Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

10 December 2013

Is Bank of England actually capable of dealing with asset bubbles?

House prices in UK are rising at nearly ten times the pace of average earnings.

House prices in UK are rising at nearly ten times the pace of average earnings. The Bank of England has already scrapped its Funding for Lending scheme for mortgages, in order to cool the housing markets.

Chancellor George Osborne insisted in the Autumn Statement that the Coalition would “avoid the mistakes of the last decade” and argued that the Bank of England would take action to deal with asset bubbles if they threaten our stability.

Now also the Bank of England’s Governor Mark Carney has admitted he is concerned about the “potential” for a bubble in the UK housing market, and said that the Bank of England will act to stop housing market growing at ‘warp speed’, reported the Telegraph 9th Dec 2013

But how capable is Bank of England of taking action, actually?

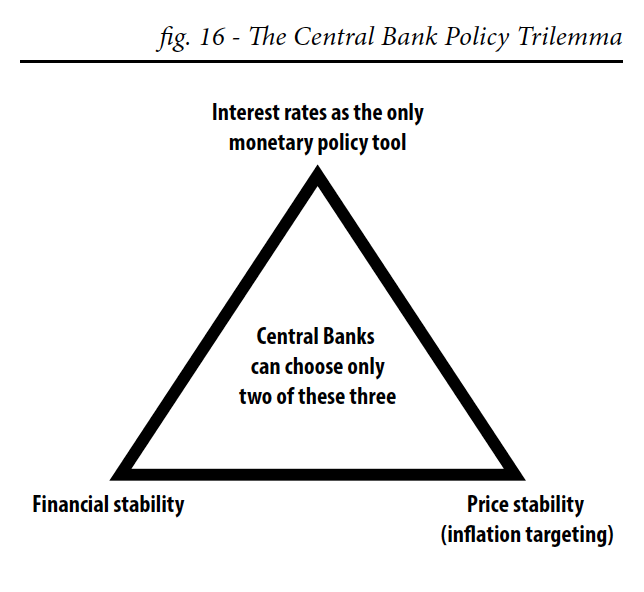

Before the crisis the Bank of England had one policy lever: interest rates, but two targets: price stability and financial stability. While the countercyclical capital ratios that have been brought in since the crisis to prevent excessive bank lending may be useful in preventing asset price bubbles, they are less effective at constraining the level of private debt to a safe level given current incomes.

The use of interest rates as the sole monetary policy tool brings the central bank’s two mandates – price stability and financial stability – into conflict with each other. By using interest rates to attempt to maintain price stability, the central bank forfeits its ability to meet its objective of maintaining financial stability, as a low interest rate can incentivise speculative behaviour. Essentially, the central bank has been asked to maintain aggregate demand at a level which maximises long term economic output, but has not been given the tools that allow it to achieve this goal. In the run up to the financial crisis, the goals of monetary policy were incompatible with the central bank’s toolset, which only consisted of interest rates.

This leads to a trilemma for the central bank in the long term – it can only choose two out of three options from: using interest rates as a policy tool, the price stability mandate, the financial stability mandate (figure 16).

For example, if the central bank wants to control prices (inflation) using interest rates, then it must give up its ability to control financial stability in the long term, unless it happens that price stability and financial stability require exactly the same interest rate at all times.

Alternatively, the central bank may choose to use interest rates to maintain financial stability, but this is likely to lead to fluctuations in the inflation rate, as interest rates may need to increased to restrict bank lending for asset purchases, even as borrowing and spending in the real economy remains stable (and therefore requires a stable interest rate).

Finally, if the central bank wants to maintain both price stability and financial stability, but only has the interest rate as a policy tool then this becomes impossible, as the central bank has two targets but only one tool. Consequently, unless the maintenance of financial stability and price stability require the same interest rate, the central bank will be forced into choosing an interest rate that allows it to hit one target or another, or a ‘compromise’ that hits neither target.

For example, take the case of a potential asset price bubble, driven by bank lending for asset purchases. The central bank could respond by increasing interest rates to discourage further borrowing. Alternatively, given the negative effect of high interest rates on investment and the ineffectiveness and long and variable lags in conventional monetary policy, the central bank could use a tool other than the interest rate limit bank lending. However, if it did mange to reduce lending in this way, the resulting slowdown in spending (due to a smaller wealth effect and lower lending for GDP related transactions) would slow growth if implemented on its own. Consequently, the central bank may be unwilling to act to slow the unsustainable growth in asset prices.

In contrast, if the Bank of England was able to increase spending while at the same time increasing interest rates to burst the asset price bubble (or some other policy restricting bank lending, such as an increase in countercyclical capital ratios) then asset prices could be deflated without negatively affecting income or growth. This could be achieved through Sovereign Money Creation – a process which involves allowing the Bank of England to create money, which would be granted to the government and spent into the real (non-financial) economy – outlined in this paper.

By increasing Sovereign Money Creation (SMC) at the same time as bank lending is reduced (due to interest rate/capital ratio increases), the central bank replaces unsustainable private spending fuelled by increasing assets prices and private debt-to-income ratios with growth fuelled by an increase in spending (that doesn’t rely on increasing private debt). This allows the private sector to pay down debt to a more sustainable debt-to-income ratio without sparking a recession. Consequently, the use of SMC during downturns makes a future recession less rather than more likely, whereas not using SMC and instead lowering interest rates may make a financial crisis more likely. Once the private sector has reached its desired debt-to-income ratio, borrowing can increase, SMC can be reduced, and private sector led growth can return.

An important benefit of using Sovereign Money Creation in addition to current monetary policy tools is that SMC allows the central bank to fulfil its democratically mandated targets to keep output at potential without increasing inflation or creating financial instability. With the addition of SMC to the central bank toolset, policymakers no longer face a trade-off between financial stability and price stability/economic growth.

(The text above is an extract from the paper ‘Sovereign Money Creation: Paving the Way for a Sustainable Recovery’; Download Here (Free, PDF, 60 pages) )