Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

1 September 2015

Money Creation: Explaining What’s Happening in China?

The current economic slump and recent stock market crash in China has got many people asking exactly what is happening in China? There are numerous theories explaining the situation, and the majority of them make valid points.

The current economic slump and recent stock market crash in China has got many people asking exactly what is happening in China? There are numerous theories explaining the situation, and the majority of them make valid points. Many analysts, however, have neglected the vast accumulation of private debt, in their explanations. This piece argues that in order to explain the current situation in China, it is necessary to understand how debt and newly created money is being used.

For those unfamiliar with current monetary systems, every time a bank makes a loan it creates new money. Similarly, every time a loan is repaid, money is effectively destroyed (for a more detailed explanation click here). When banks create new money through lending, they are increasing purchasing power in the economy. This new spending power can increase demand for goods and services. Likewise, the repayment of debt and the associated destruction of spending power can prompt a contraction in demand. This point is very well explained by Steve Keen:

“…demand and income in our money-driven economies are the sum of demand and income generated by the turnover of existing money, plus that generated by the growth of the money supply, which is overwhelmingly due to new debt…a huge proportion of demand comes from the change in debt, and that this can be negative as well as positive—that is, repaying debt destroys demand just as rising debt creates it.”

Demand and China

Up until the most recent financial crisis, China’s extraordinary economic growth was not associated with a corresponding increase in private sector debt. Indeed, before 2008, China’s economy was growing at an average rate of 8% per year, whilst private sector debt remained stable at around 100% of GDP. Accordingly, China escaped the financial crisis relatively unscathed, as China’s growth had not been accompanied by “an explosion of private debt”.

Consequently, China did not suffer internally from a debt overhang. Chinese spending did not have to be sacrificed in order to service and pay back debts. Unlike Western banks, Chinese banks did not have an overwhelming amount of non-performing loans on their balance sheet, making them unwilling to lend. Such a debt overhang however, did plague Western economies – which lead to a significant decline in demand for Chinese exports.

The other problem facing China, even before the 2008 crisis, was the steady decline in domestic consumption as a proportion of GDP. As a proportion of GDP, private consumption has fallen from 49% in 1990, to 45% in 2000, to 29% in 2011. China is increasing its productive output every year, but domestic demand for consumer goods is not growing along with it, so the consumption to GDP ratio is declining. Professor Yanis Varoufakis suggests that this is “A sure sign that the domestic market cannot generate enough demand for China’s gigantic factories”.

To ensure that the economy would keep growing above 7% per year, the Chinese put together an unprecedented stimulus package, designed specifically to boost domestic aggregate demand. With consumption and exports not showing any signs of increasing, the package was primarily aimed at stimulating demand by increasing domestic investment. The financing of this investment, roughly 85%, can be traced back to China’s banking sector.

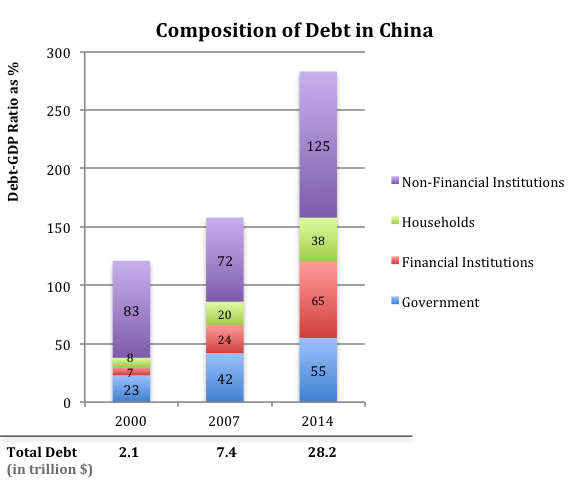

The result of the stimulus package was the rapid and vast accumulation of Chinese debt (public and private), which has grown from $7 trillion in 2007, to $28 trillion in 2014. As James Meadway, of the New Economics Foundation suggests:

“The Chinese Government response to the crisis then was to let borrowing rip, creating money on a huge scale and allowing all sorts of financial institutions, including local governments, the opportunity to borrow on a huge scale.”

Private Sector Debt

The relatively low level of private sector debt, high reserve ratios and high interest rates meant that China could afford to rapidly change levers and move into stimulus mode in 2008. By cutting interest rates and reducing reserve ratios, the stimulus package enticed the private sector into borrowing more; and banks were incentivised to extend new loans and create more money. Private sector debt skyrocketed after 2008, and has since nearly quadrupled in scale. As a percentage of GDP, private sector debt increased from 116% in 2007, to 228% in 2014.

To put this into perspective, China’s total private and public sector debt stood at $7.4 trillion in 2007. Yet between 2007-2014, private sector debt alone grew by $18.6 trillion to under $23 trillion (leaving total debt at £28 million). Professor Steve Keen notes that in 2010 alone the increase in Chinese debt was equivalent to 35% of GDP, which “Dwarfs the rate of growth of credit in both Japan and the USA prior to their crises: Japan topped out at just 25% per year, and the USA reached a mere 15% of GDP per year”.

