants in the unlucky position of having to cough up unaffordable rents while paying their landlord’s mortgage, but on top of this, they also pay higher rates of tax than their landlords!

Capital gains tax is a tax that is levied on the increase in value of an asset when it is sold. Any capital gains received from speculation in the property market is taxed at much lower rates than income from work, while also benefitting from the annual capital gains tax-free allowance of £3,000. Furthermore, the sale of primary homes is completely exempt from any tax on capital gains, which was worth a whopping £32 billion in 2023/24. Property wealth benefits from an additional exemption when inherited, as up to £500,000 of property wealth per person can be inherited by direct descendants without incurring any inheritance tax at all.

It would be possible to drastically reduce the financialisation of the housing market and improve affordability with just a few changes to the property tax regime. Taxing property proportionately or progressively in accordance with the value of the property would drastically disincentive the purchasing of homes as investments. It would also reduce the buying of second or third homes, often used only a few weeks per year and otherwise sitting empty.

Even minor changes to the council tax for second homes in Wales reduced home prices by 12%, so a national, more comprehensive strategy to replace the council tax with a proportional property tax would have even more considerable impacts for affordability. Modelling shows that an annual tax set at 0.48% of the value of the property would release 280,000 empty, unbuilt, or second homes onto the market - a significant shift towards aligning housing policy closer with the goals of fulfilling housing needs rather than satisfying investor demand.

Furthermore, taxing capital gains on the profits of the sale of a property at the same, or higher, rates as income from employment would also reduce the appeal of property as speculative assets, thus making them more available to be used as homes. The privileged treatment of rental income, on which no National Insurance is paid, should also be rectified. This would reduce the appeal of landlordism by decreasing the expected rental yield of properties, thus reducing their attractiveness as a speculative asset. Equalising taxation of income from wealth with income from work would therefore go a long way towards improving both affordability in the housing market and fairness in the tax system as a whole.

Naturally, tax policy reform is not by itself sufficient to solve all the issues related to the housing crisis, but it’s a key lever for ensuring that speculative demand does not continue to worsen affordability. Much more needs to be done, particularly in terms of building more social housing and improving renters’ rights.

However, it is clear that the government’s current strategy of solely focusing on increasing supply is wholly ineffective, and if it is serious about tackling the housing crisis, it must address the skewed incentives in the tax regime. Furthermore, tax reform could also make sure that housing policy is consistent with ecological goals, as it could ensure a much more efficient use of the housing stock by disincentivising holding empty homes as investments or high levels of under-occupation.

Changing how we tax property, and income derived from property, could therefore have a transformative impact not just in terms of stabilising the asset-price bubble in the property market and improving affordability, but also in ensuring that we use our housing stock sustainably and effectively, to ultimately help us turn our houses back into homes - not financial assets.

Sign-up to our mailing list for regular updates, or donate to support our work to redesign our economic system for a better world and a healthy planet.