MacroeconomicsUK

16 March 2026

February 23, 2024

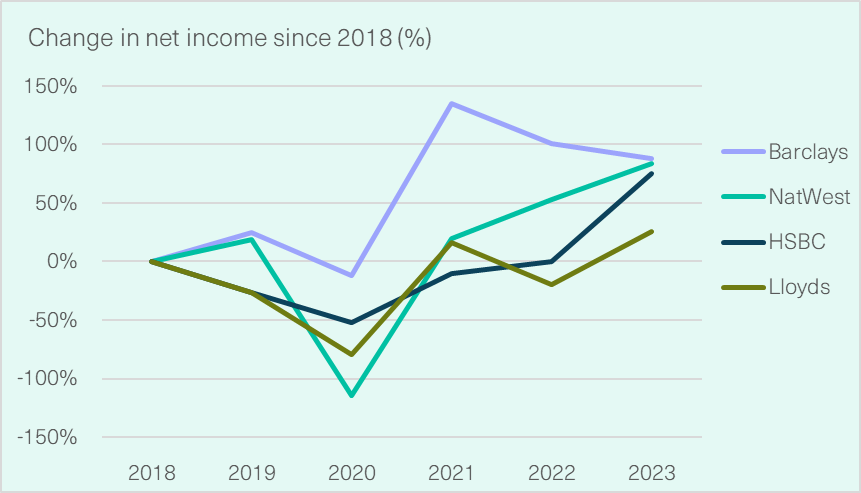

This week the Big Four UK banks — Lloyds, NatWest, Barclays and HSBC — announced pre-tax profits of £44.3 billion – an average of 66 per cent higher than their profits in 2018. Barclays had the highest percentage increase in profits, which have risen 88 per cent, from £3.5 billion to £6.6 billion.

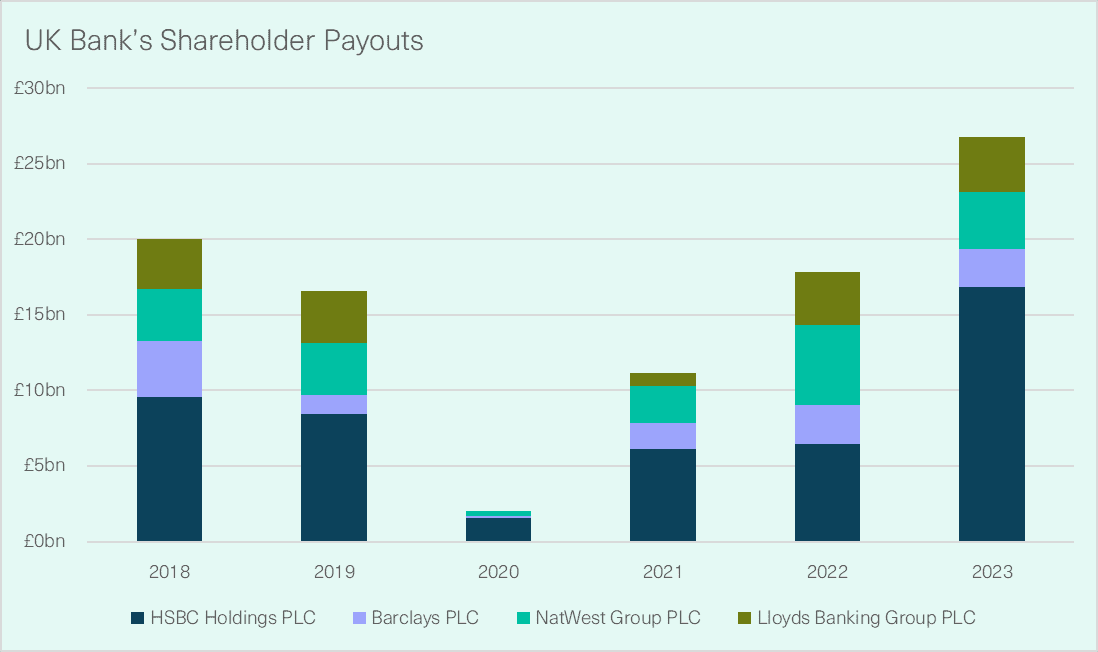

The bank’s payouts to shareholders through traditional dividend payments and share buyback schemes also increased over the same period. In 2023, the Big Four banks paid their shareholders £26.8 billion.

