UKEU

18 February 2026

Returning to more flexible public debt issuance techniques could increase value for money and reduce volatility.

Returning to more flexible public debt issuance techniques could increase value for money and reduce volatility.

An overlooked driver of the UK’s large debt interest bill is the way in which the government issues debt.

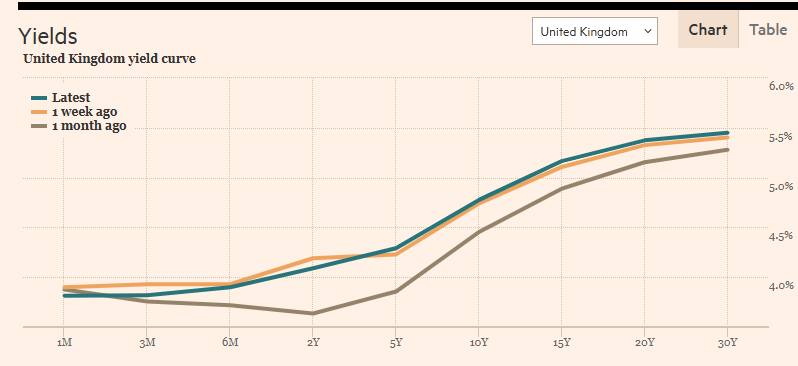

In theory, given that the UK government has no reason to default on debt issued in sterling, yields (the effective interest rate) on UK government debt (gilts) should roughly reflect expectations of average interest rates over the term of the bond, plus a term premium, which is the premium that buyers demand for holding longer-term debt, reflecting higher liquidity risk. Currently, the yield on the 30-year gilt is around 5.5%, which, unless anyone really believes that will be the average base rate over the next 30 years, indicates there is term premium making long-term borrowing relatively expensive.

UK gilt yield curve, as of 16 March 2026 (Source: Financial Times)

UK gilt yield curve, as of 16 March 2026 (Source: Financial Times)This increase in term premium largely reflects higher liquidity preference, with greater demand for shorter-term debt. This should not be surprising, given that changes in the makeup of the UK gilt market, particularly in regards to pension funds, mean that buyers are less keen on holding longer-term gilts. With interest rates where they are currently, the government could finance itself at around 4% or lower by issuing shorter-term debt, taking advantage of stronger demand for those maturities. [1]

Yet in its recent Debt Management Report for 2026/27, the Debt Management Office (DMO) published plans to issue £23bn of gilts (or nearly 10% of the total issuance) at maturities of over 15 years, locking in higher-cost borrowing for decades. While this is, thankfully, a smaller proportion than in previous years, it still begs the question as to why the DMO insists on committing to issuing set quantities of long-term gilts at increased cost for the public, rather than issuing more flexibly according to demand.

An answer to this question lies with changes to debt management techniques in recent decades. Since the introduction of the DMO in 1998, the UK has relied on an ‘auction’ or ‘tender’ system for issuing government debt. Under this system, the DMO schedules auctions for a set quantity of gilts, spread across a range of maturities, and accepts bids from buyers, which sets the yield. The DMO’s supply-driven issuance is relatively insensitive to demand and liquidity preference, as issuance is pre-determined in advance and only adjusts slowly to shifts in demand with future auction plans. As such, the DMO has continued to issue large quantities of debt at the longer-end of the yield curve, such as the 30-year. Given that the market increasingly prefers shorter-term debt, it should be unsurprising when long-dated gilt auctions end with higher yields. Unfortunately, the result is headlines about borrowing costs surging to the highest since the 1990s, which typically overlook strong demand at lower yields at the shorter end of the curve.

