Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

29 August 2018

Ending the Fiscal-Monetary Tug-o-War (NEF and IIPP)

The UK’s two most influential economic institutions are pulling in opposite directions.

The UK’s two most influential economic institutions are pulling in opposite directions. History suggests it’s time for the Treasury to take advantage of the fiscal potential the Bank of England affords it.

Ever tried walking forwards with your right leg, whilst trying to walk backwards with your left? How long do you think it would take before you fell flat on your face? Yet in some ways, that’s what comes to mind when thinking about our economic policy making.

For some time now our two most influential economic institutions – the Bank of England and the Treasury – have been pulling in opposite directions. The Bank has tried to do its job of boosting aggregate demand (spending), but the Treasury has been running fiscal austerity, which has the opposite effect.

The great irony is that through its monetary policy stimulus the Bank of England has opened up significant ‘fiscal space’ for the Treasury. ‘Fiscal space’ is a term used by the International Monetary Fund (IMF) to describe the extent to which national governments can take on more public borrowing without harming their economy). This begs the question whether the Treasury has acted irresponsibly by not taking full advantage of the fiscal potential the Bank affords it?

Without fiscal cooperation, the Bank is left trying to stimulate the economy on its own by indirectly influencing the borrowing and spending behaviour of the private sector. To this end, the Bank has lowered interest rates to historic lows, and has injected £445 billion and £125 billion of new money through so called Quantitative Easing (QE) and the Term Funding Scheme (TFS), respectively.

In doing so, the Bank has helped keep the economy afloat – but at what cost? Standalone monetary policy has reduced the number of safe assets in the market, supported more risk taking, encouraged households to take on more debt (to record levels), fuelled asset price bubbles, and promoted inequality. To boot, very little of the new money created by the Bank has trickled down into productive investments and household incomes.

In fairness to the Bank, it has kind of been thrown under the bus by the Treasury – with monetary policy stuck doing most of the heavy lifting of stimulating the economy. The Bank’s recent rate rise exposes a dangerously outdated approach to how the government conducts economic policy. Indeed, with interest rates at their ‘effective lower bound’ there are growing concerns that policymakers aiming to keep another recession at bay are running out of ammunition.

New research by NEF and the Institute for Innovation and Public Policy (IIPP) suggests that it doesn’t have to be this way. Historically, central banks and treasuries have successfully cooperated – in different ways – to help tackle some of the biggest socio-economic challenges of their time.

