Back to Archive![The fiscal benefits of a digital pound]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

1 May 2013

How Payments are Made

5. Transferring money from one account to another

Within a bank

So far we have shown how banks create the numbers that appear in our bank accounts. These numbers are referred to as ‘bank deposits’. At the moment the newly-created money is simply sitting in Robert’s account, but naturally Robert will want to spend the money. What happens when he does?

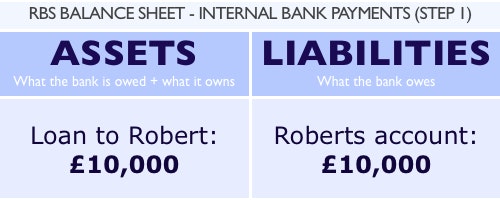

In the example above Robert borrowed £10,000 in order to buy a car. Once the loan was granted, Robert’s bank’s balance sheet appeared as so:

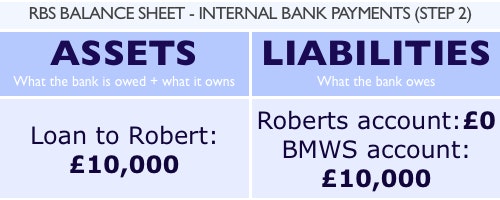

Being a fan of German engineering, Robert picks out a car which is on sale at a BMW dealership. In order to purchase the car, Robert must transfer the money from his account at RBS to BMW’s bank account. If BMW also banks at RBS it is a very simple process for Robert to transfer the money to BMW. Robert simply instructs his bank to make a payment of £10,000 from his bank account to BMW’s account. RBS then deducts £10,000 from Robert’s account, and adds it to BMW’s account, as so:

However, what if Robert and BMW bank with different banks? Payments can then be made using cash or central bank reserves.

Cash Payments

If Robert and BMW bank with different banks Robert could withdraw £10,000 in cash and pay at the BMW dealership in person.

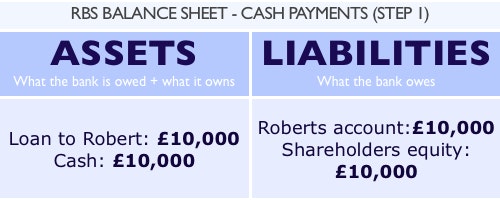

In the example balance sheets above, we’ve hidden everything that isn’t relevant to the transaction in question. But of course, RBS doesn’t only have one loan, or one customer – there will be many other assets and liabilities recorded on their balance sheet. We’re going to leave most of these items hidden for now, to keep things simple, but for the next transaction, we’re going to show the cash that RBS got from the Bank of England in the earlier example. We’ll also reveal the shareholder equity that was there from the beginning, just so the balance sheets balance.

Any cash that the bank holds in its tills legally belongs to the bank, and therefore it appears on the asset sheet of the central bank.

RBS’s balance sheet just after it has granted the £10,000 loan to Robert appears as so:

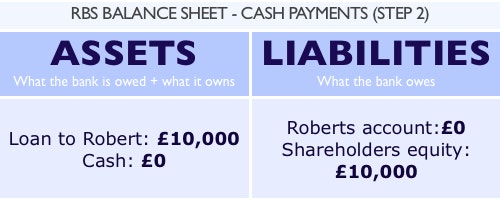

Robert then withdraws the £10,000 from his bank account:

At the point, the bank could be said to be ‘extinguishing’ its liability to Robert by repaying him in cash. Robert’s account balance of £0 shows that the bank no longer has a liability to him.

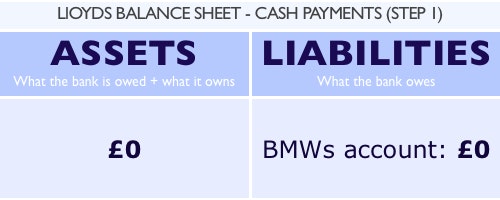

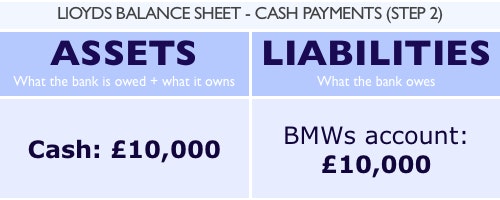

He uses the £10,000 cash to pay the BMW dealership, who banks with Lloyds. Prior to BMW placing the £10,000 in their bank account at Lloyds, Lloyds’ balance sheet looks like this:

When BMW deposit the money in their bank account Lloyds add £10,000 to their cash reserves (as they now own this cash), and increase their liabilities to BMW by £10,000:

Central Bank Reserve Payments

Of course, making payments in cash is highly inconvenient not to mention potentially dangerous. As such, payments for large amounts of money tend to be made electronically, using central bank reserves.

