MacroeconomicsUK

16 March 2026

The dollar dominates our International Monetary and Financial System (IMFS), damaging the economies of Global South countries. In the final blog in our three-part dollar dominance explainer series, we look at how countries across the Global South are adapting and responding to this, and what the future of the IMFS could look like in light of these strategies.

In previous blogs, we explained dollar dominance and its impacts. Here, we explore how Global South countries can respond - the de-dollarisation strategies they’re using already, and how these could change the dynamics of the IMFS in the future.

Because the dollar is embedded in the international monetary and financial system (IMFS), it’s difficult to avoid many of its negative effects. However, countries have been taking steps to mitigate these impacts for years, including taking actions that can be grouped under the term ‘de-dollarisation’. De-dollarisation encompasses a wide variety of strategies to reduce the use or dependency of a country’s currency with the US dollar. This can involve reducing dollar transactions in trade, in loans, in investment, in reserve currency stores and more.

Conversations about de-dollarisation can be framed cynically as an attempt to avoid US sanctions. However, as previously outlined, dollar dominance has negative impacts for Global South countries extending far beyond current or potential sanctions. Additionally, de-dollarisation can sometimes be framed as countries seeking a new hegemonic currency to dethrone the dollar. However, this blog, and our report Beyond Dollar Dominance, instead looks at how countries in the Global South can be, and are already, employing a variety of de-dollarisation strategies to achieve greater economic sovereignty and a more multipolar world, in the face of an unjust and inequitable IMFS.

One of the most fundamental ways this can be seen is through increasing trade within the Global South, using local or non-dollar currencies.

One way this can be done is through bilateral trade agreements. For example, India has signed Local Currency Trade agreements (LCTs) with 19 other countries to facilitate rupee-based trade. Additionally, the BRICS group (Brazil, Russia, India, China and South Africa) are working towards establishing commodity exchanges that use local currency pricing. Outside of BRICS, other examples can be seen as Gulf nations such as Saudi Arabia have signalled their willingness to price oil in yuan.

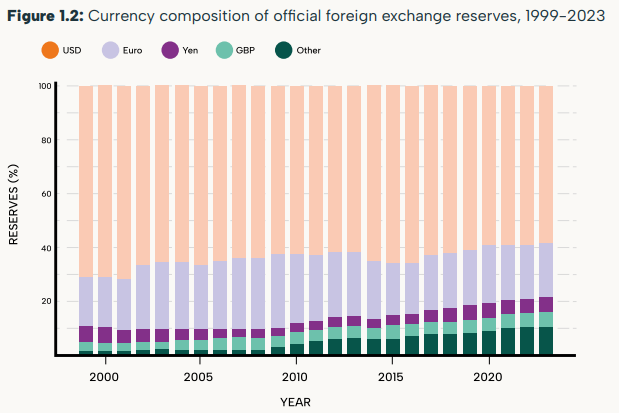

As well as for trade, countries are also increasing the number of loans they take out in non-dollar currencies, such as the growing number of loans in renminbi across the Global South. Many central banks are increasingly holding more gold, and there has been an increase in non-traditional reserve currencies like South Korean won, Canadian dollar, Australian dollar and Chinese Renminbi.

Data source: IMF, Currency Composition of Official Foreign Exchange reserves. Graph source: Beyond Dollar Dominance report

To enable and facilitate this increase in local currency trading, countries and regional groups are working to establish more regional and interbank payment systems. Payment systems can be understood as shared information systems based on financial messaging. When commercial banks across the globe want to send dollars, they rely on the dollar-based financial messaging system called SWIFT to share information as to how many dollars should be added to one account and removed from another. Creating new payment systems means avoiding having to adhere to the US legal and technological frameworks that underpin this system.

There are various kinds of new payment systems that are in use and in development. Interbank payment systems handle cross-border payments settled between central banks. Examples of new interbank systems include China’s CrossBorder Interbank Payment System (CIPS), Russia’s System for Transfer of Financial Messages (SPFS) and BRICS Pay, the system being developed by the BRICS to increase local currency use among members.

Regional local currency payment systems allow businesses and consumers in different countries to trade directly. Key examples include the pan-African Payment and Settlement System (PAPSS) and the Sistema de Pagos en Moneda Local (SML) between Mercosur trade bloc countries in South America. PAPSS enables direct, near-instant cross-border payments between participating African countries and by eliminating reliance on the dollar-dominated banking system, reduces currency exchange costs and risks, boosting intra-African trade. PAPSS is estimated to save over $5 billion a year for the African continent once fully operational.

Alongside new payment systems with a greater range of currencies, central banks across the globe have been developing new digital currencies, or ‘CBDCs’, to complement these developments.

Given the important role of public money in the economy, and against a backdrop of declining cash usage with the digitalisation of payment systems, there is growing interest in Central Bank Digital Currencies (CBDCs) or ‘public digital money’; a new form of risk-free money available to the public. Like cash, they’d be a direct liability of the central bank and be less risky than commercial money, since private banks can default or go bankrupt, and less volatile and less risky than private cryptocurrencies, which are also privately issued. Therefore, they’d be a type of public good and could play a crucial role in ensuring monetary and financial stability. You can read more on our ‘Future of Money’ page, and in the ‘Beyond Dollar Dominance’ report.

