Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

9 May 2012

Why Student Debt? What Can We Do about It?

A lot of students like me (and a lot of people in general) are opposed to tuition fees and the coalition government’s decision to dramatically increase them next year.

A lot of students like me (and a lot of people in general) are opposed to tuition fees and the coalition government’s decision to dramatically increase them next year. This is not merely for selfish reasons. In my view, tuition fees are bad news chiefly because they turn university from an education into an investment.

We badly need individuals who can think in new ways to solve today’s diverse problems – many of which are being caused by “business as usual”. Universities are one place where such individuals can be nurtured; but not if courses devolve into glorified job training centers at the behest of students themselves, anxious to graduate into the kind of structured careers that can repay their debts. There is such a thing as society, and tuition fees are bad for it.

When government spending falls, private ‘lending’ has to take up the slack.

But let’s put ourselves in the position of the government for a minute. The financial crisis lead to bank bailouts and a recession that reduced taxation revenue. The Labour government had to step in to cover the shortfall, significantly increasing the UK national debt. Along with a lot of the electorate, the coalition government are worried about the prospect of the national debt growing further – we are currently paying about £40bn annual interest on it. If not from more government ‘borrowing’, the money to pay for higher education has to come from somewhere else. It can’t come from other vital parts of the welfare state – these are already under-funded. More student debt might look like the “least worst option” for the coalition and much of the electorate.

Don’t get me wrong. I’m not writing an apology for the government here. They should be far more worried about UK private debt (over 400% of GDP, one of the highest figures in the world!) than UK national debt (only about 60% of GDP, one of the lowest figures in the world). And they could be funding higher education through taxation. Public pressure is mounting to close down tax havens and levy a financial transaction tax and this is good.

But there is a parallel approach we can take, one that most students don’t even realise is there and one that doesn’t rely on the “generosity” of the super-rich or on international collaborations to work. Also, I think it will end up being more effective anyway, by using pre-distribution (James Robertson’s term) rather than redistribution via bureaucratic taxation measures. So what is the approach? To describe it, we must begin with a question. Fellow students, have you ever asked yourself Where does money come from?

