Back to Archive![The fiscal benefits of a digital pound]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

11 November 2013

What about the National Debt?

This section is condensed from an appendix from our book Modernising Money.

This section is condensed from an appendix from our book Modernising Money.

What is the national debt?

The government has three main sources of revenue:

Taxes & fees – such as Income Tax, National Insurance, Value Added Tax (VAT), taxes on alcohol, fuel, flights and so on.

Borrowing – this is mainly achieved through the issuing of bonds.

Creation of money – the revenue from this source is negligible under the current monetary system.

If government spends more than it collects in taxes the difference is called the ‘deficit’. If it collects more in taxes than it spends, this difference is called a ‘surplus’. Surpluses have been relatively rare in the UK in recent decades, with the government typically running deficits, spending more than they collect in taxes and borrowing to make up the difference. These deficits have increased the outstanding nominal (i.e. not adjusted for inflation) value of the national debt (whereas surpluses would have reduced it).

Who does the government borrow from?

Rather than borrowing from banks, the government typically borrows from the ‘market’ – primarily pension funds and insurance companies. These companies lend money to the government by buying the bonds that the government issues for this purpose. Many companies favour investing money in government bonds due to the lack of risk involved: the UK government has never defaulted on its debt obligations and is unlikely to in the future, primarily because it is able to collect money from the public via taxation. The market in government debt also tends to be stable and liquid, and offers an interest rate in excess of that which is available on other riskless investments (i.e. physical cash).

Does government borrowing create new money?

In most cases the process of government borrowing does not create any new money. While most individuals and businesses accept bank deposits in payment, the UK government does not; they require that the purchasers of new bonds ‘settle’ the transaction by transferring central bank reserves (see The Three Types of Money) into a government-owned account at the Bank of England. This means that new money is not created in the process of government borrowing.

For example, let’s say a pension fund holds an account at MegaBank, and wishes to buy £1 million in government bonds. The fund asks MegaBank, which is one of the Gilt-Edged Market Makers (a bank authorized to deal directly with the government in the purchase of new bonds), to buy £1 million of new government bonds. MegaBank decreases the pension fund’s account by £1 million and then purchases the bonds on behalf of the pension fund. To settle its transaction with the government, it transfers £1 million of reserves to the government’s account at the Bank of England. The balance of MegaBank’s account at the Bank of England will drop by £1 million. The government now has £1 million of central bank reserves in its account at the Bank of England, which can be used to make payments. It has borrowed the money without any additional deposits being created.

To spend the money it could now transfer the reserves to Regal Bank where an NHS hospital holds an account. Regal bank would then receive £1 million of central bank reserves, and could increase the account balance of the hospital by £1 million.

So through a rather convoluted process, £1 million of bank-created bank deposits have been taken from pension fund contributors and passed to an NHS hospital. No additional money has been created; only pre-existing deposits have been moved from one place to another. Because the majority of government borrowing is done in this way it does not constitute a monetary stimulus to the economy.

(The exception to this rule is with Private Finance Initiatives, where the government borrows directly from banks. In this case, so long as the government accepts bank deposits rather than requiring a payment into its account at the Bank of England, then banks create the money that the government borrows via Private Finance Initiatives).

Is it possible to reduce the national debt?

The debt is currently higher (in nominal terms) than it’s ever been before. While the government talks about reducing the deficit, the reality is that the total national debt will keep growing. Even if it stops the debt growing, taxpayers will continue paying around £120 million a day in interest on the national debt.

It is very unlikely that the government will be able to reduce debt in the current system. To understand why, consider what would need to happen for the debt to be paid down. First, the government would need to start paying the annual interest on the national debt each year out of tax revenue, rather than simply borrowing the money to pay it. Interest payments totalled £43bn for 2012, so if the government wanted to reduce the debt it would have to find an additional £43bn in taxes, which would require, for example, raising VAT (sales tax) to roughly 30% (from its current level of 20%).

In addition, in the five years before the banking crisis the government spent an average of 10.6% more than it received in taxes every year. So even after the £43bn interest on the national debt is paid, to run a ‘balanced budget’ right now, it would need to raise an extra £22bn in taxes (to cover the 10.6% shortfall), or cut public services by £22bn – equivalent to shutting down a fifth of the National Health Service.

So far in this example, the government has raised VAT by 30% and cut £22bn of public services and has still only managed to stop the debt growing. In order to actually reduce the debt, it needs to raise taxes even further, or reduce public spending even more. If the government decided that it wanted to pay off £30bn of national debt every single year, then it would need to raise another extra £30bn in taxes: equivalent to doubling council tax. Even at this level it would take 30 years to pay down the national debt, assuming tax revenue is unaffected by these changes.

Of course, increasing taxes by such large amounts is likely to lead to a recession and even a depression: businesses will pass on the costs of higher taxes to their consumers, with the increase in prices likely to lower demand for goods and services. Likewise, faced with higher taxes, individuals will have lower levels of disposable income, and, independent of the increase in prices this will negatively affect demand. Both factors will feed through to lower sales and therefore lower sales taxes, forcing the government to further increase taxes to hit its debt reduction target. Lower demand for goods and services will also lead to businesses cutting employment, lowering the government’s income from employment taxes. Higher levels of unemployment will also increase the government’s spending on unemployment benefits, which will have to be funded through further borrowing, again preventing the government from hitting its targets.

