Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

10 November 2015

Can public money creation work? Some answers from Canadian history

The theoretical and policy arguments for monetary reform are becoming more accepted by economists and establishment figures.

The theoretical and policy arguments for monetary reform are becoming more accepted by economists and establishment figures. The financial crisis blew apart the idea that deregulated private money creation by commercial banks leads to more efficient outcomes and allocation of capital, as has been noted by Martin Wolf of the Financial Times and Lord Adair Turner amongst others. Yet there are few examples of how public money creation – and its variants – can support economic growth without causing negative side effects, not least inflation.

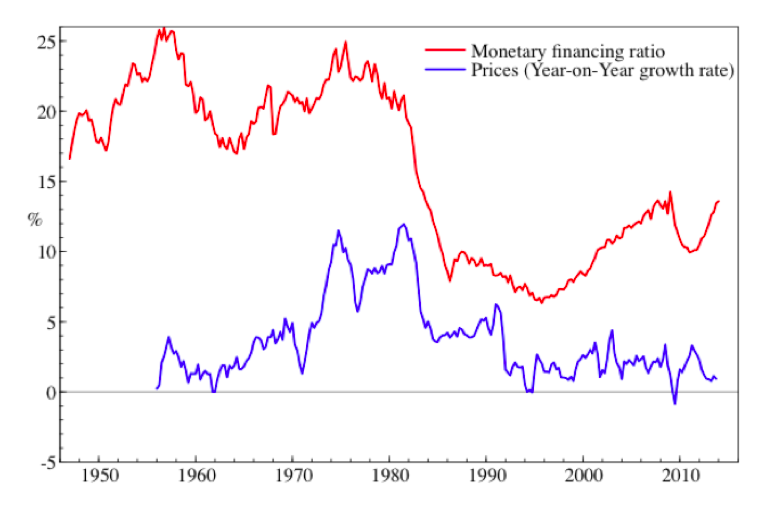

In a new working paper, I examine the case of the Bank of Canada (the Canadian central bank) in the 1935-1975 period, perhaps the most interesting example of public money creation in the 20th century in the English speaking world. Throughout this period the Bank of Canada engaged in significant direct or indirect monetary financing of government debt. In other words, the central bank created new money that was credited to the government’s account either via purchase of government bonds or direct lending. On average about one-fifth of government debt was financed and held by the Central bank, with all interest returning to the state (figure 1).

This monetary financing supported the Canadian state to recover from the Great Depression, fight World War II, enable post-war reconstruction and, in the 30 years following the war, enjoy the longest period of economic growth and high employment in its history. The Bank also created one of the worlds’ largest industrial development banks for the financing of small and medium sized enterprises (SMEs), eventually providing a quarter of all loans to SMEs, again funded via public money creation.

It is a remarkable story and one few economists or economic historians have examined. Even more remarkable is the fact that this vast monetisation program did not prove to be inflationary. As can be seen in figure 1, there is no relationship between the growth rate of consumer prices and the ratio of debt held by the Bank of Canada or the government. An econometric analysis of the relationship between monetisation and inflation and again found on evidence of a significant correlation- rather Canadian inflation was mainly influenced by U.S. inflation.

Interestingly the Bank of Canada was created in the mid-1930s not to support the financial sector but in response to a perceived failure of the banking system to provide sufficient credit to farmers suffering in the Great Depression. It was given a strong public service mandate and required to make interest-free loans to the government and municipalities for infrastructure. Which it duly did up to the mid-1970s. At this point, monetarist theory took over and the Bank sold off vast quantities of government debt to private investors.

Canadian monetary reform campaigners COMER recently hired a high profile constitutional lawyer, Rocco Galati, to sue the Bank of Canada for reneging on this commitment.

Whatever the outcome of the legal case, the example of Canada is a great reference point for monetary reformers. The Bank of Canada did not follow the prescriptions of mainstream monetary policy: it was not fully ‘independent’ of the government, it had a wide mandate focussing on full employment, support for small businesses and industry and the reduction of government debt and it used a number of different ‘tools’ including credit guidance and ‘moral suasion’ to influence the commercial banking sector.

At a time of high private and public debts, deflation and stagnant growth, monetary policy makers would do well to study the Canadian example and see how monetary financing is possible and has been successful in creating a vibrant and stable economy.

Download the working paper here.

Citation: Ryan-Collins, J. (2015) “Is Monetary Financing Inflationary? A Case Study of the Canadian Economy, 1935–75.” Levy Economics Institute, Working Papers Series, no. 848

[1] ‘Monetary financing ratio’ is the proportion of total public debt held by the Bank of Canada or government, sourced from Canadian Statistics, CANSIM Table 176-022, http://www5.statcan.gc.ca; Prices are the YoY growth rate of the Canadian Consumer Price Index (2010=100) from the OECD (2010) Main Economic Indicators: http://www.oecd.org/std/oecdmaineconomicindicatorsmei.htm