Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

26 March 2014

Creating Money – What Purpose? Adair Turner’s Latest Speech

On Friday 21st I saw Lord Adair Turner speaking at a high-profile conference at the London School of Economics.

On Friday 21st I saw Lord Adair Turner speaking at a high-profile conference at the London School of Economics. The title was simply “Creating Money: What Purpose?”

Turner summarised his recent speeches in Stockholm (“Credit, Money and Leverage – What Wicksell, Hayeck and Fisher knew and Modern Macroeconomics forgot”) and Frankfurt (“Escaping the Debt Addiction” Text of Speech | Slides).

I’ll summarise the key points here, although I highly recommend reading the full text of both speeches. They’re very clear and actually break new ground in thinking about how to use money creation to manage the economy. (Note that I didn’t record the audio of the speech, so the following is an amalgamation of what I heard and the other two speeches – not a verbatim record of what he said.) Audio of the presentation has now been released (Turner speaks from about 1 minute in until 50 minutes):

[adair_turner_lse_conference audio_embed]

Whilst Turner’s policy proposals are not as “radical”* as the Positive Money reforms, he highlights many of the issues with the modern monetary system that we’ve been warning about since 2010.

*On the point of whether Positive Money’s position is ‘radical’ – we’re essentially just arguing that the law that gives the Bank of England the exclusive right to print paper money should be updated to cover the electronic money (deposits) which is currently created by the banks. More on this here

1. How Banks Create Money

Turner started his speech by presenting the simple way in which banks create money when they make loans. When they issue a loan, the loan is recorded as an asset on their balance sheet, and they simultaneously create a deposit for the amount of the loan. This deposit is the money that appears in a borrower’s bank account, and exists as a liability from the bank to the borrower (at least until he spends the money). For the best explanation of how this works, see our Banking 101 video.

Turner stated – quite rightly – that it is fundamental to understand this process of money creation in order to understand the economy. From his Stockholm speech:

“Banks create credit, money and purchasing power. That fact is fundamental to macro-economic dynamics in any economy with a complex banking (or shadow banking) system: and fundamental to both the 2007 – 2008 financial crisis and the depth of the post crisis recession. ” (p4).

He explained how an intern of his had gone through nearly every major economics textbook currently used in universities, and found that they were almost all either ignoring this aspect, or when they did present money creation, explained it through the inaccurate and misleading “money multiplier” myth. My colleagues at the New Economic Foundation debunked this story of the banking system way back in 2011 through the book Where Does Money Come From? and our Banking 101 video course also explains what’s wrong with the money multiplier.

2. Lending to businesses is a trivial part of what banks do

The textbooks and much of current economics literature also assume that what banks do is take money from savers and then lend this money in businesses. That, in theory, helps businesses and the economy as a whole grow, leading to more employment and a better average quality of life. But this is what I personally call the “fairytale” story of banking. The reality is different:

“[M]uch pre-crisis economics and finance theory presented an inadequate account of the role of credit creation within an economy, and of the consequences of resulting leverage.

“In that pre-crisis orthodoxy, credit is extended primarily to finance new business investment. But in fact most credit in advanced economies does not serve this function, but finances either household consumption or the purchase of already existing assets, and in particular the purchase of real estate and the irreproducible land on which it sits. And at the core of financial instability in advanced economies lies, I suggest, the interaction between the in-principle infinitely elastic supply of new private credit and matching private money, and the highly inelastic supply of locationally specific land.” (Frankfurt, page 2)

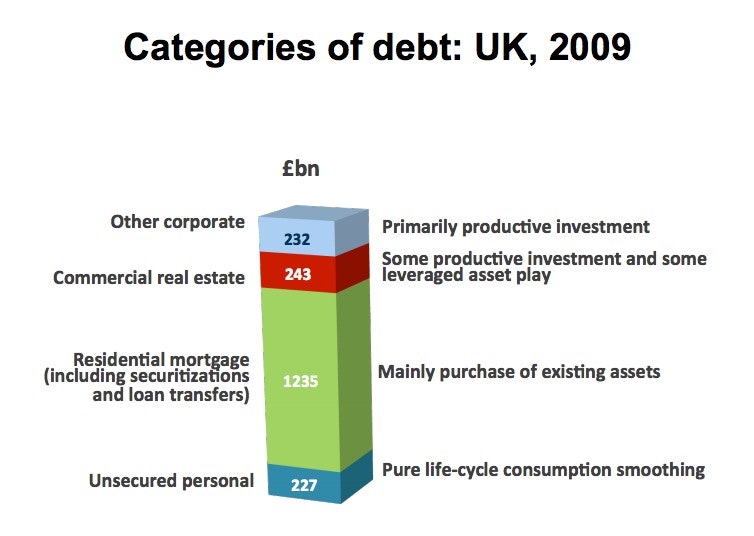

In fact, just 12% of current bank lending in the UK is to businesses, as the chart provided by Turner shows: (The top blue section, “Other corporate”, is that part that is lent to non-financial, non-real estate businesses).

