Back to Archive![It is time to include housing prices into the ECB’s inflation index]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

16 January 2020

It is time to include housing prices into the ECB’s inflation index

The ECB’s primary mission is to maintain consumer price stability, but while doing so it omits an important item of household consumption: the cost of housing.

The ECB’s primary mission is to maintain consumer price stability, but while doing so it omits an important item of household consumption: the cost of housing. It is now time to fix this strange exception which induces biases in the design of the ECB’s monetary policy.

Central banks were made independent because their role theoretically focuses on such a narrow objective: price stability. The ECB interpreted this mandate by self-defining its objective as maintaining consumer inflation at a close but below 2%. But what if the compass driving their narrow mission is itself disoriented?

As reminded by a recent Bloomberg article, there is a vast difference between how the ECB and other central banks measure inflation, in particular when it comes to housing.

For example, the Federal Reserve measures both direct rents and the “owners’ equivalent rent of primary residence” (OER), ie. the amount homeowners would likely pay if they were to rent their own house. This ensures that the inflation index reflects the situation for all households, regardless of whether they rent or own their home.

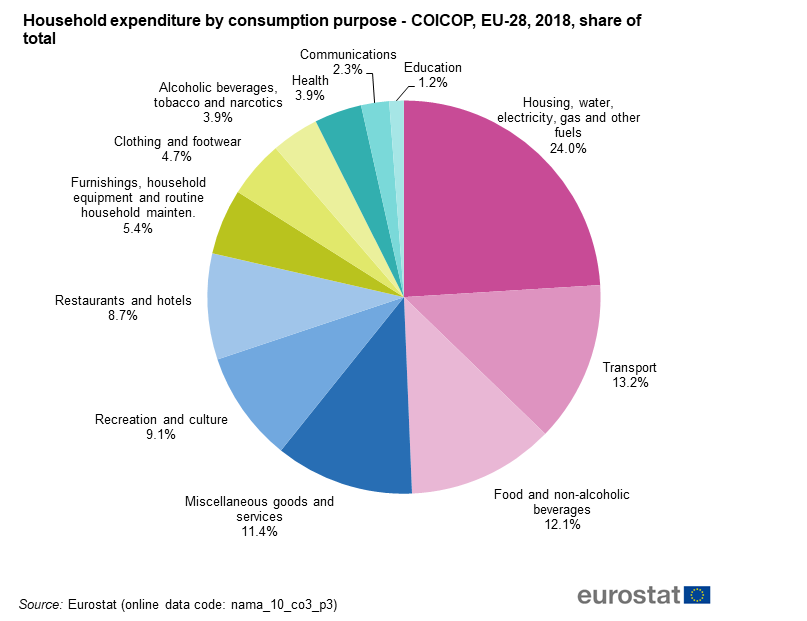

In contrast, the European Central Bank has a much narrower definition of inflation. The Harmonised Index of Consumer Prices (HICP), which is produced by Eurostat and used by the ECB, does only include the cost of actual rents (with a very low weighting of 6,5%), but not the “imputed rent” housing cost for homeowners.

This is very problematic, as this means the HIPC index used by the ECB overlooks the fact that 60 % of households are homeowners in the Eurozone. Just because 60% of households own their house don’t pay rent does not mean their housing cost is inexistent! As a matter of fact, 25% of households in the Euro area currently have a mortgage loan to repay.

This troubling feature of European statistics is even best reflected in the fact that Eurostat estimates that housing cost represents 24% of Europeans’ consumption, which is three times more the weighting of 6.5% for rental costs in the HICP index!

What does this difference mean? An obvious consequence of this peculiar exclusion is that the HICP underweights the cost of housing in the Eurozone.

Inflation is under-estimated in the Eurozone

The fact that the ECB’s inflation metrics underweight so much one of the main consumption items of European households’ budget, ultimately means the inflation index does a poor job in reflecting households’ purchasing power, or at least with a significant discrepancy.

HICP is the main indicator through which the ECB gears its monetary policy, and how its performance may be evaluated by citizens and the public. Failure in reflecting housing prices in the inflation index means the inflation index calculated by ECB/Eurostat is very likely to be lower than it actually is in reality.

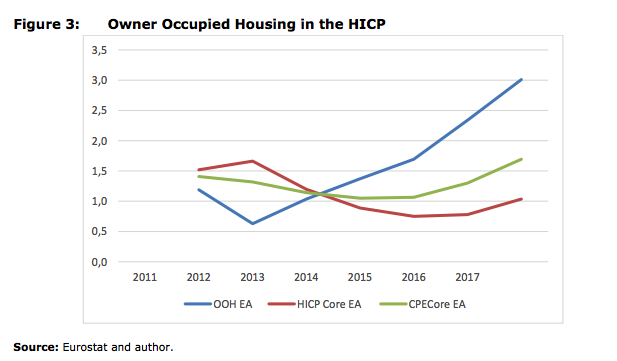

In a briefing to the European Parliament’s ECON Committee, Daniel Gros (CEPS) estimated that the HICP index would be higher by 0.3% if it included the Owner-Occupied Housing, thus making the HICP index closer to the ECB’s inflation target of 2%.