Alternatively the government could cut its spending. However, this is likely to have similar effects to increasing taxes. During recessions people tend to cut their spending – if the government cuts its spending at the same time the result can be a catastrophic drop in demand. This of course lowers output and therefore the tax take. Indeed, in a paper looking at eight episodes of fiscal consolidations (i.e. cuts in government spending), Chick and Pettifor (2010) find that:

“The empirical evidence runs exactly counter to conventional thinking. Fiscal consolidations have not improved the public finances. This is true of all episodes examined, except at the end of the consolidation after World War II, where action was taken to bolster private demand in parallel to public retrenchment.”

As they point out this runs contrary to mainstream thinking, where recessions are thought to be, at least in the long-term, self-correcting. The presumption is that eventually the fall in demand will lead to lower prices, at which point demand increases (as the fall in prices increases relative wealth), which increases demand (the Pigou-Pantinkin effect). However, as was discussed in Chapter 9, when money is created with a corresponding debt, a fall in prices leads to an increase in the real value of debt, thus the negative effect on the real value of debt offsets the positive effects on real wealth. Thus lowering spending/increasing taxes is likely to lead to a fall in tax revenues, requiring even further tax increases/spending cuts and so on. In fact, in this situation a debt deflation scenario is far more likely if the population is highly indebted to begin with.

Is it desirable to reduce the national debt?

On the surface, paying off government debt may be beneficial because lower government debt frees up government revenue for core services. It is argued that high levels of government debt may also be problematic in the long run because:

Government bonds compete with private sector investments for funds, so government borrowing diverts money away from private sector investments and increases the rate of interest the private sector pays to attract investment.

Individuals may start saving more (and so spending less) in expectation of an increase in future taxes (to pay off the debt). (This is known as Ricardian Equivalence).

Because of the potential for adverse effects to long term interest rates and the exchange rate.

There is also the danger that excessive government debt can lead to a sovereign debt crisis, as seen in Greece and other Eurozone countries. However, for countries that retain control of their currencies (i.e. those that have central banks that are able to print currency, such as the UK, the US, Japan, but crucially not the Eurozone countries) defaulting on debt is only one of two options, as the country could simply print currency to pay off its debts. Of course, if this printing of currency caused significant inflation it would reduce the real value of the debt and represent a form of hidden default, in that the holders of the debt would not be repaid as much, in real terms, as they initially invested.

However it is important to also recognise the positive effects that come from having at least some national debt:

First, as mentioned previously, the debt gives the private sector a safe asset in which it can invest. This strengthens private sector balance sheets, increasing their robustness in the face of downturns and negative shocks (because bond prices don’t fluctuate as severely as stock prices).

Second, it allows a degree of certainty for institutional investors looking for long term returns (such as pension funds with older beneficiaries, who need security over capital gains).

Third, it allows the private sector (excluding the government), in aggregate to hold a positive balance of wealth (see for example Godley and Lavoie (2012)).

Fourth, it is misleading to think of the national debt in the same way as we think about private debts. The major holders of the national debt are UK investors: mainly pension funds and insurance companies. Thus, it is in many senses a debt we owe to ourselves (albeit it one owed by current taxpayers to current holders of the debt, which can create an inter-generational transfer of wealth). That said, approximately 40% of the national debt is owned to foreign investors (also pension funds and insurance companies).