3. We need growth in the stock of money to grow the economy

Turner presented the hypothetical situation in which we had a pure metallic currency, eg. gold and silver, where there was a fixed supply of money. In this situation, as the economy becomes more productive (through advances in technology and better ways of work) meaning that there is more ‘stuff’ produced relative to the existing fixed supply of money. As a result, prices fall over time. In fact, throughout much of the 19th century UK, there was stable nominal GDP (i.e. the same absolute level of spending in the economy) but as prices were slowly but consistently falling, real GDP was rising and people were consuming more.

But economists have come to the conclusion that low and steady inflation of around 2% a year will help the economy grow more smoothly. One reason for this is because consistently falling prices mean that the real value of debt keeps rising: if you borrow 10 month’s income and prices and wages fall by 10%, then you must repay 11 month’s income, plus the interest).

So to have consistent and mild inflation (eg. 2% a year) then you need either (a) a shrinking economy or (b) a growing stock of money.

4. Three Ways to Boost Money / Spending

Turner asked the question: “How can we have a growing supply of money or spending?” He then presented three options:

The government can print money and spend it into the economy. This is the “Overt Monetary Financing” proposal that he presented in his “Debt, Money and Mephistopheles” speech, and also the proposal included in our paper Sovereign Money: Paving the Way to a Sustainable Economy.

This creates new money, with no additional private sector debt (i.e. the debts of households and businesses).

We could rely on banks to create money through lending.

This creates new money, but also increases private sector debt.

The government could borrow and spend.

This does not create any new money, but it does increase the public sector debt.

Turner then made a crucial statement that (paraphrasing) “if you trusted politicians and the authorities not to misuse the process of money creation, then I believe, along with Simons, Fisher and Friedman, that the first option is absolutely the way you would want to go.” However, he then moved on from this idea, saying that we fundamentally just don’t trust government to manage this kind of power. (This is why a significant part of our paper Sovereign Money focuses on the governance that prevents this power to create money being abused by politicians.)

5. Recommendations

Again, the two full speeches are worth reading in their entirety, as there are so many ideas in them that are worth reading and considering. But Turner’s recommendations were fairly moderate:

We (or really, regulators) need to take action to constrain both the level and rate of growth of private debt.

Turner believes that the rate of growth in the level of credit provided by banks (and the consequent household debt) is a good indicator of future recessions or financial crises.

The overall level of debt determines how easy it is to escape from the recession when it actually arrives. (The paper Credit Booms Gone Bust cover this in more detail).

We should increase capital risk weights for real estate finance above the defaults in the Basel Capital Accords. This involves changing the amount of capital banks are required to hold against each mortgage or commercial property loan, as a way of countering banks’ natural tendencies to jump into (and fuel) property bubbles.

We should impose (or raise) Loan-to-value and Loan-to-Income ratios for mortgages.

We should establish banks that have a dedicated mission to lend to businesses, and which are restricted from other types of lending.

A question from the audience asked him if he was in favour of the original “100% Money” proposals from Irving Fisher (on which our book Modernising Money is based). He stated (paraphrasing) that “Some believe that that [i.e. Fisher’s proposal to stop banks creating money] is the logical endpoint of the analysis that I presented. I worry that I’m not being radical enough. I have several reasons why I’m not being that radical, but due to time I won’t cover them now.” (We were in the final minute of the session).

Further Reading:

I enjoy reading Turner’s work. He’s a deep thinker and also highlights another aspect of the current monetary system that I hadn’t noticed before. If you have time, I highly recommend reading this (in the following order):

Escaping the Debt Addiction: Monetary and Macro-Prudential Policy in the Post-Crisis World (Frankfurt, Feb 2010) Text of Speech | Slides

Credit, Money and Leverage – What Wicksell, Hayeck and Fisher knew and Modern Macroeconomics forgot

Debt, Money and Mephistopheles – a 19,000 word paper where Turner proposes that the fastest way to stimulate the economy out of a recovery would be for the government to create new money and spend it into the economy – rather than Quantitative Easing or relying on banks to create money.