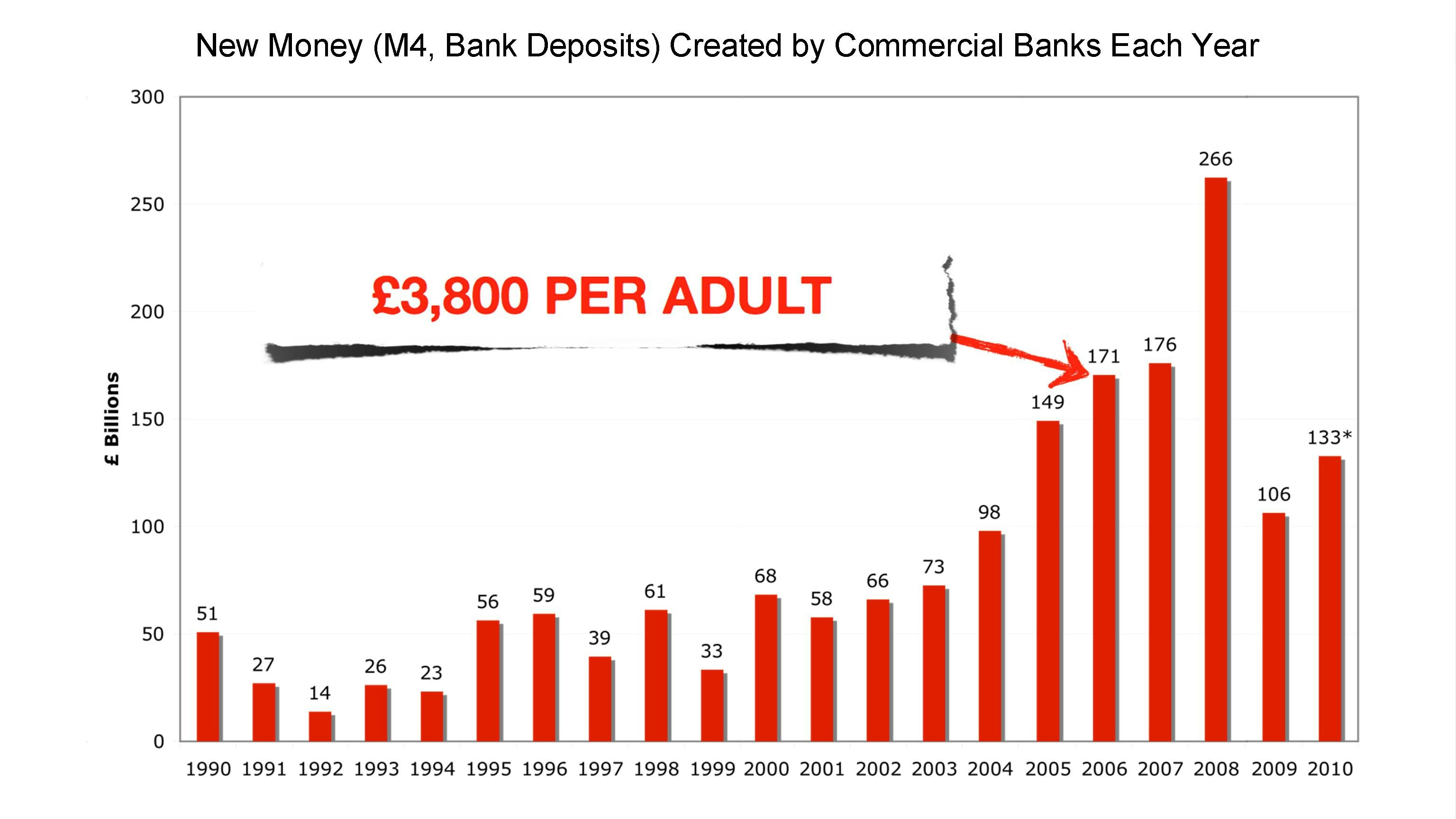

Most of us think that the government / the Bank of England issues the money supply and it’s true that notes and coins are minted there. But what about the numbers in your bank account? Are they money? Most of us would say, yes of course, that’s my money in the bank. But who created these numbers? The answer is that private banks did, when they issued something they misleadingly call a ‘loan’. I’ve written about how it works here and how banks do not lend money, they create it. In fact banks create and allocate about 97% of our nations money supply this way – here is some proof, straight from the horse’s mouth.

So banks create and crucially allocate most money – the word “allocate” means they decide who the new money is given to first, according to whether or not they think it will make them a profit. This gives them a lot of control over the economy and where money is scarce and abundant within it. If that concerns you, good! It’s one reason why there seems to be less and less money available to fund not-for-profit state projects like the NHS and higher education.