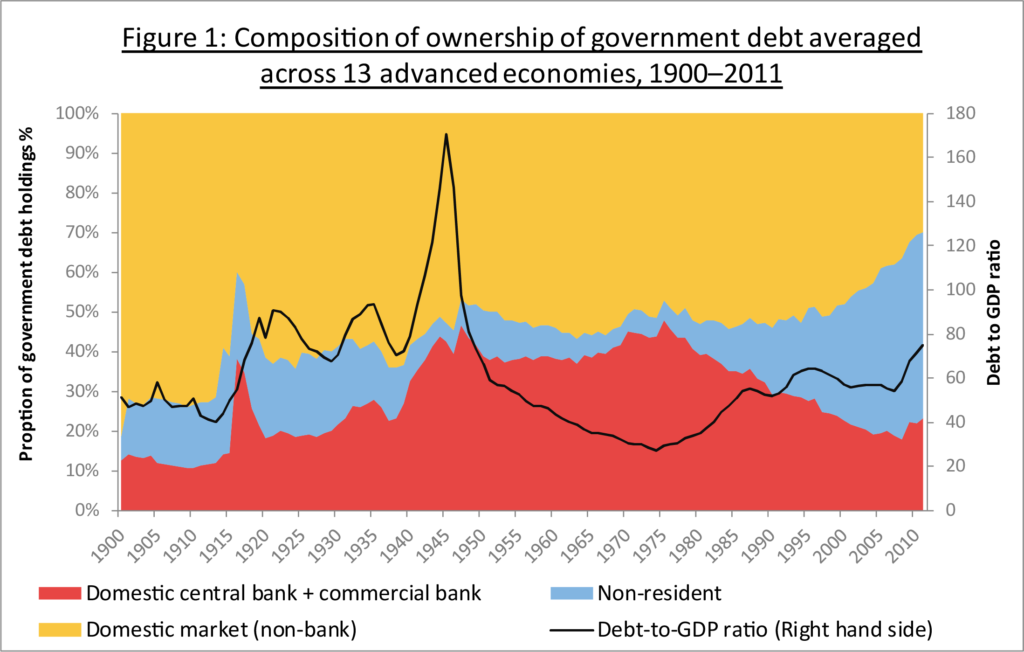

By reviewing IMF data for 13 advanced economies from the 1930s to the 1970s, our research demonstrates that Treasuries cooperated with central banks and commercial banks to help finance government expenditure. In fact, for the 30 years following World War II, almost half of government debt was held by these monetary institutions.

Notable examples include the US Treasury in the 1930s, which used the Federal Reserve Bank to help finance the publicly owned Reconstruction Finance Corporation — at the time the world’s largest bank — to support Roosevelt’s New Deal Policies to help the US out of the Great Depression.

The central bank of Canada also used monetary financing to capitalise an Industrial Development Bank in 1945 which went on to support small and medium sized enterprises across Canada for the next 30 years, providing almost a quarter of total domestic bank lending to businesses by the 1960s.

Figure 1: Composition of ownership of government debt averaged across 13 advanced economies, 1900–2011

Source: Author’s calculations based on IMF data

But how did they manage to do all this? Central banks co-ordinated with fiscal authorities to help realise public objectives – their mandates went well beyond the narrow focus of low but steady inflation.

It is true that in the absence of an international system of exchange rates and capital controls, the policy context is currently different to the immediate post-war period. Today, international markets may react negatively to stronger fiscal-monetary coordination potentially leading to increased interest rates and higher public net debt, which could result in cost-push inflation. However, the experience of countries like Japan (since the 1990s) and the UK (since the 2008 financial crisis) shows that risk of markets reacting in this way are low; and a good argument can be made that central banks with free floating exchange rates can control government borrowing costs.

Of course, fiscal-monetary coordination should be mindful of inflation, but if new money is directed towards productive activities (boosting the production of goods and services alongside the supply of money) then inflation becomes less of a concern. Indeed, the major incidences of high inflation in our study are more likely explained by external events, like wars, the collapse of the Bretton Woods system, and oil price shocks.

There are multiple opportunities for the UK Treasury and Bank of England to learn the lessons from the past. These hold important implications for policy makers who claim that ‘there is not enough money’ to tackle important issues like climate change, inequality and diminishing public services.

The big elephant in the room is that a monetary policy stimulus is likely to be much more successful if fiscal policy isn’t pushing in the opposite direction. But more importantly, monetary stimuli can enable fiscal policy expansion that delivers vital public objectives.

The most obvious is that through its monetary policy initiatives, the Bank lowers the government borrowing costs. Indeed, the Bank of Japan has been successfully targeting 0% interest on 10 year government loans for some time now.

Less obvious are the fiscal implications of making slight adjustments to existing QE and TFS programmes. For example, the Bank of England holds around £435 billion of government debt due to its QE programme. If the Bank of England ends up permanently holding this amount of debt, it will effectively be cancelled. This is basically what the US Treasury and the Federal Reserve Bank did in the 1930s – without triggering hyperinflation (in fact they struggled to stimulate inflation).

Another opportunity could be to make better use of the Bank of England’s existing Term Funding Scheme, where the Bank has already created £125 billion of new central bank reserves to lend (short term) to the banking system. As the banking system repays the Bank of England for these loans, the Bank could simply re-invest the proceeds more strategically for social and economic purpose.

So for now, we don’t need helicopter money or for the central bank to create any new money in aggregate, we just need the Treasury and the Bank of England to do a better job of working together – and for the Treasury to realise the fiscal potential the Bank affords it.

You can read the full report, ��‘Bringing the Helicopter to the Ground, from the New Economics Foundation (NEF) and the Institute for Innovation and Public Purpose (IIPP) here.