Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

17 February 2014

House prices: If wages had kept up, we’d earn £44,000 more

House price inflation has been so extreme in recent years that if wages had grown at the same rate, many of us would be earning tens of thousands of pounds more each year, according to the Telegraph, 11th Feb 2014 “If salaries had risen as fast as house prices since 1997, an average couple would ...

House price inflation has been so extreme in recent years that if wages had grown at the same rate, many of us would be earning tens of thousands of pounds more each year, according to the Telegraph, 11th Feb 2014

“If salaries had risen as fast as house prices since 1997, an average couple would earn £44,000 a year more today.

In the most expensive regions the house price-earnings gap crosses the £100,000 barrier.

In the borough of Westminster in London, for instance, the average annual household’s earnings would have to be £158,000 higher today than is actually the case, had earnings risen in line with house prices in the area.

The calculations, undertaken by housing charity Shelter, are based on official, regional house prices and earnings data taken from 1997. These are then compared with equivalent data from 2012.

Shelter has an online calculator where you can check what the average earnings in any area would be had they kept up with house price rises since 1997.

But why have house prices gone up so quickly?

And can the answer to that question reveal the solution to the problem of unaffordable houses?

Where does the money to fund these ever-larger mortgages actually come from?

If you – as most people – assumed that banks are taking money from savers and lending it to borrowers, here’s a surprising fact: When we borrow from a bank, we’re not borrowing money from someone else’s life savings. It’s actually newly created money. In fact, brand new money is created by banks every time somebody takes out a loan, overdraft or credit card. (Proof)

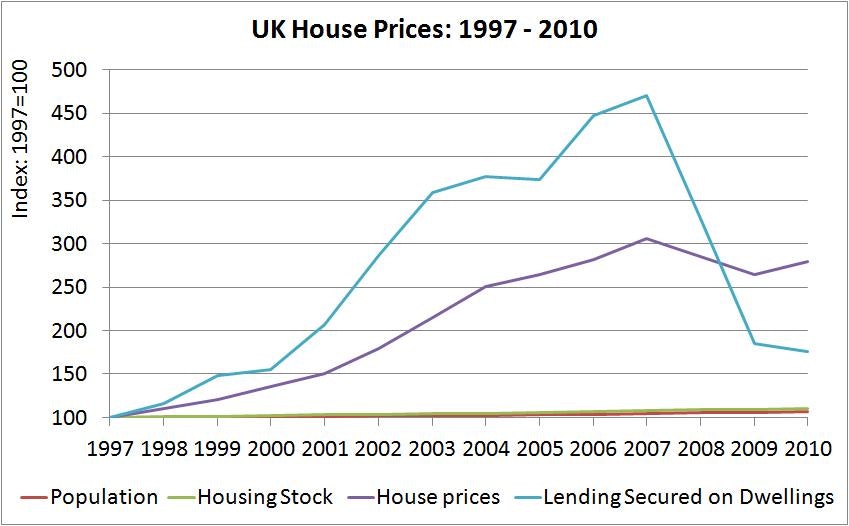

In the 10 years running up to 2007, the banks had collectively created over £417 billion of new money in the form of larger and larger mortgages, with every new mortgage creating an equivalent amount of new debt and new money.

There are many factors contributing to this increase, but the 300% increase in house prices in the UK between 1997 and 2010 would never have happened without the creation of £417bn of new mortgage credit by the banking system.

The key fundamental driver of rising house prices is the ability of banks to create money when they make loans.

Building affordable housing

According to Cambell Robb, chief executive of Shelter, successive governments have failed to build the affordable homes that this country needs. Now the shortage has reached crisis point and the only solution is to build more affordable homes.

Consensus opinion is that the UK is currently building far fewer homes than it needs to every year. Unfortunately, the private sector is unlikely to meet the demand for new houses.

As the market is failing to provide the UK with the optimum number of new houses, there is “a clear case for government intervention, at least in the short term”.

However, given the UK government’s commitment to cutting the deficit, an increase in house building financed from usual government budgets would require the diversion of funds from elsewhere. But there’s a solution whereas this need not be the case:

In our report Sovereign Money Creation, we have outlined how the Bank of England could create money in a similar way to Quantitative Easing, but whereas QE relied on flooding financial markets and hoping that some of this money would ‘trickle down’ to the real economy, Sovereign Money Creation would inject new money directly into the real economy. Find out more