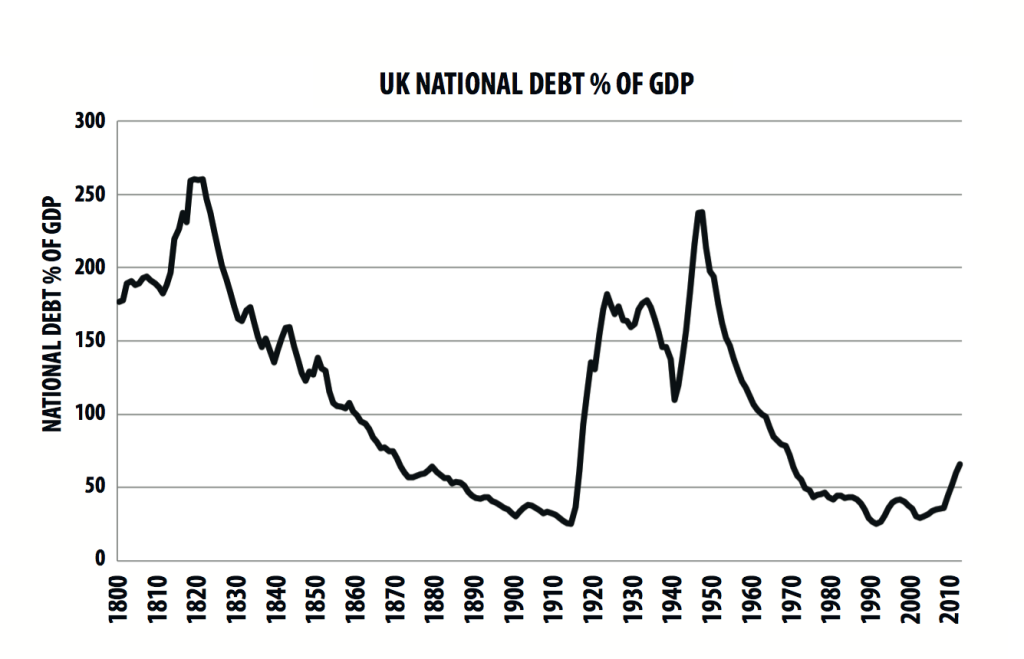

In addition, it is important to remember that the nominal value of the debt is not actually important; it is the level of debt (and its maturity) relative to the earning capacity of the economy that is the important figure. For example, an individual with no income and no assets may consider a debt of £10,000 impossible to repay, yet an individual that earns £1 million a year would consider the same debt an inconsequential sum. Broadly speaking, the ‘income’ of the nation can be represented by GDP (Gross Domestic Product). The chart below shows the national debt as a percentage of the UK’s GDP:

This brings into context the comments made earlier about the government never really paying off its debt. Instead of paying off the debt by actually reducing its nominal value, the debt tends to be reduced over time in terms of its burden. Rather than decrease the nominal amount of the debt, the earning ability of the economy (GDP) is increased.

Unsurprisingly the national debt to GDP ratio tends to shoot up during wars – such as World War I (from £650m in 1914 to £7.4bn in 1919) and World War II (from £7.1bn in 1939 to £24.7bn in 1949). It also shot up significantly in 2008 onwards, as the tax take plummeted due to the recession and spending (for example on unemployment benefits) increased. (The borrowing to bailout banks is not included in the main national debt figures.) It is pertinent to note here that despite the financial crisis, public debt is actually at a relatively low level (albeit at its highest level historically in the absence of a World War). In addition, we must be clear that the largest part of the recent increase in public debt came about not due to too much spending, but rather as a result of the government’s reaction to the financial crisis.

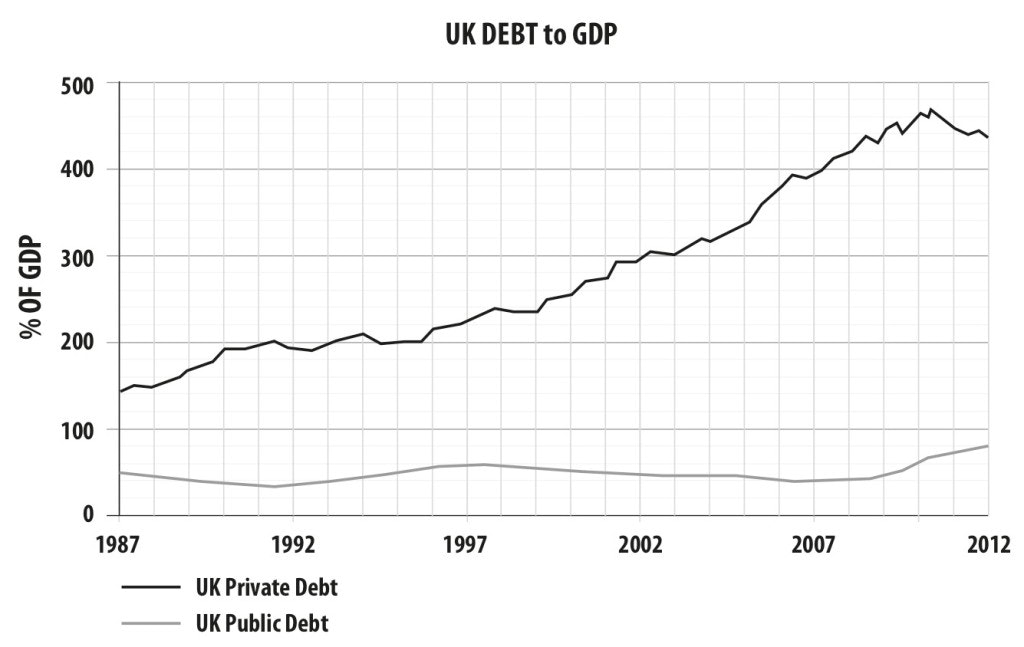

This brings us to the crux of the argument. The first half of this book [Modernising Money] was largely concerned with the effect of the banking sector on the economy and society as a whole. The excessive creation of private (i.e. household and business) debt was shown to be a major cause of boom bust cycles, financial crises, recessions, etc. As can be seen from the chart below, the level of private debt far exceeds the level of public debt, and as such this should be the focus of debt reduction efforts:

As well as looking at absolute values, the cost of debt (i.e. the interest rate on the debt) should also be considered. In this context the overall interest rate on the national debt between 2000 and 2012 worked out at around 5.6% per annum (Webb & Bardens, 2012). In contrast, the interest rate for household debt ranges between 6% and above for mortgages, right up to 17% on credit cards and up to 29% on store cards. Overall, the average interest rate is undoubtedly higher for households than it is for the government. For these reasons, the government should focus on enabling the public to reduce its debts.