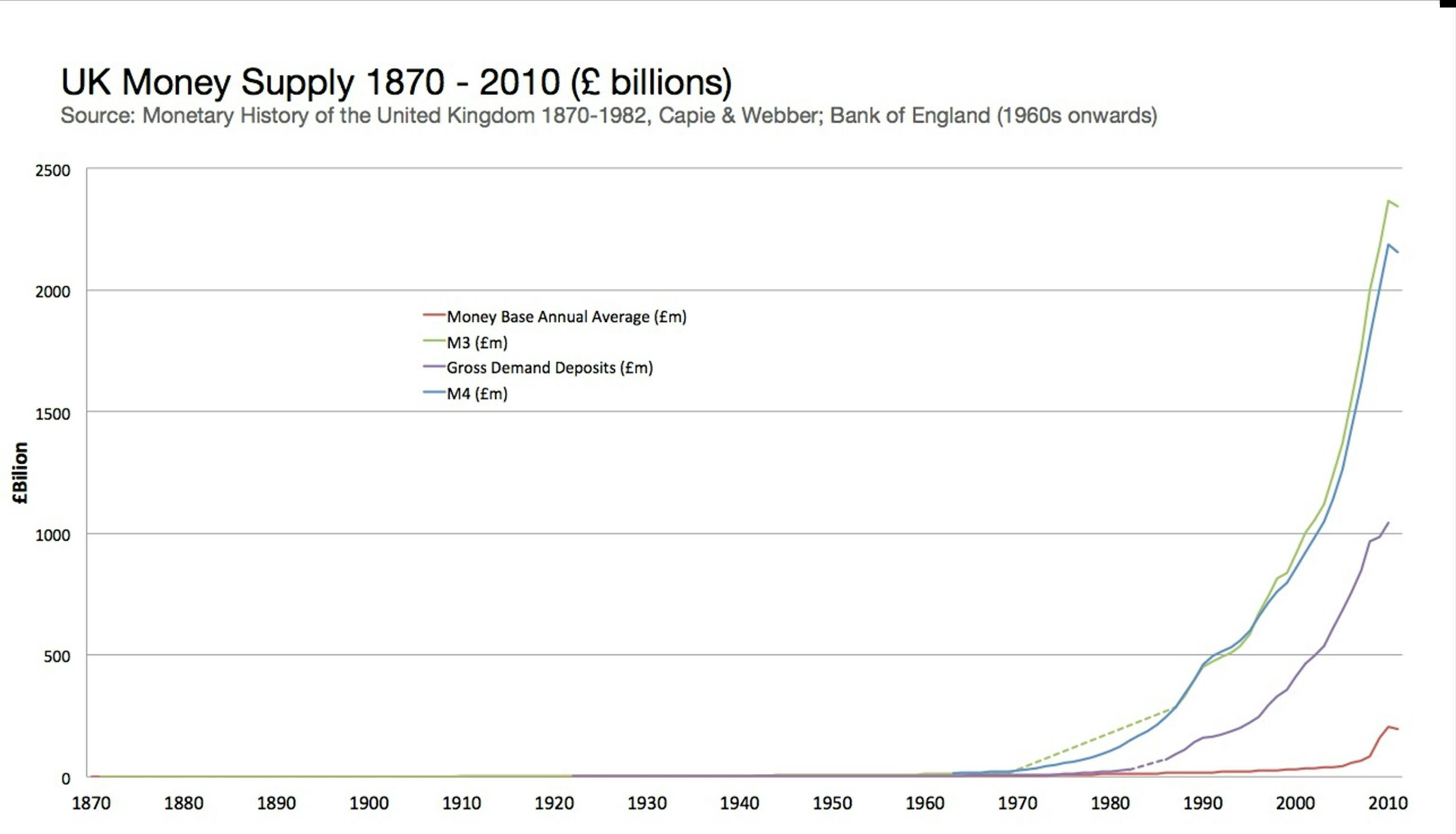

Let me explain. In the 1960s, when univerities were almost entirely publicly funded (see top graph), cash and coins made up about 20% of the nation’s money supply. Since then, the percentage has gradually fallen and today is less than 3% – with the other 97% being digital bank deposits. So what? Well, when the government creates say a £10 note, it charges banks the face-value of £10 for this. The note only cost a fraction of this face-value to mint, so the government gets to pocket the rest, a source of income called seigniorage.

The government also gets to decide where this seignniorage income is allocated – it can stimulate the not-for-profit sector (health and education) as opposed to bank ‘loans’, which go to whatever is most profitable to banks. The fact that this debt-free part of the money supply has fallen from 20% in the 1960s to 3% today is one reason why the state is chronically short of money to fund health and education, and has to rely increasingly on the private sector.

In the 1960s, the government would receive seigniorage on about 20% of the money created above. Today banks create this 20% instead and receive interest on it – no wonder we’re so short of money for education! (a slide from Ben Dyson’s talk: http://www.youtube.com/watch?v=9K5dao1lUQ0&list=PL32339BDA75B6BFC8&feature=mh_lolz)

The important point with seigniorage is that it proves that governments (or alternatively, students!) don’t need to go into ever more debt to fund higher education. Instead we could create new digital money free of debt, and allocate this to different sectors of the economy (universities in this case). As famous inventor and monetary reform enthusiast Thomas Edison once put it:

“If our nation can issue a dollar bond, it can issue a dollar bill. … Both are promises to pay; but one promise fattens the usurer, and the other helps the people.”

