Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

20 November 2013

Soaring UK personal debt wreaking havoc with mental health, report warns (The Guardian)

Poorer people are “bearing the brunt of a storm” during which average household debt has risen to £54,000 – nearly double what it was a decade ago, the report by the Centre for Social Justice thinktank warns, reads The Guardian, 20th Nov 2013 The report, entitled Maxed Out, found that almost half of households in ...

Poorer people are “bearing the brunt of a storm” during which average household debt has risen to £54,000 – nearly double what it was a decade ago, the report by the Centre for Social Justice thinktank warns, reads The Guardian, 20th Nov 2013

The report, entitled Maxed Out, found that almost half of households in the lowest income decile spent more than a quarter of their income on debt repayments in 2011. More than 5,000 people are being made homeless every year as a result of mortgage or rent debts.

Christian Guy, director of the thinktank established in opposition by the work and pensions secretary, Iain Duncan Smith, said: “Problem debt can have a corrosive impact on people and families. Our report shows how it can wreak havoc on mental health, relationships and wellbeing. Across the UK people are up until the early hours worrying about their finances and bills.”

The report, written by the former Labour work and pensions minister Chris Pond, found that:

• Personal debt in the UK, including mortgage lending, stands at £1.4tn – an average of £54,000 per household compared with £29,000 a decade ago.

• Consumer debt had trebled since 1993 and now stands at £158bn;

• More than 8m households have no savings, including half of low-income households;

• Outstanding debt on credit cards has almost trebled since 1998 to reach £55.6bn;

• There were 300,000 arrears on mortgage in 2012 – with 34,000 homes repossessed. This is a reduction of 30% from the peak of the recession but a 60% overall increase since 2006.

You can read the whole article here.

But why is there so much debt?

Who did we borrow all this money from? Was it from an army of grannies who have spent their whole lives putting money away for a rainy day? No. When you go into a bank and borrow a large amount of money to buy a small amount of house, that money doesn’t come from somebody else’s savings.

It’s just created, out of nothing, by the bank, with a few taps on a computer keyboard. (How banks create money)

Now, here’s the problem: If almost all the money we use is created by banks when they make loans, then for every pound of money, there has to be a pound of debt.

If we want more money in the economy, we have to go further into debt to the banks, because more borrowing from banks means more new money is created.

But the process happens in reverse when we repay loans; when we pay down our debts, the money effectively disappears. This makes it impossible for all of us to reduce our debts. If we start paying it off, then the amount of money in the economy shrinks. Less money in the economy means less spending, and less spending means fewer jobs.

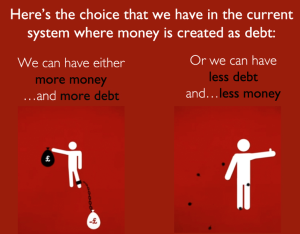

So there’s the choice: we can have either more money and more debt. Or we can have less debt and less money.

When the only way to get money into the economy is to borrow it from the banks that create it, then we’ll always be trapped under a mountain of debt.

But it doesn’t have to be this way

If we took the power to create money away from banks, and instead have money created by a public institution that isn’t chasing short-term profits, then this new money, as it supports jobs and the economy, could be used to pay down the debt and we could finally start to clear this mountain.

Watch our video Why is there so much Debt?