Finance and DemocracyUK

30 April 2026

Trump wants tariffs on countries that ‘move away from’ the dollar - but why is the dollar used internationally in the first place, and why does that matter? This first blog in our series of three on dollar dominance looks at the fundamentals.

In all the news coverage of Trump recently, you'll have seen him calling for trade tariffs on Global South countries “trying to move away from the dollar”. Or maybe you’ve heard phrases like ‘the almighty dollar’ or economists talk about concepts like ‘dollar dominance’. But, what does this all mean? If the dollar is US currency, how does it have power on the international stage? How did it become so powerful, and why does it matter what other countries do with it? In the first of our series of three explainer blogs, let’s look at exactly how and why the dollar is used globally, and how it came to be so dominant in the international economy.

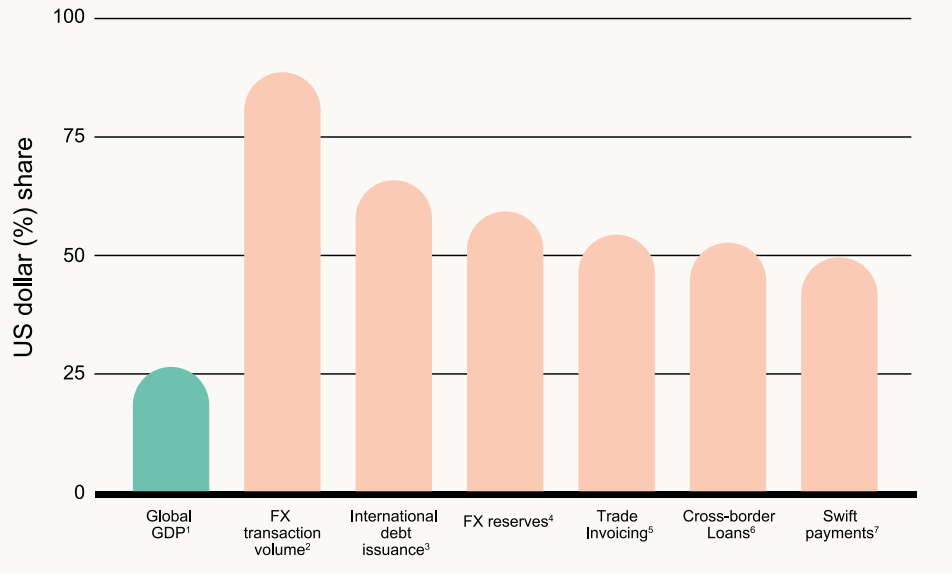

Yes, many countries have their own national currencies, like the Japanese yen, or a shared regional currency, like the euro. But in a global economy, they also need to buy goods and services from other countries which use different currencies. To enable this cross-border trade, banks and financial institutions mostly work by converting each currency into a common currency. The most widely used common currency, accounting for over 80% of global trade finance, is the US dollar.

Figure 1: The global role of the US dollar

Source: Beyond Dollar Dominance (2024), data sources in report

So, much like how someone from Germany and someone from China can have a conversation together by speaking English, someone from Kenya can buy something from Indonesia because their money is converted to dollars. In this way (as one economist puts it): “the dollar is to international finance what the English language is to international communication”. This is one piece of the puzzle as to why the dollar is so dominant globally.