A key source of banks’ profits is higher interest rates. The Bank of England currently conducts monetary policy by paying its base rate of interest (currently 5.25 per cent) on central bank reserves held by commercial banks. In an analysis for the IFS, former Bank of England Deputy Governor Sir Paul Tucker suggested that banks would receive £42 billion and £33 billion in 2023 and 2024 respectively from interest paid on their risk-free reserves. The costs of this are ultimately borne by the Treasury, which has been transferring tens of billions of pounds to the central bank to cover these payments.

This mechanism, combined with banks being able to charge higher interest rates on loans to households and businesses, has boosted banks’ net interest income (NII), as they have resisted passing gains onto ordinary depositors.

These fiscal costs from higher rates could ultimately be mitigated by changes to how the Bank of England remunerates reserves, as proposed by the New Economics Foundation. But in the absence of a change to the monetary policy framework, the undesirable distributional impacts of monetary policy could also be offset by windfall taxes on banks’ unearned profits.

There is precedent for this. In 1981, when energy companies and banks were again recording record profits while the wider economy was in turmoil, the Thatcher government introduced windfall taxes on both of these sectors. As Thatcher justified it in her memoirs:

We had in November announced extra taxation on North Sea Oil and Gas profits. The question now was whether to levy a windfall tax on bank profits. Naturally, the banks strongly opposed this; but the fact remained that they had made their large profits as a result of our policy of high interest rates rather than because of increased efficiency or better service to the customer.

Replicating the Thatcher government’s 2.5 per cent levy on non-interest bearing deposits could raise around £10.5 billion today.

Alternatively, the government could simply bring the existing three per cent surcharge on bank profits in line with the 35 per cent windfall tax introduced on energy company profits — doing so would bring in an additional £14 billion from the 2023 profits of the big four banks alone.

The bank surcharge was introduced in 2015 to accompany the existing bank levy, in recognition of the need for banks to “make a fair contribution in respect to the potential risks they pose to the UK financial system and wider economy.” However, the government recently slashed the surcharge by 60 per cent (from eight per cent to three per cent), while also halving the bank levy. In contrast, the Netherlands recently increased their bank levy by 70 per cent. Simply reversing the cuts to both the surcharge and bank levy could raise an additional £3.5 billion this year at least.

A number of other European countries have also introduced windfall taxes on their banking sector. Italy made headlines last year with a 40 per cent windfall tax on the difference between banks’ NII in 2021 and the figure for 2022 or 2023, depending on which is larger. Such a levy would raise nearly £8 billion from the UK’s big four banks.

The Czech government has also introduced a 60 per cent windfall tax on bank profits exceeding 120 per cent of the 2018-21 average. Doing so in the UK would raise more than £7.3 billion from the 2023 profits of the big four banks.

Meanwhile, Spain has introduced a 4.8 per cent windfall tax on banks’ NII and net commissions above a threshold of 800 million euros. An equivalent tax would raise £4.5 billion from the big four banks’ 2023 profits.

The government has so far resisted calls for a windfall tax, claiming that banks’ exorbitant profits are ultimately good for society, as the financial services sector provides a large number of jobs. But as we’ve seen banks aren’t reinvesting their profits back into the economy — they’re squandering them on dividends and share buybacks, while ruthlessly cutting jobs and branches across the country. The Chancellor should therefore take the opportunity in the upcoming Budget to raise billions of pounds with a windfall tax on the big banks, which could be used to support the public who are paying the price of banks’ profiteering. Sign Positive Money’s petition calling on him to do that here.