Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

19 July 2017

Rising asset prices are keeping the UK economy afloat. But what will happen when they pop?

The Office of Budget Responsibility (OBR) – the government’s fiscal watchdog – has released a ‘Fiscal Risk Report’.

The Office of Budget Responsibility (OBR) – the government’s fiscal watchdog – has released a ‘Fiscal Risk Report’. Positive Money welcomes its in-depth analysis, but we are concerned with its central findings.

In the OBR’s ‘base-case scenario’, in which UK GDP growth rises from 1.6% this year to 2.0% by 2020, UK households must spend significantly more than their income over the period. In fact, this growth will rely on them spending at a rate only ever seen at the very height of the last boom – not just for one year – but into perpetuity. To fund this spending, household debt is anticipated to rise back towards the 160% reached in 2008. Alternatively households will sell down assets that have risen in value. UK economic growth therefore relies on the price of financial assets – such as houses, equities or bonds – remaining at the highest level ever relative to incomes, forever:

But what if some known or unknown risk were to threaten this base-case scenario? This is exactly what the OBR has considered, and it has rightly earned praise from the IMF for considering the effect of such a shock. The OBR makes clear, ‘the chance of a recession in any five-year period is around one in two’ and that ‘since 1970, no decade has passed without a recession’. It is now nine years since the last recession.

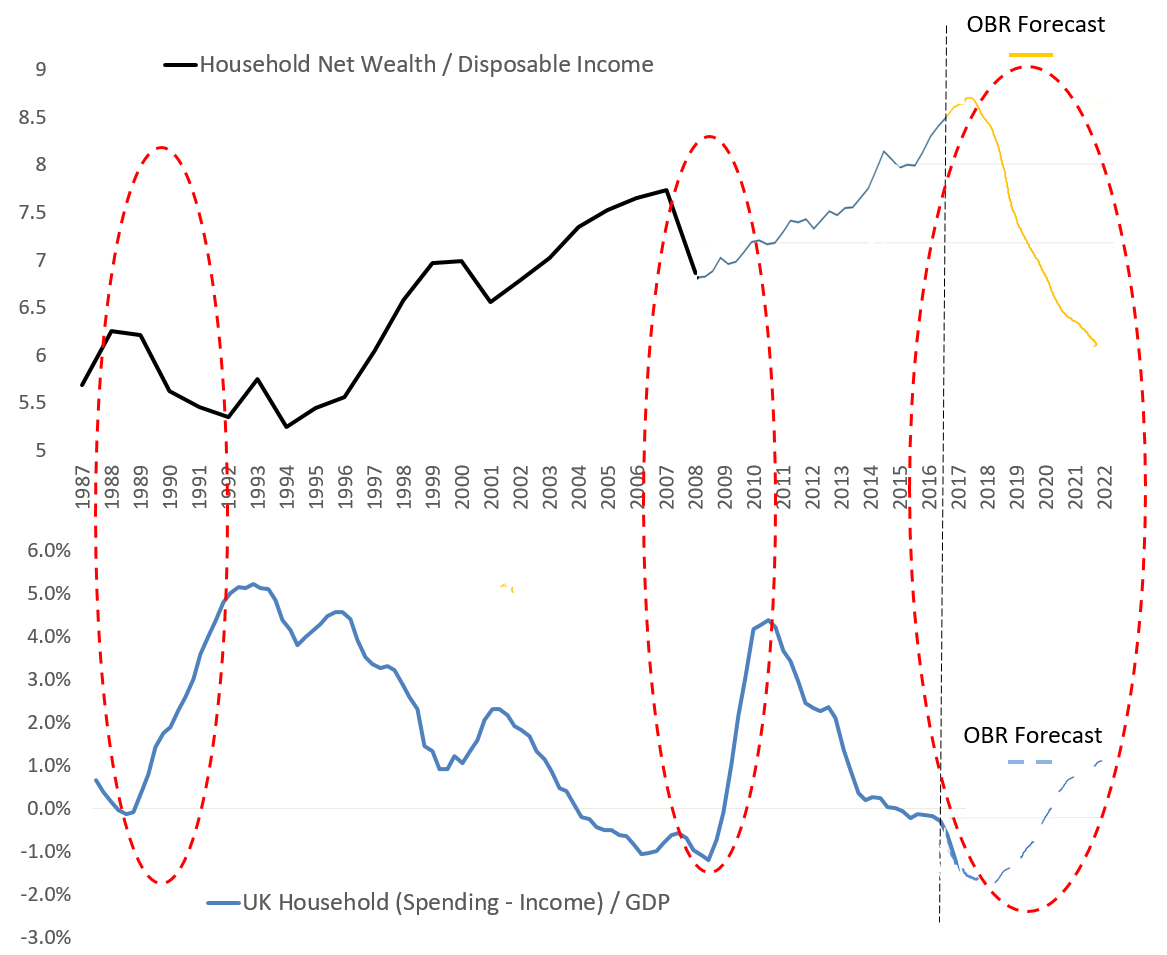

The ‘stress scenario’ the OBR imagines has real GDP falling in the same way it did in the last recession, then following a similar multi-year trajectory. As part of this stress they assume that the average house price falls from £215,000 in 2016-17 to £150,000 in 2019-20, and a sharp decline in equities of 45%. We calculate that this would wipe out almost one third of UK household wealth (i.e. a decline of £3.5 trillion vs the current ~£10.5 trillion of UK household net worth). The critical question is how households might react to such an evisceration of their savings, in terms of their efforts to then rebuild them.

The OBR’s assumed outcome is that in the event of a crisis UK households will increase their savings rate by the equivalent of 3% of GDP over four years.[1] But we fear this number will be considerably higher.

In the below charts, previous significant crises are circled in red. Despite falls in wealth much smaller than what the OBR is anticipating for its stress scenario (yellow line), household savings surged by almost double what the OBR are predicting (blue line). If history repeats, household consumption and investment will fall significantly, meaning the next recession will likely be more severe than the last. [2]

Positive Money is working towards a monetary system that doesn’t depend on ever rising asset prices and debt to achieve economic growth, punctuated with regular and debilitating financial crises. We must reform the banking system so that it does not unnecessarily contribute to boom and bust. And we must urgently develop and promote a new ‘unconventional’ policy tool of Overt Monetary Financing, or “QE for People”. In the next crisis, this tool will be the only way to ensure the government can and does spend to offset the likely collapse in private sector spending.

————-

[1] We understand the OBR’s estimate is worked backwards off a need to ensure that GDP follows their ‘stress forecast’ of -9.2% GDP in 2022 versus the March 2017 forecast; household consumption simply can’t fall further without breaking this core assumption.

[2] This would mean unemployment rising well above 10% and public debt topping 120% by 2021.