Back to Archive![Official data shows richest gained over £300,000 each in era of QE]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

5 April 2013

Taxes & Public Spending

[vc_row][vc_column][vc_column_text] When banks are allowed to create a nation’s money supply, we all end up paying higher taxes.

[vc_row][vc_column][vc_column_text]

When banks are allowed to create a nation’s money supply, we all end up paying higher taxes. This is because the proceeds from creating new money go to the banks rather than the taxpayer, and because taxpayers end up paying the cost of financial crises caused by the banks.

1. The Proceeds from Creating Money

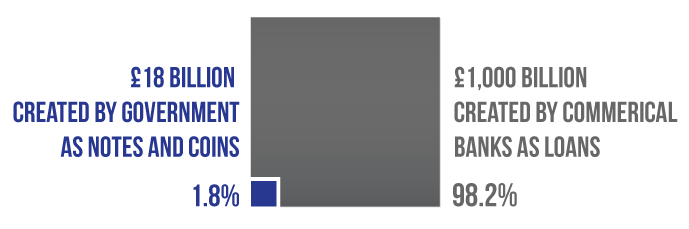

The Bank of England still prints paper money (e.g. £10 notes). Because it only costs a few pence to print a £10 note, the government makes a profit on every single bank note that it prints. Between 2000 and 2009, this profit on newly-created money added up to £18 billion – enough to pay the salaries of around 90,000 nurses over that time.

But the Bank of England only creates the paper money, and leaves it to banks to create the electronic money that we also use every day. When banks create money, they – not the government or the taxpayer – get the benefits of creating that money.

From 2002 to 2009, banks increased the amount of money in the UK by £1 trillion through lending (with every new loan creating new money). Because this money was created by banks, it’s the banks that get the benefit from it (in this case, the interest received on £1 trillion of additional loans).

If the government had created this money instead of the banks, taxpayers would have been able to pay up to £1 trillion less taxes: approximately £33,000 for every person who pays income tax over just 7 years.[1]

Money creation: 2000 – 2009 inclusive

2. Interest on the National Debt

Because the profits from creating money currently go to the banks instead of to the government, the government has to borrow much larger amounts of money to make up for this lost income.

As taxpayers, we have to pay the interest on all this money that the government has borrowed. We currently spend more in interest on the national debt (£51 billion annually) than we spend on either defence, the police or on transport (including the road system). This interest costs works out at £1,700 per income-tax payer per year.[2]

The more money that is spent on interest on government debt, the less money there is to spend on public services, and the higher taxes will be without getting anything extra in return.

3. Deficit: the Cost of Crises and Recessions

When the financial crisis hit in 2008, hundreds of thousands of people lost their jobs, people stopped spending and businesses’ sales fell. All of this meant that the government collected significantly lower amounts of tax, due to fewer people working, and lower profits by businesses.

At the same time, more people went onto unemployment benefit, which meant that the government’s costs went up significantly. The gap between the money coming in (tax revenue) and the money going out (expenditure) rocketed from £30bn right up to £180bn. This gap is the ‘deficit’, and had to be covered by borrowing money.

Without a banking system that creates money every time it makes a loan, we wouldn’t have these crises and wouldn’t need to use taxpayers’ money to rescue banks.[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_message color=”alert-info”]Learn more about how the national debt works here >>>[/vc_message][/vc_column][/vc_row][vc_row][vc_column][vc_accordion active_tab=”false”][vc_accordion_tab title=”Sources”][vc_column_text]1. HMRC states that there were 30 million income tax payers in 2012-2013.

2. Of course, this interest cost will be covered across all taxes, so some of the cost will be incorporated into taxes paid by companies that you shop with, etc.[/vc_column_text][/vc_accordion_tab][/vc_accordion][/vc_column][/vc_row]