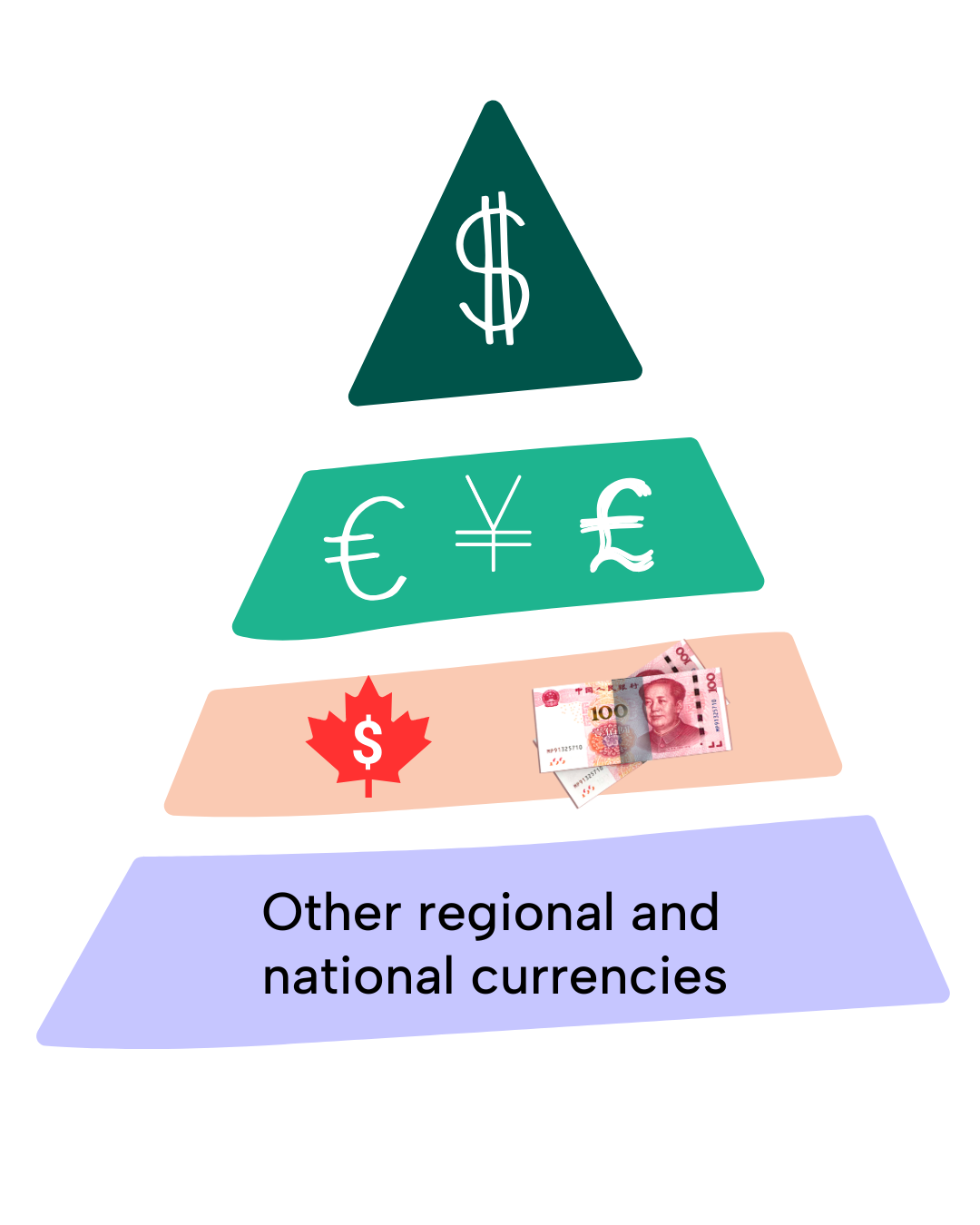

Unfortunately, getting access to dollars isn’t quite as easy as switching the language you’re speaking. You might be familiar with the process of changing your money before going on holiday at a bureau de change, and how the ‘exchange rate’ for you might be better or worse depending on the currency you have, and want to change into. If you’re based in the UK, or somewhere else with a ‘stronger’ currency, you usually get a good deal when you change your money. This can be illustrated in the global currency hierarchy.

Figure 2: The global currency hierarchy

However, if you want to buy dollars with your own currency when you're from a country where the currency is less ‘strong’ or desirable (lower down the currency hierarchy), you’ll find it’s expensive, and you won’t get such a good deal. This is because not many people want to trade their (high-value, ‘strong’) dollars for currencies that are perceived as more risky (likely to see sudden losses in value) to hold than the more ‘stable’ dollar, resulting in low demand and a lack of liquidity. This lack of demand for ‘weaker’ and ‘riskier’ currencies is what reflects onto their exchange rate, and what makes changing them for dollars less of a good deal.

Zooming out to think of this on a national scale, while these countries may not have currencies perceived as desirable, what many of them do have, that is desirable internationally, is natural resources. Therefore, what they often end up having to do is exploit these natural resources and sell them on international markets to get dollars in return instead.

