Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

18 March 2021

The Treasury and the City – still too close for comfort

Despite all the wreckage to the economy from the financial crisis over 10 years ago – today major banks and their lobbyists continue to have the direct ear of the Chancellor and top officials at the Treasury.

March 18, 2021

Despite all the wreckage to the economy from the financial crisis over 10 years ago – today major banks and their lobbyists continue to have the direct ear of the Chancellor and top officials at the Treasury. This erodes public trust and widens our demoractic deficit.

The revolving door between politicians, the City of London and regulators is by now well known. There are a litany of examples of prime ministers, Chancellors and regulators revolving back and forth between the financial sector and whitehall. The current Chancellor Rishi Sunak, and his predecessor Sajid Javid, both came from banking before entering No 11. and Javid seamlessly returned to a top job at JP Morgan rather than continue in public office.

For decades politicians have treated the City as the UK’s golden goose – praising the contributions of a sector that was primed to fill the gap left by deindustrialisation which decimated the economic fortunes of many parts of the UK. Successive governments have promoted and protected the sector. We saw the extent of this with the 2008 bank bailouts totalling £137 billion of public money to stabilise the banks and £1 trillion worth of state backed financial guarantees. This cosy relationship between the City and government left a huge blind spot to the recklessness and greedy habits of bankers searching for ever more profits. The failure to spot systemic failures was clear as regulators and credit ratings agencies overlooked and even endorsed the risky behaviour of banks.

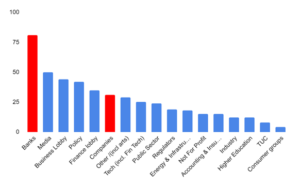

Fast forward 12 years and there is no doubt that the culture of quid pro quo is steadfast. Chart 1 below shows the disportionate influence of banks and the wider financial lobby upon the Treasury, especially when compared to other sectors and groups in our economy.

Chart 1: Number of lobbying meetings with the Treasury (Jan to Sept 2020)

Source: Data drawn from HMT ministers’ meetings, hospitality, gifts and overseas travel – GOV.UK (www.gov.uk) and Open Access UK (transparency.org.uk). Note: Categories are broad and include both individual meetings and group meetings or roundtables. The category ‘Policy’ refers to both central, local government and specific policy area meetings. ‘Business Lobby’ also includes SME bodies, Trade associations and professional bodies.

Banks had 81 out of a total of 464 meetings with the Chancellor and top Treasury officials during the first 9 months of 2020 for which the latest data is available. This is by far the sector with the greatest access to the Treasury despite an ongoing health emergency. Taking both banks and finance lobbyists together (red bars) these meetings account for a total of 25% of meetings dedicated to the financial sector. While certain major banks had more meetings than others. HSBC, Barclays Plc and Black Rock were amongst the Treasury’s top 10 lobbyists in 2020. In sharp contrast the Not For Profit (NFP) sector had only 15 meetings; The Trades Union Congress (TUC) had 5 and consumer groups just 4. This is a deeply worrying trend given the degree of financial hardship the pandemic has heaped on the everyday lives of people. Loss of jobs, mounting debt, worsening inequality and wellbeing should be the priority for the Chancellor.

This all shows that the interests of the government and the City are dangerously blurred. This results in prioritising the financial sector over the needs of the rest of society. In the last few decades the growing size and complexity of the financial sector ensures that the government will always step in to prevent any disruption or collapse. When the pandemic hit, the Bank of England swiftly resumed quantitative easing (QE), which involves creating new money to purchase government bonds and corporate assets from financial institutions, in order to calm markets. Yet, the government has only extended loans not grants to small and medium sized businesses forcing them to take on unsustainable debt. Similarly, people relying on furlough or the £20 universal credit top up have had to wait numerous times to be told if their support would be removed, adding to their financial distress.

This kind of uncertainty has not been the experience of the financial sector. In this month’s budget the Chancellor devoted a large chunk to soothing market fears about the national debt with assurances it will be a priority for the government. While hidden in the details were £4 billion of cuts to unprotected government departments, and a measly 1% pay rise to NHS workers who have been our frontline lifeline this past year.

There is growing research to show that beyond a certain size the financial sector can be harmful to the economy. The so-called Finance curse refers to our over dependence on the financial sector which has become too big and powerful, and tends to extract from the rest of the economy. The role of financial markets should be to help people build their lives and raise investment for the productive economy. Today it is speculative, debt-fuelled and addicted to inflated asset prices. This is why Positive Money has been calling for greater scrutiny and civil society voices to be part of the post-Brexit financial services regulatory system.

The government’s role is to regulate and ensure the financial sector serves us – not the other way around. Failure to do so is eroding public trust and widens our democractic deficit. Rather than being a captive audience for the banks, the Treasury should lend it’s ear to the voices of the public. That way the issues that matter most to the public from wellbeing to climate change, are prioritised over the profits of the financial sector.