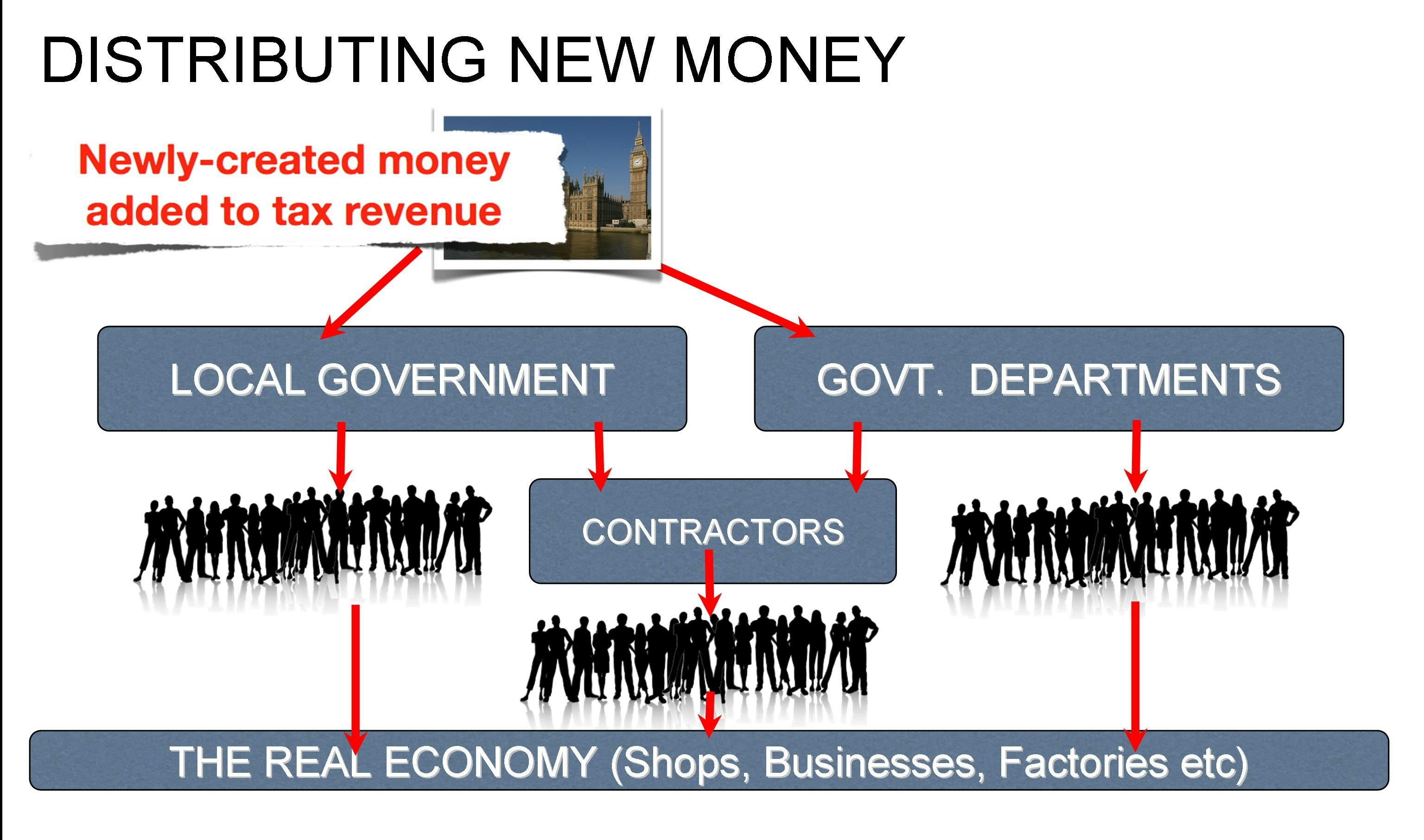

Here’s how it could work:

Allocating government money in a locally responsive way (a slide from Ben Dyson’s talk: http://www.youtube.com/watch?v=9K5dao1lUQ0&list=PL32339BDA75B6BFC8&feature=mh_lolz)

Money could also be extracted from the economy above via taxation and destroyed. That might sound strange to you: we have been conditioned to think of taxation as the source of income for the government. But a nation creating its own money has no need for taxes as a source of income. Today’s government only needs to take so much tax because they have handed the power to create money over to private banks, without the people’s consent or awareness. So if you want to pay less tax, take this power back!

Let’s now consider two common objections to the above ideas: conflict-of-interest and inflation. Firstly, if you’re worried about the government both creating and allocating the money supply then you’re in good company and probably these functions should be separated. An independent and publicly accountable body can decide how much money the nation needs. Then the government, based on its election manifesto, will decide how to allocate this money (and banks will merely lend out the deposits of savers, in the way that most of us mistakenly think they currently do). Consider this too: if you don’t want the government both creating and allocating the money supply, surely you don’t want a cartel of private, profit making firms called banks doing so either?