If a country can’t earn enough dollars through exports, or attract enough international investment, their other option is loans. This most often means getting large, private, mostly Global North-based banks to loan them dollars at expensive interest rates. The interest rates are high as major credit rating agencies perceive many Global South countries as risky (although this is very questionable given many Global South countries are now strong economies globally). In economic crisis situations, countries often borrow instead from international multilateral financial institutions like the International Monetary Fund (IMF) or the World Bank (WB). These crisis situations can often be caused by struggling to make repayments to private creditors for dollar-denominated debts, as the high interest rates become so unsustainable. This is dollar dominance in a nutshell.

None of the options outlined above are desirable (we’ll go into more detail about them in our next blog), but there are three main reasons why countries have to go to such lengths to acquire dollars.

Firstly, without dollars, their ability to buy, or ‘import’, from other countries is severely limited. This is because essentials like food and energy are often traded in dollars, and countries across the world rely on their ability to import these for their survival.

Secondly, they also need dollars to pay off any international debts they have. Because of the US' status as the world’s largest economy, and historical context (see below), a huge amount of international loans have been issued in dollars. That’s the case for loans directly from the US, from international organisations (still headed up by the US in their governance structures) like the IMF or World Bank, or from private Global North creditors. That debt issued in dollars (or ‘dollar-denominated’ debt) has to be repaid in dollars too, and it accounts for 64% of world debt overall.

Finally, and perhaps a little more complex, is that central banks across the world need dollars to keep in reserve. Given how key a country’s ability to import is, central banks are motivated to have dollars in their reserves to ensure import needs are taken care of, both today and in the future. But reserves can also be used to keep their currency more stable in times of crisis. To do this, central banks hold foreign exchange reserves, most often in dollars as they’re widely available and easily traded, which they can buy and sell on the foreign exchange markets to stabilise the value of their currency. This is why dollar assets (including Treasury bonds, dollar deposits, and other financial instruments) make up about 59% of global foreign currency reserves.

All of this results in a bit of a chicken and egg situation: countries want dollars because it’s viewed as a stable, reliable currency that’s used very widely, and easy to buy and sell. So, they proceed to accumulate dollar reserves. But so many countries having such a demand for dollars, and so many having dollars and dollar-denominated assets in reserve, is part of what makes it so easy to buy dollars - because there’s lots of them (a.k.a. the dollar is abundant, or ‘liquid’ in the global economy). This further means its status as a widely used and stable currency keeps getting cemented. In economics, the way this situation reinforces itself is called ‘network effects’, and what it means is that countries are in a large part trapped in this status quo of chasing dollars for their economic survival. That is, trapped in a world of dollar dominance.

It’s all to do with history, the economic might of the US, and how our current International Monetary and Financial System (IMFS) has been set up. We can think of the IMFS as a combination of all the payments infrastructure, institutions, international regulation and power dynamics that underpin how money and finance flows across the world.

After World War Two, Europe and the US got together to create a new financial and monetary framework called the Bretton Woods system. The centrality of the US and the dollar was crucial in how everything was set up, with most major currencies ‘pegged’ to the dollar, and dollars exchangeable for gold. It’s when international institutions like the IMF and World Bank were created, with the US and European countries holding huge sway in their governance structures. The Bretton Woods system effectively ended when President Nixon removed the convertibility to gold in the 1970s, but demand for dollars remained strong due to the scale of the US economy and because of the already established mechanisms for using the dollar internationally. You can read more about the history here.

Dollar dominance, therefore, is partly a reflection of the size and stability of the US economy, and partly a result of the post-World War Two settlement to use it as an international currency, which continually reinforces its status. It dominates not only how trade happens and goods and services are priced by being the main settlement currency globally, but also US-based payment systems and financial institutions have outsized roles in the global financial system. This leaves countries forced to continue to accumulate dollars to participate in the dollar-dominated global economy.

Now we’ve explained what ‘dollar dominance’ is, next we’ll explore who it benefits, who loses out, and how some countries are looking for alternatives to ‘move away from’ it in the next blogs in our series.

–

Want to learn more? Take a look at our ‘Beyond Dollar Dominance’ report, explainer videos, and check out the second blog in this series Dollar Dominance: The impacts!