UKEU

18 February 2026

The dollar remains dominant in foreign exchange markets, but there are clear signs that attempts to internationalise the renminbi are slowly bearing fruit amidst increasing reluctance in the Global South to rely on the dollar for trade and finance.

Every three years the Bank for International Settlements publishes a survey of foreign exchange (FX) and related financial markets, offering a snapshot of which currencies are traded around the world in deals between banks and investors.

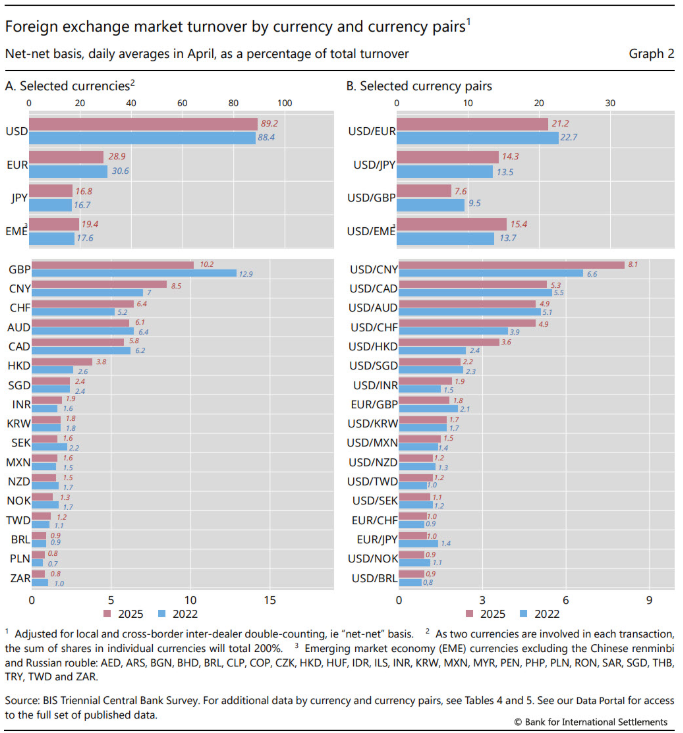

Given the outsized role of the US dollar in the global economy and its deep financial markets, it is unsurprising that the latest survey results show that the dollar continues to dominate foreign exchange markets, appearing on one side of 89.2% of trades, which is an increase from 88.4% in 2022.

However, perhaps the most eye-catching news in the latest survey is the increased market share of the Chinese currency renminbi. China’s ambitions to reduce its reliance on the dollar are far from new, but growing concern about the outsized role and weaponisation of the dollar has prompted Beijing policymakers to take a more proactive stance on internationalising the renminbi by supporting its use in trade, finance, investment, and payment infrastructures.

Amidst various measures to promote the renminbi’s internationalisation, the latest BIS survey showed that its market share in terms of FX trades had grown from 7% to 8.5% since 2022. While this rise may seem modest, it should be noted that the renminbi’s share was still 0% in 2001, and only 1% in 2010.

The centrality of the City of London in international financial markets is clearly visible in the results of the survey, with 38% of all FX trades recorded from desks in the UK. Nonetheless, the share of pound sterling traded in FX markets declined from 12.9% three years ago to only 10.2% in 2025.

Many other traditional Global North currencies also saw a drop in their prevalence on FX markets (Figure 1). The market share of the Euro fell from appearing in 30.6% to 28.9% of trades, while the Australian dollar and Canadian dollar fell from 6.4% to 6.1% and from 6.2% to 5.8%, respectively. Bucking the trend for Global North currencies, the Swiss franc increased its market share from 5.2% to 6.4%.

Figure 1: Foreign exchange market turnover by currency and currency pairs

Source: Bank for International Settlements

In addition to the increased share of the renminbi in FX markets, the Hong Kong dollar also saw sizable gains, with the Indian rupee and the Mexican peso also reporting small increases. Put together, a basket of Global South currencies (including renminbi but excluding the Russian rouble) increased from 24.6% in 2022 to 27.9% in 2025. This is a significant increase for such a short period of time, particularly given the incumbency advantages that established currencies benefit from.

While the rise in the use of renminbi and other Global South currencies in FX trading is relatively small, it nonetheless signals a significant development reflecting wider policies and ambitions to move towards increasing local currency finance and trade in the Global South.

In addition to the foreign exchange market, tighter monetary policy in the Global North in recent years have resulted in an increased appetite for renminbi credit, particularly in Asia-Pacific, mirrored by a reduction in dollar credit in the same region. As noted in a BIS statistical release on international banking, “the year 2022 marked a turning point away from dollar- and euro-denominated credit and towards renminbi-denominated credit [in the Global South]”. Since Q1 2021, Emerging and Developing Economies (EMDE) have seen a cumulative decline in cross-border dollar-denominated bank credit of $257bn, while cross-border renminbi credit expanded by $373bn over the same period.

However, the increased use of renminbi or other Global South currencies in foreign exchange markets may not be a desirable end in itself. These markets are highly financialised and speculative, and detached from the real economy. Instead, this trend can be understood to be a reflection of the increased use of the currency for trade, payments, and finance, inadvertently deepening the liquidity of the currency more generally.

It should be noted that China does not seek to challenge the dollar in the arena of foreign exchange markets, as it wishes to protect its domestic financial system through tight capital controls and limited convertibility. The increased use of renminbi in foreign exchange markets can instead be seen more as a necessary byproduct of the trade-focused goal to hedge against US weaponisation of the dollar by building alternative infrastructures for cross-border payments, credit, and trade settlement. By prioritising trade-based internationalisation of the renminbi, China has established a viable alternative to dollar-based payment and trade - also benefitting its trade partners who might be excluded from or disadvantaged by the dollar-based system.

The unequal status of currencies in the global financial system exposes countries lower down the currency hierarchy to various vulnerabilities and reinforces existing hierarchies between the Global North and Global South. You can read more about the details of this unjust hierarchy in our ‘Beyond Dollar Dominance’ report, but at the heart of the problem lies the fact that Global South currencies are not accepted on the international market for trade and finance, meaning that countries have to gear their economies towards the accumulation of dollars or other hard currencies to participate in the global economy. The US, on the other hand, benefits from the ‘exorbitant privilege’ of having its own currency being used as the global reserve currency, dominating both trade and finance.

Moving beyond the dominance of the dollar towards a more multipolar monetary order is therefore at the forefront of many policymakers’ minds. The issue of advancing local currency payment solutions featured prominently at the latest BRICS Summit, and we at Positive Money were delighted to see our recommendation to ‘promote efforts to building a multi-currency international financial architecture’ included in a T20 High Level Communiqué ahead of South Africa hosting the G20 summit.

The transformation towards a multi-currency system won’t happen overnight. It will require a lot of work and effort not just to build, but also in terms of resisting the efforts of the US and others who seek to maintain a status quo which grants them immense privileges at the expense of the global majority. However, initiatives to increase local currency financing and trade are gaining momentum, and calls for deeper structural reform to rebalance the global economy are only getting stronger.

Our report 'Beyond Dollar Dominance' can be found here. Sign-up to our mailing list for regular updates, or donate to support our work to redesign our economic system for social justice and a liveable planet.