Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

31 January 2014

My flat earns so much more than I do…

What does it tell us about the housing market that my flat earns so much more than I do?, asks Melissa Kite in the Guardian, 30th January 2014 Realising that my two-bedroom flat now earns more than I do was a bitter-sweet moment.

What does it tell us about the housing market that my flat earns so much more than I do?, asks Melissa Kite in the Guardian, 30th January 2014

Realising that my two-bedroom flat now earns more than I do was a bitter-sweet moment. A neighbour regaled me with the news that a standard apartment in our south London street had just changed hands for an astonishing £700,000. If true, that means my flat in Balham has put on £100,000 in the past year. It went up by a similar amount the year before, and the year prior to that.

As a freelance hack who takes time out to write books, it is no great shock that my annual income is not keeping pace with the value of my London home, which I bought over 10 years ago. But most of my neighbours, who work dawn to dusk five days a week, are also struggling to make anywhere near that amount.

You can read the whole article here.

The article explains how the gap between house prices and average earnings is producing some extremely quirky social trends, e.g. two or sometimes three generations of a family living under the same roof, as teenagers can no longer afford to leave.

To avoid “our capital city [becoming] ghetto for the rich, and our green belt a sprawl of starter homes” the author suggests that we must either control the housing market or regulate the rental sector.

We would argue that in order to fix this problem we have to first understand the key driver behind this enormous house price rise.

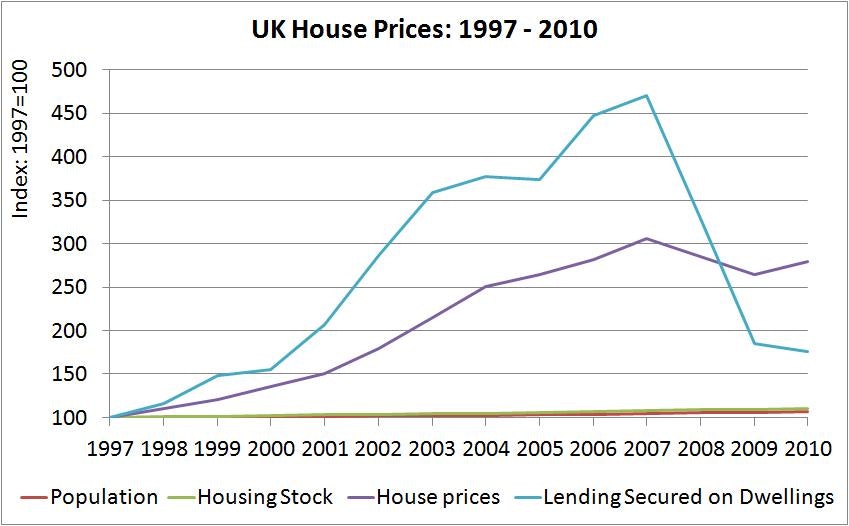

There are many factors contributing to this increase, but the 300% increase in house prices in the UK between 1997 and 2010 would never have happened without the creation of £417bn of new mortgage credit by the banking system.

The reality is that house prices were pushed up by the hundreds of billions of pounds of new money that banks created in the years before the financial crisis.

And where did that £417 billion come from? Well, when a new mortgage loan is made, the bank doesn’t borrow money from savers — banks actually create new money with every loan they make. Those numbers in your account don’t represent a pile of money in the bank; they’re just numbers, accounting entries, in the computer system of your bank.

Positive Money is advocating that new money should be created by an independent transparent and accountable public body and that it should enter the economy via the government.

In order to avoid house price bubbles and ensure affordable housing in UK we believe that we need a systemic solution – and we should start by radically rethinking how the monetary system works.