Back to Archive![ECB missed the opportunity to revise QE reinvestments]()

![PositiveMoney - Post]()

18 June 2018

The end of quantitative easing is near, long live QE!

Despite the supposed end of quantitative easing in December 2018, future reinvestments mean the ECB will purchase at least another 180 billion euros of bonds in 2019.

Despite the supposed end of quantitative easing in December 2018, future reinvestments promised by the European Central Bank mean it will purchase at least another 180 billion euros of bonds in 2019. This offers ample room for channeling the money created by the ECB more effectively.

Edit: On 13 December 2018, the ECB has confirmed it will stop purchasing more bonds while maintaining its reinvestments in place.

At Thursday’s meeting of its governing council, the European Central Bank (ECB) announced that it “anticipates” ending quantitative easing (QE) by December 2018. It is the first time that the ECB has explicitly put a possible end date to its programme. This led the euro to fall, with markets worrying that the ECB’s withdrawal from its stimulus would negatively impact the Eurozone economy.

However, from a closer look it appears that the ECB’s announcement does not quite mean that quantitative easing will disappear by December. In fact the stimulus programme is here to stay for quite a long time.

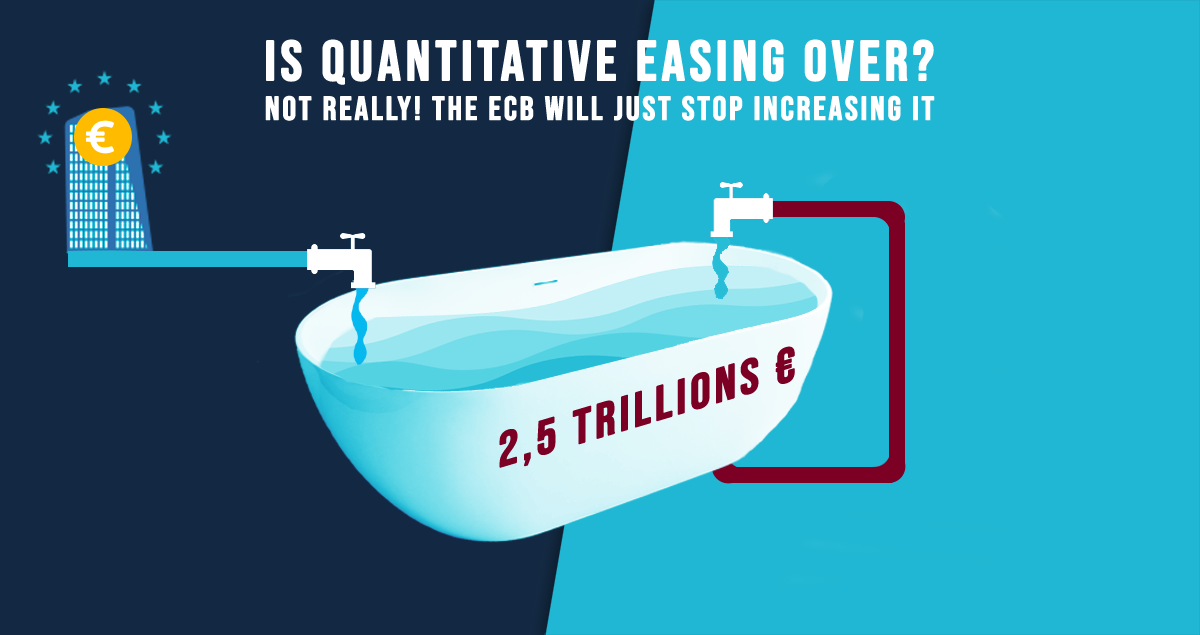

First, contrary to previous expectations that the ECB would stop QE in September, the ECB has actually prolonged it for an extra three months at 15 billions euros per month. So, contrary to media headlines, the main policy change announced yesterday by the ECB is actually an increase of QE by 45 billions, for a total of 2550 billion euros.

Second, the ECB’s communication remains extremely prudent and flexible. It talks about an “anticipation” rather than a firm commitment to stop quantitative easing. In his press statement, the ECB President Mario Draghi insisted rather loudly on the fact that this announcement was “subject to incoming data confirming the Governing Council’s medium-term inflation outlook.”

Draghi spelled out very clearly that ending QE is "s-u-b-j-e-c-t t-o i-n-c-o-m-i-n-g d-a-t-a confirming our medium-term inflation outlook" – in case you didn't read it properly…

— Ferdinando Giugliano (@FerdiGiugliano) June 14, 2018

In other words, the ECB has left room to change its mind if the economic outlook changes. And a lot can happen in six months.