Caption: the green line represents core inflation with Owner-Occupied Housing (OOH) included.

Incorporating housing prices would improve monetary policymaking

The way inflation is calculated may sound like a very technical matter. It is not. As the ECB’s former chief economist Peter Praet once said, “The availability of these [real estate] data could have profound consequences for macroprudential and monetary policymaking and so for all euro area citizens.”

Indeed, this data gap also maintains a cognitive bias in the way the ECB formulates its monetary policy, due to the very strong interaction between housing prices and credit creation, as demonstrated by Josh Ryan-Collins (2019):

Since the majority of mortgage loans finance the purchase of existing rather than new property, the inevitable result is house price inflation. With the support of bank credit, households bid up the price of land as they compete for property in more desirable locations. This creates even more demand for mortgage debt, which then flows into existing property and so on. In other words, the supply of bank mortgage credit can be seen to create its own increased demand – via rising property prices – for ever more mortgage credit.

In the Eurozone, 35% of commercial bank loans are granted for the purpose of house purchase. This means that housing prices are more likely to be affected directly by monetary policy changes than most other budget items. It is silly that the ECB does not closely look at one of its main transmission channels, that of mortgage lending.

Instead, by overlooking housing market developments in inflation, the ECB risks propelling housing bubbles without even noticing it, for example by implementing policies such as direct purchases of mortgage-backed securities from banks (for example throughout ABSPP in the ECB’s case) which are skewed towards generating real estate bubbles, making housing increasingly unaffordable for most people.

Does it mean the ECB should have refrained from any form of monetary stimulus as some orthodox economists argue? Surely not. With or without housing prices, inflation is still too low. As pointed out by Former Czech central bankers, including properly the cost of housing in HICP would likely make the ECB’s monetary policy more counter-cyclical, as the ECB would probably have to reduce significantly the size of its stimulus right now, while it would act more decisively if there was a crisis.

A 20 years old problem

The reason behind this is both historical and technical. When the euro was created in 1998, there was no unified methodology for measuring the cost of housing across all Eurozone member states. As a result, no consensus was found on how to incorporate it into HICP, so policymakers simply decided not to include it, for the time being. Since 2000, the EU statistical agency Eurostat has worked on establishing an experimental index, the owner-occupied housing price index (OOH) and it released its first data in 2006. But 20 years later, its inclusion into HICP has still not been achieved.

In a public letter to MEP Sander Loones dated July 2018, Mario Draghi said the ECB was “from a conceptual point of view, in favour of the inclusion of an owner-occupied housing price index in the HICP, since the index’s coverage of household expenditure for consumption purposes could be improved.”

However, an assessment carried out by the European Commission published later in 2018 tells a somewhat different story. The document reveals there are strong conceptual disagreements over the statistical nature of housing prices and how to incorporate it into the HICP – which ultimately block the resolution of this issue.

On the one hand, statisticians think HICP should be narrowly constrained to monetary consumption expenditures. According to this purist view, including the net purchase of housing into HICP would distort the nature of HICP, because imputed rents are technically not monetary transactions (they are simulated price of rent for homeowners).

Historically, the ECB adopted the approach of looking at home-purchasing as an investment and not a consumption cost, therefore advocating for no inclusion of imputed rents in the HICP. However, primary residence housing can be considered as both an investment and a consumer expense. However more recently, the ECB put forward a compromise approach, by proposing to decouple the price of land from the price from the housing unit structure (ie. price of construction, maintenance and renovation). Christine Lagarde reiterated this view during last week’s press conference:

“The whole debate of whether or not we take housing into the measurements and what portion of housing and how do we dissect between the asset value of the land and the actual use of the premises. Those are tricky technical questions that we will have to look at.”

This makes sense in theory, as the value of the land (which is inherently limited in supply) is the house price component that is likely to be more sensitive to (potentially unlimited) money supply by bank lending. But the proposal entails practical difficulties, as the separation of the price of land from the price of housing is only possible via complex modelling, and not through empirical data collecting methodologies.

The Commission’s report also points to the lack of timeliness and frequency of OOH. While HICP is established on a monthly basis, data on OOH are only aggregated on a quarterly basis. For all those reasons, the Commission concluded that OOH was “currently not suitable for integration into the coverage of the HICP.”

Approximation better than omission?

However one looks at it, the way that housing prices are currently under-reflected into the HICP index is highly unsatisfactory, especially when one has in mind that shelter is often the biggest expense of households. The conceptual and practical difficulties identified by the European Commission are not viable excuses for inaction, especially after 20 years.

Although rigorous methodologies are usually preferable than hasty decisions, at this point it is clear that a better approximation of housing cost in the inflation index would be better than outright omission. We hope the ECB will strongly revise its position on this issue as part of its upcoming monetary policy framework review.