The same goes for inflation. If you’re worried the government will create too much money this is another argument for separating who allocates the money and who decides the quantity. Provided the government allocates new money to productive parts of the economy, goods and services can grow with the money supply and there needn’t be inflation. Or excess money could be extracted via taxation, as mentioned earlier. Consider this too: if you don’t want the government creating as much money as they think is good for their short term re-electability (and to hell with the economy), why on Earth would you want private banks creating as much money as they think is good for their short term profitability (and to hell with the economy)?

Private banks can cause inflation and financial crises, by creating new money for speculative bubbles. “Banks don’t have to cause crises… But they almost always do.” – Prof. Steve Keen

Hopefully you’re still with me! We’ve discussed that banks create and allocate digital bank deposits, that these increasingly constitutes the entire national money supply and that this is an important reason the government can’t find any pennies down the back of the sofa to spare for the health and education of its citizens.

But today’s system of money creation by private banks is not a law of nature! If we build enough public pressure this system can be changed to one where money is allocated for the social good by an elected government responsive to the public will; not by an “industry” that only considers its own profitability and will thus tend to gorge itself on speculative bubbles whilst starving health and education of vital funding. They caused the current crisis this way, by pumping new money into property, inflating house prices to the point where students in particular cannot afford them. So, if you ever want to move out of your parents’ house, perhaps we should stop private banks creating the money supply!

How can students help? You can join Positive Money, a London based monetary reform NGO, and support their campaign to take the power to create money from banks and put it where it belongs, in public hands. Money is social – we all agree to accept it and as we found out during the financial crisis, we ultimately back it. Rather than allowing private banks to create the national money supply as debt and charge us interest for its use, we the people should enjoy a “free-lunch” of seigniorage on money creation – since it is our money. Rather than watching huge sums of our money move into financial speculation instead of social services, then struggling in vain to claw enough of it back via taxation (“redistribution”) we could make sure our money is allocated as we wish to begin with (“predistribution”).

You can try to educate your MP. Most politicians are completely ignorant of how money is created and have never seriously asked questions like: Where does money come from? Why are we all in so much debt? If we are all in debt, who are we in debt to? How do we get of debt? How can getting into more debt be the answer to that question?! The current system of money creation, as interest bearing debt by private banks, presents our politicians with two choices. Either:

1 – Have more money, but also more debt (deficits).

2 – Have less debt, but also less money (recession).