But there is a more important and under-appreciated aspect of quantitative easing: the so-called QE reinvestments.

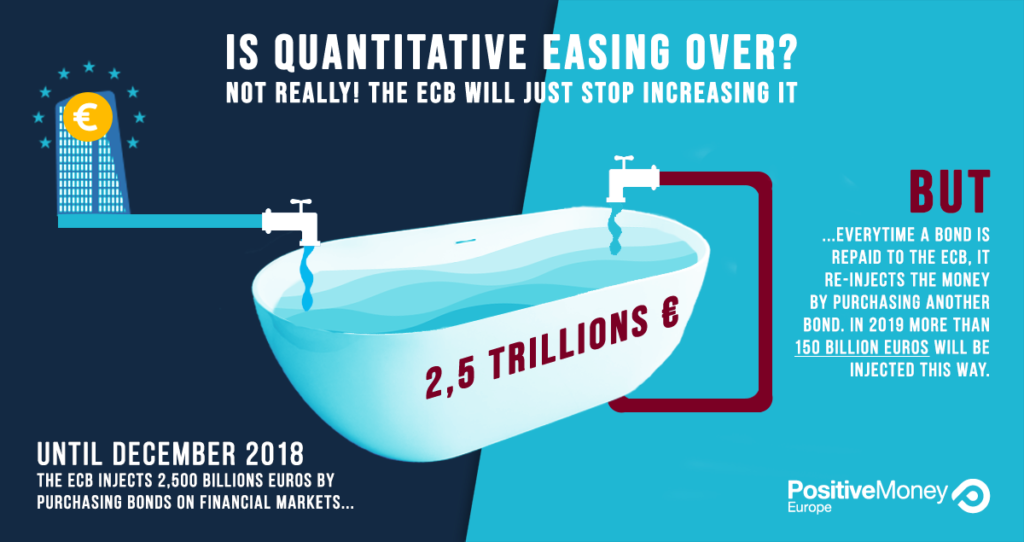

For a long time, the ECB has been very clear that the proceeds from maturing bonds held under QE will be reinvested through further asset purchases. Concretely, this means that every time a government or company reimburses, say, one million euros to the ECB, the money received is used to buy the same amount of another bond. This way, the ECB will maintain the size of its balance sheet at a very large level.

So when commentators say that QE will be stop in December, what they actually mean is that the ECB will stop increasing QE. However, the ECB will continue to operate it, although more discreetly.

The ECB will keep injecting 180 billions in 2019

This underappreciated aspect of QE may look like a detail for many, but it’s an increasingly big one.

The QE reinvestments have already started. In 2017, the ECB re-purchased about 47 billion euros this way. This amount will triple to 147 billions in 2018. Full data for 2019 is not yet available but would exceed 180 billions if the current pace continues over 12 months. In all logic, the QE reinvestments are expected to grow over the years, since the average maturity of the bonds held by the ECB is around 6-7 years.

So, while a lot of digital ink is being wasted to discuss the alleged “end” of quantitative easing, the reality is that the ECB will maintain a very large degree of stimulus beyond December 2018. Yesterday, the ECB reiterated that it will keep doing so “for an extended period of time.” In theory, this could mean “permanently”.

QE ends, long live QE!

Whether you like it or not, quantitative easing is not going away. It has become an ongoing policy instrument of the ECB.

In this context, the proposals that Positive Money Europe has been making through our QE for People campaign are still extremely relevant. Future QE reinvestments offer an opportunity for the ECB to finally channel quantitative easing towards the real economy and the green transition instead of bluntly purchasing whatever the market offers.

For example, the ECB could decide to purchase more green bonds instead of bonds from questionable sectors such as gambling, fossil fuels, pharmaceutical companies and carmaking. It could even add new eligibility rules for sovereign bonds, by giving preferential treatment to bonds issued by the European Investment Bank or any “green sovereign bond” issued by a member state. Both approaches would contribute to supporting the EU’s ambitious plans for enhancing sustainable finance and speeding up the energy transition.

Last but not least, the QE reinvestment phase also means that it is not too late to finally include Greece in QE (contrary to what Yanis Varoufakis said). Indeed, when greek bonds (finally) become eligible to QE, the ECB could easily buy them instead of other categories of bonds such as securitized mortgage loans and corporate bonds. This would provide a timely support for Greece in exiting its adjustment programme and returning to the markets.

Better late than never, we can make QE work for people and society!

Credit picture: European Central Bank