Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

9 May 2016

What are the alternatives to QE? How about money creation for the public?

Since 2010, the Quantitative Easing (QE) programme has pumped £445 billion into the UK’s banking system.

Since 2010, the Quantitative Easing (QE) programme has pumped £445 billion into the UK’s banking system. While QE may have prevented the financial crisis from sending the UK even further into recession, designed differently, this money could have reached the households and businesses that needed it the most.

Instead, QE flooded financial markets with billions of pounds and helped push up house prices. It has consequently increased inequality. Most importantly, it treats the cause of the recent financial crisis – too much private debt – as a primary solution.

QE was a missed opportunity to promote growth in the non-financial sectors, the real economy. Consequently, a number of alternative monetary policy proposals have emerged – what we call Public Money Creation.

Below we answer some of the important questions about Public Money Creation proposals that are being put forward.

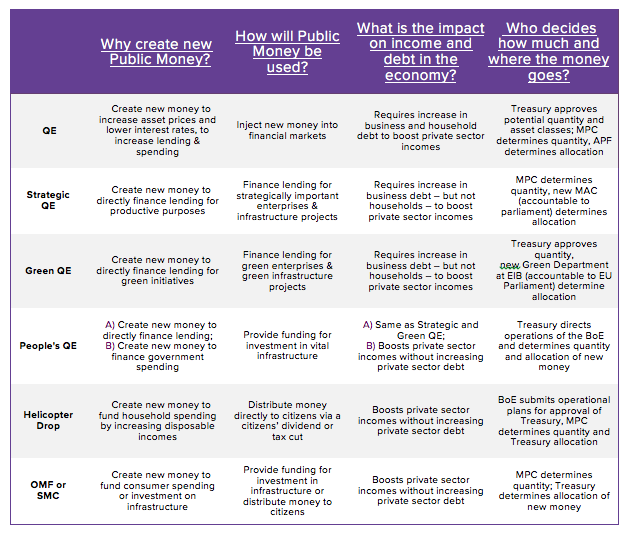

What is Public Money Creation?

Public Money Creation proposals advocate using central bank money to directly stimulate the real economy. These proposals are known as Strategic QE, Green QE, Sovereign Money Creation, People’s QE, Overt Monetary Finance and People’s QE.

Whilst they are all pose an alternative to QE, these proposals have some important differences. (We have outlined each proposal in detail in our new paper).

What is Public Money Creation for: Lending or Spending?

Certain Public Money Creation proposals involve the Bank of England creating new money that can be invested into a public intermediary – i.e. a public investment bank. The public intermediary can then lend money to businesses taking on (green) infrastructure projects, or it can lend money to green enterprises or SMEs. In this sense, credit is strategically aimed at businesses outside the financial sector, and money is lent into the real economy.

Other proposals aim to directly increase government or household spending, without the private or public sector having to take on more debt. In these proposals, newly created money is effectively spent, rather than lent, into the economy.

What is the Central Bank Money for?

When compared to QE, Public Money Creation proposals have different recommendations as to how the central bank’s ability to create money could be used. Four general approaches can be distinguished:

1) Some proposals advocate using central bank money to directly finance lending to large businesses, SMEs, social enterprises, co-operatives, and local governments.

2) Proposals that advocate using money that is newly created by the Bank of England to finance infrastructure investment (via lending or spending).

3) Proposals that advocate using newly created money to finance either a tax cut, or direct cash transfers to households, such as a one-off “citizen’s dividend” (a non-repayable grant to every citizen).

4) Proposals that offer a mix or combination of the three options above.

What is the Impact on Income and Debt in the Economy?

For there to be an increase in income, current QE firstly relies on making wealthy asset holders feel better off, which should induce them to spend and consume more. But this ultimately leads to inequality (as the Bank of England has admitted).

Secondly, QE relies on encouraging businesses and households to take on more debt. Because QE doesn’t specifically target the real economy, QE favours the current status quo – where just under 85% of new lending goes into the unproductive sectors of our economy, primarily property and the financial sector. This reinforces our dependence on household debt – and runs the risk of causing yet another crisis.

(Note: It was increased from £375 billion since the video was made to £445 billion.)

This is why certain Public Money Creation proposals involve redirecting credit, so that lending is targeted at everyday businesses and small and medium enterprises, the so-called productive sectors of the economy.

This means that households would not have to take on more debt for there to be an increase in household incomes. Businesses in the private sector would take on more debt to spend on salaries and wages – which would boost household incomes.

But this debt would also be used to invest in productive ventures (revenue generating assets in technical jargon) such as a green infrastructure project. By investing in a productive venture, over-time businesses would acquire enough revenue to pay off their outstanding debts over time and ideally make a profit to boot.

The other Public Money Creation proposals, which involve the Bank of England creating money to finance spending, increase private sector incomes without increasing the level of debt in the economy.

Money can be created for the government to spend on infrastructure projects. The government’s spending on goods and services would directly result in an increase of the incomes of businesses and households. Alternatively, money could be created to finance a tax cut or cash transfers to households, which result in direct and immediate increase of household disposable incomes.

What About Inflation?

Those new to Public Money Creation often fret that it could lead to high level of inflation or even hyperinflation, making the subject ‘taboo’.

Mainstream economic theory often suggests that inflation is the consequence of the stock of money increasing faster than the supply of goods. With more money in their pockets, people will demand more goods and services. Businesses will notice that there is a high level of demand relative to their available supply, and therefore raise the price of their goods and services, resulting in inflation.

According to this approach, increasing the amount of money in the economy faster than the supply of goods and services results in inflation.

But creating new money does not always trigger price inflation. If new money is created and spent on the production of new goods and services, then the supply of goods and services is increasing alongside demand. In this situation you have an increased amount of money chasing an increased amount of goods and services being supplied. Inflation will not take place if supply is growing consistently with growth in the stock of money.

This helps explain why many governments, as the case studies referenced in this blog demonstrate, have been able to successfully grow their economy through the careful and responsible use of money creation. Their economies were operating below full capacity, and the new money was created and allocated to the sectors that were performing below their potential.

The new money created was able to tap into the sectors where resources and inputs lay idle, therefore increasing the supply of goods and services. As supply (the production of goods and services) and demand (the creation of new money) broadly increased in tandem, high levels of inflation were avoided.

Who Gets to Decide how Much Money to Create and Where it Goes?

The above is based on the notion that money is created responsibly and for productive purposes. This is why the majority of Public Money Creation proposals suggest that there needs to be a clear institutional separation, between the decision of how much money to create and the decision of where to allocate money.

An administrative branch of the Bank of England (such as the MPC) would determine how much money to create, while a politically accountable body (or politicians) would determine where it goes.

These institutional procedures avoid elected politicians controlling monetary policy tools, and prevent unelected technocrats from gaining unwarranted influence over fiscal policy.

Decisions over how much money to create would most likely be done according to an indicator of some sort, such as the consumer price index (measurement of inflation). So if inflation was above the desired level, then no new money would be created. However, if inflation was deemed to be below the desired level (currently 2%) then new money would be created.

Why Should I Care?

Proposals for Public Money Creation are hitting headlines because people are beginning to understand that there are more effective ways to use the Bank of England’s money creating powers.

These proposals represent a realistic opportunity for central banks to use their power to create money for the majority of society, rather than a special few. They offer more direct ways to stimulate spending/investment in the real economy, that will make our economy more stable and sustainable over the long-run.