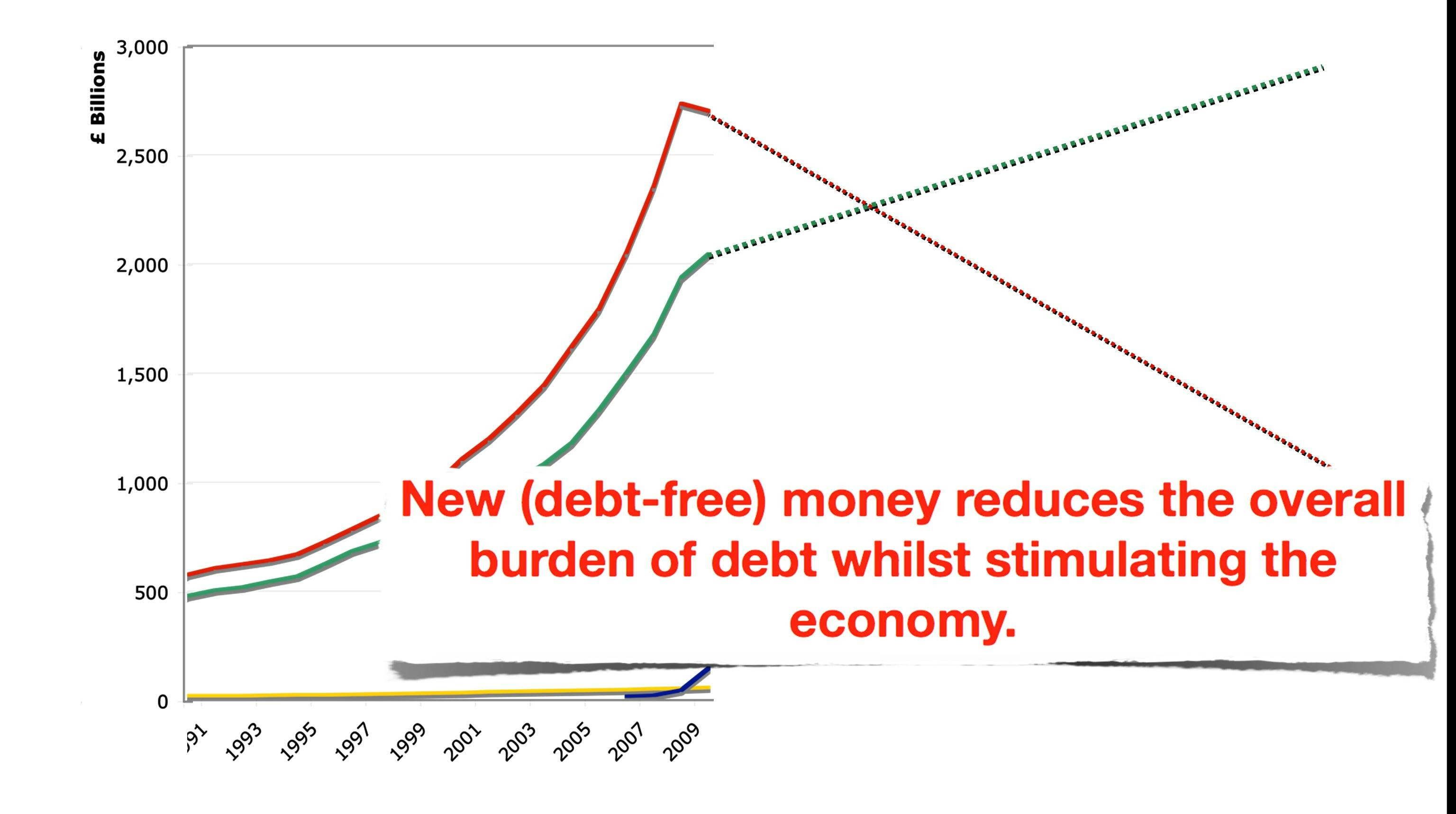

We would like to have less debt and more money. But with “our” current monetary system, that option is practically impossible! It will only be possible when we decide to start creating money free of debt:

Creating debt-free money (green line) to get out of debt (red line) (a slide from Ben Dyson’s talk: http://www.youtube.com/watch?v=9K5dao1lUQ0&list=PL32339BDA75B6BFC8&feature=mh_lolz)

Perhaps David Cameron ought to understand all this? After all, he has a 1st class honours degree in PPE from Oxford University. Unfortunately, mainstream economics courses pay little attention to how money is created and allocated to the economy. This blind spot of mainstream economics for money and debt is a big part of the reason why we are in this mess today. As economist Steve Keen (winner of the Revere Award, for “the economist who first and most cogently warned the world of the coming Global Financial Collapse”) puts it:

“The whole idea that you can model capitalism without including money and debt in your models – and that’s 99.9% of neo-classical models include neither money nor debt – is a bit like trying to model how a bird flies by assuming that it doesn’t have wings. It’s just ridiculous that it’s left out.”

Another vital thing you can do is tell your friends about who creates and allocates money and what this means for power, democracy and the future of the welfare state. Spread the news via social networking! If Kony2012 showed anything, it was that social networking gives the power to rapidly bring an issue to mass awareness. Many made the criticism that the Kony2012 campaign lacked substance or adequate understanding of the underlying issues, but I think Positive Money has spent enough time building substance and understanding behind its campaign demands. It now needs mass awareness and students can definitely help here! If as many people watch the brilliant new documentary 97% Owned as watched Kony2012, we might be onto a winner!

The campaign to give the power to create money to the public, where it belongs, will only succeed with a significant increase in public understanding and support. Politicians can’t do it on their own. Only a handful of them understand the problem anyway and those that do will have to challenge powerful vested interests. They won’t be able (or willing?) to do this without public backing. In my view, who gets to create and allocate the money supply is the critical issue for power and democracy in our times. So students, start making some noise – let’s democratise money!