Prior to the establishment of the DMO, UK government debt was managed by the Bank of England, typically through a ‘tap’ system, in which gilts were continuously supplied ‘on tap’ directly to the public according to demand, with set yields (Allen, 2019). As opposed to today’s supply-driven auction system, the tap can be considered a demand-driven system. The authorities announced the price and maturity of gilts being issued, but did not set pre-determined limits to supply, and the tap was set open so individuals and institutions could buy desired amounts of gilts on demand (Tily, 2010). Gilts were available on tap at different tenures, with yields falling with maturity. The authorities could still manage the tap flexibly, adjusting issuance and pricing according to market demand (Dennis, 1982). If the private sector did not want to buy gilts at the prices offered, the government deficit would ‘automatically’ be residually financed via the sale of short-term Treasury debt to the banking sector. Such ‘residual monetary financing’ was routine and, though attempts were made to minimise it at times, it was not considered a serious problem for monetary control (Llewelyn, 1982).

The tap system meant that the composition of government debt was essentially determined by the public’s liquidity preference - or as JM Keynes put it: “Authorities make rate what they like by allowing the public to be as liquid as they wish.”(Keynes, 2013). Indeed, the tap system was advocated for by Keynes, who, later reviewing its application, noted that “it is the technique of the tap issue that has done the trick”, in enabling the ‘cheap money’ policy that allowed the UK to fight the Second World War and build the post-war welfare state without today’s debt sustainability fears, with interest rates capped below 3% for 25 years (Tily, 2010).

Keynes championed the tap system as an alternative to the preceding ‘funding complex’, which insisted on longer-term funding while restricting the supply of shorter-term debt, mirroring the ‘full funding’ rule that currently guides debt management. The problem with such ‘funding’ rules is that if the public’s preference for longer-term debt is not as high as the government’s, then rates on longer-term debt would have to be higher (Tily, 2012), as is the case today. Given the state of mainstream discourse, in which the insights of the Keynesian macroeconomic revolution appear to have been completely forgotten, this has helped fuel a perception that gilt yields are driven by concerns over government solvency, rather than the public’s liquidity preference.

Interest in reforming the tap system and a partial shift to a tender system emerged with the rise of monetarism in the 1970s and 1980s, which held that the tap system’s accommodation of higher liquidity preference made it more difficult to reduce the ‘money supply’ and therefore inflation. Despite the theoretical flaws and practical failures of their doctrine, the monetarists ultimately won, and we are still paying the price today, with a debt management system that offers poor value for money. Writing in the midst of policy debates in the early 1980s, G. E. J. Dennis presciently warned that an auction system offers less flexibility than the tap system, and risks greater volatility, with dramatic increases in yields if demand for longer-term debt is weak (Dennis, 1982). Under the present system, serious policy debate has been hijacked by short-term fluctuations in gilt yields, which have managed to have an absurd influence over long-term economic strategy.

Encouragingly, the DMO appears to be going in the right direction towards better debt management with plans to increase issuance of short-term Treasury bills. As the Bank of England also transitions from a supply-driven to a demand-driven framework for issuing reserves, it makes sense for the DMO to transition to a demand-driven framework for other public liabilities.

If the Treasury wants to rebuild Britain while quelling fears about the sustainability of public debt, it would be advised to revisit Keynes’ advice and reintroduce the tap system that provided the stable financial conditions to rebuild the post-war economy with much higher levels of government indebtedness.

[1] Though continually rolling over short-term debt is not risk-free, as long as, on average, the government is able to borrow at less than 5%, it represents better value for money

Bibliography

Allen, William A. (2019), The Bank of England and the Government Debt.

Dennis, G. E. J. (1982) ‘Monetary Policy and Debt Management’, in Llewellyn, David T. (ed), The Framework of UK Monetary Policy.

Keynes, J. M. (2013) The Collected Writings of John Maynard Keynes: Volume XXVII.

Llewellyn, D. T. (1982) ‘Money Supply in the UK’, in Llewellyn, David T. (ed), The Framework of UK Monetary Policy.

Tily, G. (2010) Keynes Betrayed.

Tily, G. (2012) ‘Keynes’s monetary theory of interest’, in Moessner, R. and Turner, P. (Eds.) Threat of fiscal dominance? BIS Papers No 65, 31 May.: https://www.bis.org/publ/bppdf/bispap65.htm