Back to Archive![The fiscal benefits of a digital pound]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

1 May 2013

Introduction to Balance Sheets

Notes and coins today make up just three out of every hundred pounds in the economy.

[first]Notes and coins today make up just three out of every hundred pounds in the economy. The other ninety-seven pounds exist as accounting entries on the books of commercial banks. That means a basic understanding of accounting and balance sheets is essential in order to understand how money is created.[/first]

There is no reason to be put off by the accounting terminology; if you have ever borrowed money from a friend and left a note on the fridge to remind you to repay them, then you have already done one half of the accounting necessary to understand banking.

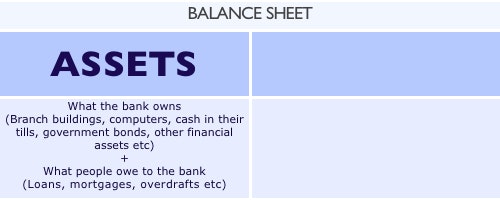

In short, a bank’s balance sheet is a record of everything it owns, is owed, or owes. The balance sheet comprises three distinct parts: assets, liabilities and shareholder equity.

Assets

On one side of the balance sheet are the assets. The assets include everything that the bank owns or is owed, from cash in its vaults, to bank branch buildings in town centres, through to government bonds and various financial products. Loans made by the bank usually account for the largest portion of a bank’s assets.

(In fact, if you lend £100 to a friend, your friend’s agreement to repay you can be recorded as an asset on your own personal balance sheet.)

You may find it counter-intuitive that a loan made by the bank is recorded as an asset; after all, once you’ve lent money, you no longer have the money, so how can you record it as an asset? However, when a loan is made, the borrower signs a contract committing to repay the full loan, plus interest. This legally binding contract is worth as much as the borrower commits to repay (assuming they will repay), and so can be considered an asset in accounting terms.

Liabilities

What about the other half of the balance sheet? This side is called the ‘liabilities’ of the bank.

Liabilities are simply things that the bank owes to other people, organisations or other banks. Contrary to the perception of most of the public, when you (as a bank customer) deposit physical cash into a bank it becomes the property (an asset) of the bank, and you lose your legal ownership over it. What you receive in return is a promise (an IOU) from the bank to pay you an amount equivalent to the sum deposited. This promise is recorded on the liabilities side of the balance sheet, and is what you see when you check the balance of your bank account.

Therefore the ‘money’ in your bank account does not represent money in the bank’s safe, it simply represents the promise of the bank to repay you – either in cash or as an transfer to another account – when you ask it to. The bulk of a typical bank’s liabilities are made up of ‘deposits’ which are owed to the ‘depositors’. These will generally be individuals, businesses or other organisations.

Deposits in a bank can be split into two broad groups: demand (or sight) deposits and time (or term) deposits. Demand deposits are deposits that can be withdrawn or spent immediately when the customer asks, in other words ‘on demand’ or ‘on sight’ of the customer. These accounts are commonly referred to as current accounts (in the UK) or checking accounts (in the USA), or instant access savings accounts. In contrast, time deposits have a notice period or a fixed maturity date, so that the money cannot be withdrawn on demand. These accounts are commonly referred to as savings accounts.

Equity

The final part of the balance sheet is the equity. Equity is simply the difference between assets and liabilities, and represents what would be left over for the shareholders (owners) of the bank if all the assets were sold and the proceeds used to settle the bank’s liabilities (i.e. pay off the creditors).

Equity is calculated by subtracting liabilities from assets. A positive net equity indicates that a bank’s assets are worth more than its liabilities. On the other hand a negative equity shows that its liabilities are worth more than its assets – in other words, that the bank is insolvent.

For more details see:

Where Does Money Come From?

A guide to the UK Monetary and Banking System

Written By: Josh Ryan-Collins, Tony Greenham, Richard Werner & Andrew Jackson