In the same way that you or I may have a bank account with a private bank, private banks have bank accounts at the central bank, known as reserve accounts. Reserve accounts hold a special type of money known as central bank reserves, which can be thought of as being an electronic form of cash created by the central bank. Central bank reserves are used to make payments between banks electronically. So, if Robert and the BMW dealership bank with different banks, the payment could be made by electronic transfer using these reserves.

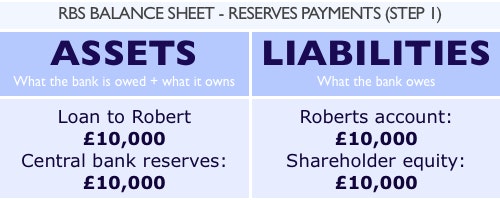

To show how banks make payments using reserves, we must first include central bank reserves on RBS’s balance sheet. We’ll also reveal shareholder equity so that the balance sheet balances. (Again, this is a simplified example with everything else hidden for simplicity).

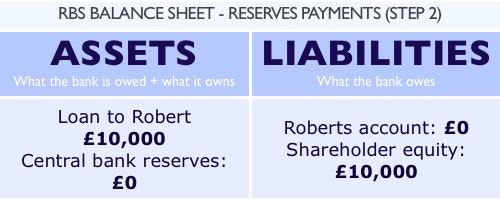

RBS’s balance sheet just after it has granted the £10,000 loan to Robert appears as so:

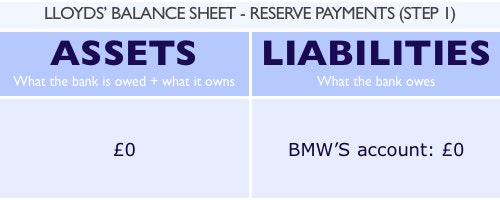

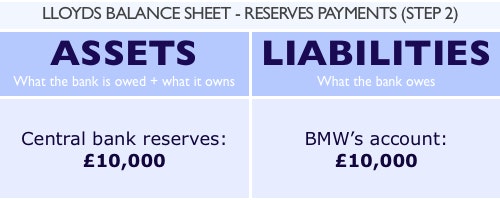

Meanwhile Lloyds’ Balance sheet is:

Robert then instructs RBS to make a payment of £10,000 to BMW’s bank account. Upon receiving this instruction, RBS reduces the balance of Robert’s account, and transfers the reserves to Lloyds bank:

Upon receiving the transfer of central bank reserves, Lloyds’ credits BMW’s account with £10,000, finishing the transaction:

The payment from the perspective of the Bank of England

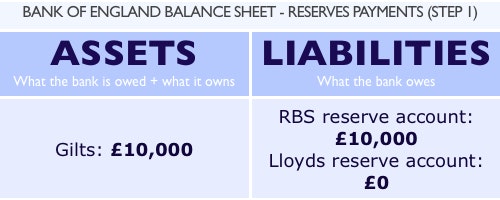

Let’s look at the same transfer of reserves from the perspective of the Bank of England’s balance sheet. With both banks banking at the Bank of England, transferring reserves between reserve accounts is the same as when two individuals at the same bank make a payment to each other; a liability to one customer becomes a liability to another customer. However, while reserves appear as an asset on the balance sheet of private banks, they are a liability of the central bank (just as your bank balance is actually a liability of a private bank). Before the payment is made from RBS to Lloyds, the reserve accounts appear as so:

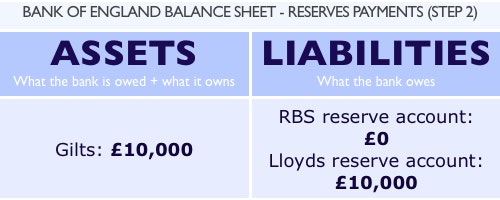

Robert then instructs RBS to transfer £10,000 from his bank account to the BMW dealer’s account at Lloyds. To do so, RBS will contact the Bank of England (electronically), asking them to transfer £10,000 from its reserve account to Lloyds bank account:

Once Lloyds receives confirmation that the reserves have been transferred, they will credit the BMW dealer’s account, as before.

For more details see:

Where Does Money Come From?

A guide to the UK Monetary and Banking System

Written By: Josh Ryan-Collins, Tony Greenham, Richard Werner & Andrew Jackson