UKEU

18 February 2026

October 9, 2023

Inflation, often met with high interest rates by central bankers, exerts mounting pressure on households. However, this approach fails to address the root causes of inflation and may hinder long-term price stability by limiting investments in the green economy. It is time for a revaluation of economic policies to ensure price stability in the face of climate change and the energy transition.

Inflation in the UK has skyrocketed in the last two years, and remains stubbornly high; with food price inflation still in double digits. The Bank of England (BoE) has hiked rates 14 times since December 2021, when the cost of borrowing stood at a record low of 0.1%, to its current level of 5.25%. Raising interest rates not only hampers green investments by inflating the costs of financing renewable energy projects but is also an inadequate tool for tackling current sources of inflation. It pushes people into increasingly precarious financial situations while benefitting financial giants, with major banks amassing nearly £30 billion in profits in the first half of 2023.

Tackling Fossilflation and Climateflation

Fossilflation is inflation that is primarily caused by fossil fuel-related energy price shocks. Likewise, climateflation is the climate crisis driven by more frequent and severe fossil-fuel-driven extreme weather events disrupting our food supplies, sending their prices soaring. The European Central Bank (ECB) predicts a 50% increase in food inflation by 2030 due to global warming.

Renewable energy projects require substantial upfront capital, rendering green investments highly susceptible to interest rate hikes. This raises borrowing costs, posing challenges for green projects to secure the necessary funding. It follows from this that speeding up the energy transition will be an important part of the solution to controlling fossilflation and climateflation. Green investments can reduce the exposure of the UK economy to future bouts of fossilflation by providing more lending to retrofit commercial buildings and homes to make them more energy efficient, to help bring down bills, and for clean energy projects. Additionally, such investments can also help to address climateflation. Rate hikes cannot address fossilflation, corporate profiteering or any of the supply-side causes of inflation.

Green Investment Gaps

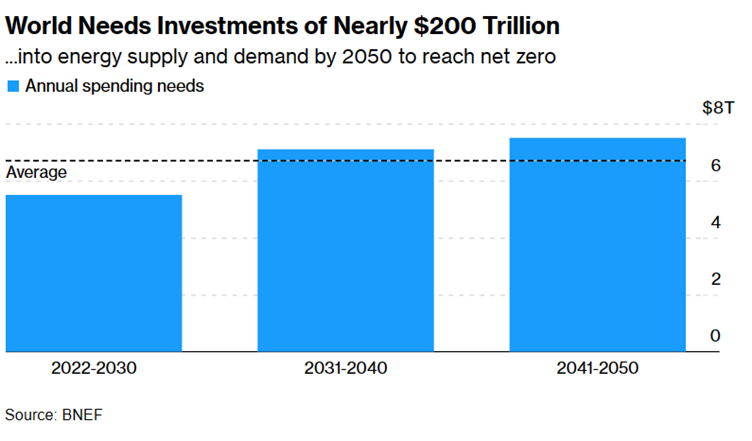

Despite the growth of the renewable energy sector, there is still a gulf between present and needed investments. Unfortunately, both public and private investments have fallen short of requirements, with only $1.1 trillion spent on related initiatives last year, while an estimated $6.7 trillion is needed annually to achieve net zero by 2050. Central banks have a major role to play in creating the conditions to spur investments in these sectors. The time-sensitive nature of climate change means that delays in adopting green technologies can slow down the growth of renewable energy industries, which will not only exacerbate environmental issues but also jeopardise long-term price stability by prolonging our dependence on fossil fuels.

Green policy options for central banks

The good news is: we can make green investments cheaper. One proposal to make green investments more affordable is to offer lower interest rates for low-carbon projects. Monetary policy can ‘safeguard’ green investments from interest rate hikes by offering preferential refinancing rates for clean investments which can introduce more suitable price dynamics and safeguard long-term financial stability from climate-related risks. Various instruments, such as green refinancing schemes, green asset purchase programs, and green-tiered reserve requirements, can be employed. Central banks can directly influence private bank credit allocation through lending and credit guidance.

Is green credit guidance the answer?

Green credit guidance can direct finance towards net zero goals and Megan Greene – the newest member of the monetary policy committee which sets interest rates – has previously spoken in favour of this. Additionally, factoring environmental risks into lending decisions can reduce exposure to stranded fossil fuel assets which are crucial aspects of green credit policies.

The Bank of Japan (BoJ) has been “providing zero-interest financing to lenders supporting action to address climate change” since early 2022, which aligns with price stability and financial stability mandates. Christine Lagarde of the ECB has also put green credit guidance as one of her top priorities for her presidency at the bank.

The UK could adopt a similar scheme by repurposing the Bank of England’s Term Funding Scheme (TFS) to provide cheaper funding to banks for sustainable investments. Interest rates for TFS green credit lines to banks could be set at 0%, or in all cases below the Bank rate, ensuring lower costs of green credit. The refinancing rate could even be made negative, with the condition that commercial lenders pass on a predefined rate discount to retrofit borrowers, offering green loans to households and businesses at 0% interest. This ‘dual interest policy’ aligns with the broader ‘green credit guidance’ framework.

Fiscal policy is also required for price stability and must lead the way on the ‘green transition’. The U.S. Inflation Reduction Act illustrates how tax incentives and government programmes play vital roles in promoting sustainability-focused projects and is a key advancement in this regard. When Rishi Sunak seeks to drain “every last drop” of North Sea oil, it undermines every monetary policy the Bank of England may pursue.

However, there are many uses and abuses of green finance. Despite green lending schemes, certain credit practices, like those of the People’s Bank of China (PBOC), favour coal production, which risks normalising extractive behaviours in the green economy, such as profiteering and ‘’greenwashing’’. The question of which investments qualify for the lower interest rate, and whether they are genuinely sustainable requires the establishment of a clear green taxonomy. The success of green credit guidance policy in France and Japan indicates that state-driven policy directions, aligned with green industrial policy objectives and ‘missions’, can be effective.

Green credit guidance should not be seen as a ‘silver bullet’, but part of a holistic strategy to discourage ‘dirty’ investments while boosting both public and private green finance. A central bank that does not address climate risk is failing to do its job. Given today’s challenges it is difficult to argue that green credit policy is any less important for the future than export finance was in the second half of the 20th century.

Sign-up to our mailing list or follow @snya92 on X (formerly known as Twitter) for more regular updates on our work fighting for a money and banking system that enables a fair, sustainable and democratic economy.