Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

28 January 2015

QE for Europe – an Opportunity Lost

Quantitative easing is back, only this time in the Eurozone.

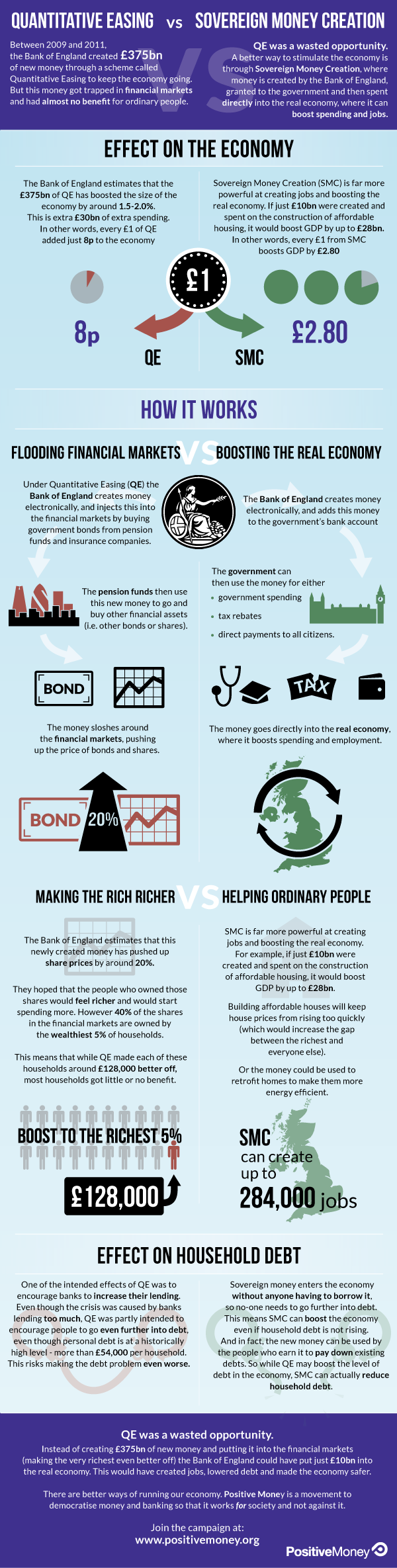

Quantitative easing is back, only this time in the Eurozone. But is the ECB making the right decision? Like many other economic commentators, here at Positive Money, we think it’s the wrong decision, not because it will have little or no effect, but because it won’t have the right effect! QE works by pouring money into financial markets, when what is really needed is to inject money directly in the ‘veins of the real economy’ to address Europe’s significant unemployment problem. For Europe, QE in its current form will be a huge wasted opportunity.

In reasonably simple terms, QE is a procedure whereby a Central Bank, (i.e. the ECB, European Central Bank), issues new money electronically, and uses this money to buy government bonds (mainly) that are currently held by the private sector (specifically, pension funds, insurance companies and banks).

By buying these assets the central bank pushes up their price, which simultaneously pushes down their yields (the return that bond holders earn). The lower yields should force investors to move their investments into riskier assets with higher yields (like corporate bonds and shares), hopefully directing more credit and investment towards businesses. Similarly, lower yields means that borrowing costs for business will be lower, making it cheaper for them to invest or spend more. The central bank will be hoping that some of the new money created and injected into the financial markets will reach businesses that issue bonds and shares, who will spend more, boosting employment.

But how well did this complex process work for the UK and the US? The Fed and Bank of England argue that it has made a contribution to the recovery in the US and the UK, often suggesting that the situation may have been much worse without QE.

While this is debatable, what is clear is that QE has funnelled billions (£375bn in the UK) into the financial markets, whilst hoping that that money would eventually ‘trickle down’ to the real economy. This money creation helped spur a bubble in financial markets: by the Bank of England’s own estimates, QE in the UK pushed up share and bond prices by around 20%. But because around 40% of stock market wealth is held by the wealthiest 5% of households, QE has made that wealthiest 5% better off by around £128,000 per household. The evidence is that it has done very little to create jobs and increase economic growth.

There is a far more powerful way of creating jobs and boosting economic growth. The European Central Bank could create the €1.1 trillion that it intends to create, but transfer it to national governments (allocated proportionately to the population) to spend directly into the real economy. This “sovereign money” approach, as advocated by Positive Money, would mean that the ECB and EU could make the recovery much more sustainable, without the negative effects (on inequality and financial market bubbles) that QE has. Newly created sovereign money could directly fund government spending (i.e. infrastructure or renewable projects), tax reductions, or even direct payments to all citizens (of approximately €3,000 per Eurozone citizen!).

Whereas QE in the UK and the US relied on flooding financial markets and hoping that some of this money would ‘trickle down’ to the real economy, sovereign money works by injecting new money directly into the real economy. By getting spending power directly into the hands of the public, this new solution could be up to 37 times more effective than QE in boosting GDP.

In sum, QE for Europe will be a wasted opportunity. The power to create money can be used to benefit the public, reduce unemployment and boost the economy, but not if we rely on that newly-created money trickling down from the financial markets.

(More analysis to follow over the next few days).

This infographic shows how QE was ineffective in UK, and how the creation of sovereign money by the state would have been up to 37 times more effective: