Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

28 April 2015

What the Politicians Really Aren’t Talking About?

As the UK general election is nearly upon us, many commentators are highlighting the important issues that the majority of politicians seem reluctant to discuss.

As the UK general election is nearly upon us, many commentators are highlighting the important issues that the majority of politicians seem reluctant to discuss. While I read, watch, or listen, I’m left slightly disgruntled, often feeling less satisfied than before having engaged with the coverage.

There is one issue that isn’t being mentioned by politicians or the media: the use of debt as a policy tool to spur economic recovery. This is despite the fact that we’re trying to recover from a crisis that was largely caused by excessive leverage and irresponsible lending.

The Office for Budget Responsibility has forecasted a return of household debt to pre-crisis levels over the course of the next parliament, but few politicians genuinely seem concerned.

At a presentation last week, Martin Wolf, the chief economics commentator of the Financial Times, said that future generations will look back on the people in charge of our financial system and think that they were either stupid or corrupt, or both. With policy makers currently turning a blind eye to household debt, it is no surprise.

For the sake of clarity, debt in itself should not be antagonised, nor treated as some sort of debauched abstract concept. There is no denying that some debt and a certain type of lending can be very useful. However, we are in a monetary system where the only way to get new money into the economy is to encourage more lending. A reliance on debt and money creation by banks as a source of growth increases vulnerability to future crises, and severely limits the potential for recovery.

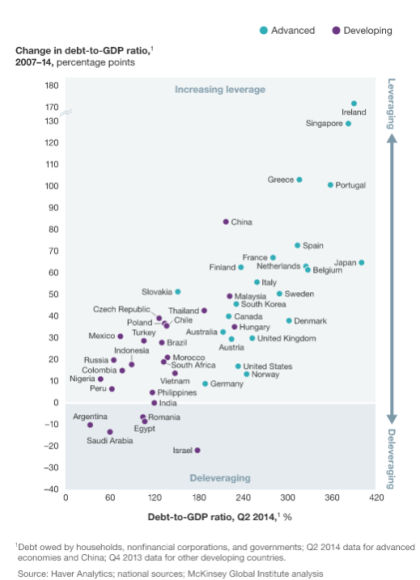

Currently, total private sector debt stands at £8 trillion (this includes private bank lending and foreign lending, loans from finance companies, and total long and short-term bills and bonds issued), while public sector debt represents another £1.45 trillion. According to these measures, UK debt to GDP stands at about 550%. Indeed, the debt-to-GDP ratio (for households, non-financial businesses, and the Government) stands at about 250%. This had increased almost 30% since the onset of the financial crisis.

Household debt is looking particularly worrying: unsecured debt (e.g. personal loans and credit cards) hit an all-time high at the end of 2014, of almost £9,000 per household, predicted to reach £10,000 by 2016. The total stock of non-mortgage borrowing grew at its fastest rate in 10 years, by about £20 billion (9%) in 2014.

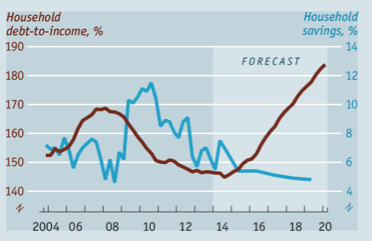

In the meantime, the Office for Budget Responsibility has estimated that savings will continue to decrease while the total household debt to income ratio will soon surpass its pre-crisis high, and increase to 184% by 2020. UK household debt has increased to one of the highest amongst advanced economies. It even has foreign watchdogs worried, evidenced by the IMF who recently added the UK to a warning list of nations susceptible to financial crisis.

While debt seems to be increasing, there is much discussion of the current economic recovery in terms of GDP. However, the chart below paints a very different picture, when considering GDP per UK citizen. While GDP per capita is slowly picking up, since WWII GDP per head has never stagnated for such a long period of time – yet household debts are increasing.

Of even more concern, the disposable income of UK residents has remained stagnant for the last five years. Indeed, the Net National Disposable Income per head (NNDI), which represents the income available to UK residents, shows that disposable income still remains 5% below pre-crisis levels.

Thus, despite increasing debt levels, UK residents are not any better off than before the crisis. Although GDP per capita may be showing some signs of increasing, this is not the case for NNDI. This is because not all income generated from production in the UK goes to UK residents. Non-UK residents own many of the assets employed in the UK and they are entitled to the profits made from their respective investment. The NNDI accounts for this discrepancy (and is therefore a much better indicator of UK living standards), while GDP per capita does not.

As an economic researcher, I am exposed to these issues on a day-to-day basis. But, it is the reality that I will probably never be able to afford a mortgage, that my nephews and nieces wont be able to go to University without taking on at least £30K of debt, and that my children, and grandchildren, will most likely spend the majority of their lives in debt that leaves me shocked that so few (if any) politicians are raising these issues.

The recent crisis demonstrated the extent to which our socio-economic system is dependent on debt, and what can happen if the private sector becomes over-leveraged. The policy response to the crisis demonstrated how our socio-economic system is excessively dependent on debt – as we are depending on the very same tool that got us into this mess, to try and dig ourselves out. Einstein famously defined insanity as “Doing the same thing over and over again and expecting different results”.

If the current trend levels of debt to income continue to increase, it will not be a question of if we’re at risk of another crisis, but when it will occur. More politicians and media correspondents need to start looking at our dependence on debt, and how this has manifested into an extremely unhealthy relationship. Efforts needs to be redeployed toward finding new ways to increase employment and incomes without increasing the total level of debt.

Please sign our petition to tell the future Prime Minister of the UK that money creation should only be used in the public interest. And if you’ve signed it already, share it with your friends on Facebook and Twitter.