There are two main types - retail and wholesale. Retail is a digital version of cash for households and businesses to use for daily payments and as a store of value. Wholesale ones are used by financial institutions and commercial banks to settle large value interbank payments between themselves. Cross-border wholesale CBDCs have the most potential to help countries bypass the current dollar-based corresponding banking system. Reducing the need to rely on intermediaries and external currencies would reduce costs and settlement risks associated with cross-border flows, as well as reducing settlement time from an average of one to two days to instant settlement with CBDCs.

The most influential development in CBDCs for de-dollarisation and a more multi-polar IMFS however would be if these CBDCs achieved something called ‘interoperability’. Interoperability means that a CBDC issued by one central bank can be directly exchanged with another across different jurisdictions and regulatory frameworks, meaning that interoperable CBDC platforms essentially function as payment systems. Interoperability is important because it would reduce the need for multiple currency conversions and intermediaries, typically through the dollar. One interoperable digital money project developed by China, Thailand, Saudi Arabia, Hong Kong, and the UAE, is called mBridge. It is one of the furthest progressed interoperable CBDC platforms, and, if fully rolled out, could provide benefits including reduced cost, instant settlement, and improved reliability. However, many barriers to full cooperation and interoperability between the countries involved remain.

MDBs are an alternative to the Global North-based World Bank, International Monetary Fund, and other large-scale financing institutions. Examples include: The New Development Bank (NDB), established by the BRICS; The Asian Infrastructure Investment Bank (AIIB) led by China, and the Banco del Sur (Bank of the South) established by South American countries. If given more financing capacities, these banks could more easily commit to offering financing in non-dollar currencies, and potentially offer more favourable loan conditions with fewer strings attached than funding from Global North institutions, reducing current debt burdens.

Finally, there are more structural reforms to the IMFS that could help not just de-dollarisation, but a wider shift in power away from the Global North, and allow greater economic sovereignty for the Global South.

An essential first step is a comprehensive programme of debt cancellation, as the on-going debt crises across many Global South countries has deep roots in colonialism. As discussed previously, cycles of debt and unfair loan conditions from Global North institutions trap Global South countries in a cycle of poverty. Countries trapped by the dollar-centric IMFS are unable to invest in climate change mitigation despite being the most harshly impacted, and the source of materials for the Global North’s green transition. Debt cancellation has happened before, and, as a Jubilee year, organisations across the world are pushing for more in 2025.

Other necessary reforms include reallocation of ‘Special Drawing Rights’, which are reserve assets issued by the IMF, and can be exchanged for currencies like the dollar or the euro. The majority of SDRs are allocated to high-income countries who do not use them yet control 60% of total SDR allocation. This creates a disparity where the countries most in need of SDRs are not receiving enough.

Additionally, there needs to be an end to harsh economic sanctions imposed by Global North countries, like those recently seen from the US, that only deepen neo-colonial power dynamics and limit economic sovereignty.

The biggest obstacle to these efforts is of course the structural embeddedness of the dollar in the IMFS, and the political and economic power of the US and other Global North countries who currently benefit. Beyond this however, another major challenge is political will and diplomatic cooperation between Global South countries looking to de-dollarise. Expanding regional payment systems, increasing trade in local currencies, and building interoperable CBDCs all involve increased South-South cooperation, and will take extensive negotiations and regulatory alignment.

However, while countries have been using de-dollarisation strategies long before President Trump’s second term tariff increases, these developments have added new urgency. These could therefore foster greater partnership and political will to develop solutions between more Global South countries.

There are further economic benefits too. Payments infrastructure that is directly owned and controlled by countries themselves could work to reshore economic activity and, over time, help countries to diversify away from extractive, environmentally destructive export sectors. Moreover, digital public money, paired with new payments infrastructure, could offer an important alternative to the private sector-led fintech industry’s growing presence in Global South economies, keeping more money in public hands.

The de-dollarisation movement will be accelerated by the Trump administration given its belligerent stance, by pushing more countries to reconsider their financial entanglements with the US. It is becoming increasingly difficult for the Global North to justify and maintain the hierarchy of the financial system as it was built on the basis of ensuring a neo-colonial dependence on imports and financing from the Global North, that is fundamentally at odds with the rapid economic and technological development of Global South countries. Tariffs, threats, and sanctions - meant to assert US financial dominance across the globe - seem increasingly impotent against the rising tide of Global South countries asserting their right to monetary and economic sovereignty.

The dollar’s status is weakening, and given the developments in new payment systems, local currency trade, and South-South integration, this is unlikely to be a mere bump in the road. Concerted efforts to move away from the dollar would not cause a catastrophic collapse of the greenback, but instead see it relegated to a position within the currency hierarchy that is more reflective of the actual size of the US economy.

The world is increasingly multipolar and, with collective efforts, the world can move away from the unipolar monetary order of dollar dominance. However, despite the clear case for a more just financial system, this development will not happen by itself, but only as a result of countries coming together to build the necessary technological, political, and diplomatic frameworks and infrastructure. A new financial architecture beyond dollar dominance is within reach, and together we can make it a reality.

Want to learn more? Take a look at our ‘Beyond Dollar Dominance’ report, videos here, and take a look at our previous blogs explaining dollar dominance and its impacts!