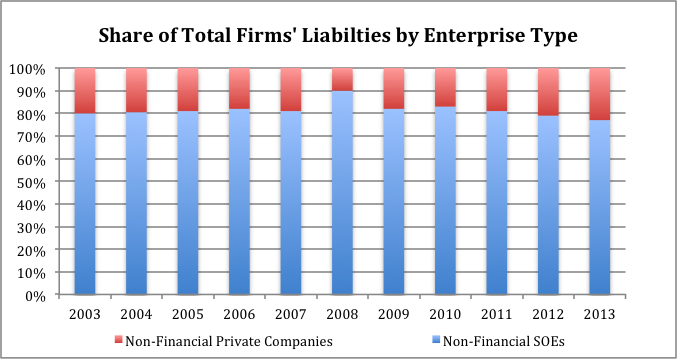

Deconstructing the figures for Chinese debt reveals that it is corporate debt, which has increased the most since 2008 – from 72% of GDP to 125% of GDP in 2014. The vast majority of this corporate debt (75-80%) actually comes from State Owned Enterprises (SOEs), primarily in the construction and real estate sectors (to a lesser extent mining and utility companies). In fact, according to an IMF Report (2015), since 2006 Chinese private firms have been steadily deleveraging. SOEs are not considered to be official government branches, and hence they fall under the private sector.

Government Debt

The initial central government stimulus package announced in 2008, amounted to around RMB 4 trillion. About 70% of this package was aimed at infrastructure projects, with RMB 1 trillion of re-construction of the Sichuan earthquake area, and an estimated RMB 1 trillion spent on developing high-speed railways (see table below).

Approximate Breakdown of Chinese RMB 4 Trillion Stimulus Package

Infrastructure2.87General Infrastructure1.50Reconstruction of Sichuan earthquake area1.00Rural area infrastructure0.37Technology & Environment0.58Technology & structural adjustment0.37Energy savings & emission reductions0.21Social Measures0.55Construction & renovation cheap houses0.40Social security & health0.15

But how was the public stimulus financed? Roughly 30% of it came directly from the central government, and the other 70% was financed through local governments. As local governments were prevented by law from borrowing money, they set up local government financing vehicles (LGFVs). This also allowed infrastructure to be financed without blowing up the Central Government’s headline budget. These LGFVs turned to banks to finance the infrastructure projects of local governments. Accordingly, it is estimated that RMB 2.8 million of the public stimulus package was financed by the new money created by private banks in the form of loans to LGFVs.

Money and Growth

The above suggests that while China has grown since 2008 (like many other countries prior to the 2007 financial crisis) this growth has been primarily fuelled by bank lending. Lending and new money creation for growth is not necessarily problematic. However, lending and new money creation that doesn’t lead to growth, that tends to prompt asset price inflation and asset bubbles, can be particularly problematic. New lending has increased at about 35% of GDP per year; this suggests that the amount of new lending required to generate a unit of GDP growth has steeply risen.

But what explains this growing inefficiency of lending? The answer essentially lies in how loans are used.

Nearly half of China’s debt is in one way or another related to the Chinese property market. On the one hand, as the original stimulus package had intended, economic activity was boosted. China for example poured more concrete from 2011-2013, than the USA from 1901-2000. As Meadway points out, “That meant jobs in construction and demand for concrete and steel”.

On the other hand, this has led to vast speculation in the real estate and triggered an asset bubble in the property market. State owned enterprises (SOEs) and to a lesser extent households, took out new loans to purchase property and invest in real estate, with the expectation of getting higher returns. However, SOEs are evaluated on the basis of their ability to produce growth. Thus, they had the added incentive of borrowing money from banks in order to develop real estate – so that they could help reach growth targets.

As more new money was created for speculative purposes, an ‘artificial’ level of demand was being signalled to the market, and property prices skyrocketed. For example:

“An index of prices in 40 Chinese cities rose by 60 percent from 2008 to August 2014; prices rose in Shenzhen by 76 percent and in Shanghai by 86 percent. Residential property prices in prime locations in Shanghai are now only about 10 percent below levels in New York and Paris.”

As a result of the property bubble, China now has a number of ghost cities, where “whole towns built speculatively that now stand empty”. One statistic suggests that there are over 50 million housing units are privately owned but lay vacant. Another suggests 42% of demand for property comes from speculators who already own property.

The Stock Market Bubble

After four years of languishing, the Chinese stock market began to take off in the summer of 2014. By spring of 2015, the Shanghai Composite index was more than twice of what it had been the year before. One estimate suggests that price to earnings ratios for Chinese stocks averaged 70:1, compared to a global average of 18:1.

There are a variety of reasons for the recent stock market bubble. One common explanation is that once the property market started cooling in 2013, investors and speculators moved their money out of property and into the stock market. Indeed, with 40% of bank loans secured with property as collateral, it is very likely that property is being used as collateral to acquire loans for investing in the stock market.

However, the above is perhaps an oversimplified explanation of the Chinese stock market bubble. In the face of a slowing economy and increasing debt, it is more likely that the government made a concerted effort to boost the stock market to help heavily indebted SOEs acquire new capital to pay off outstanding loans. As Derek Scissors, an economist at the American Enterprise Institute suggests, the Chinese government thought “Hey, why not address our huge problems by replacing debt with equity?”.

In order to funnel more money into the stock market and increase prices, the government has reduced the reserve ratio of banks 4 times and lowered interest rates 5 times in the last year. It has also invoked more lax standards for margin lending, allowed pension funds to invest 30% of their assets in equities, and forced a number of SOEs to purchase stocks whilst preventing them from selling any.

While the Chinese stock market has taken a massive dive since June, it is important to note that equities still play a very small role in the Chinese economy, and are far less influential than in Western markets. Also, as Deloitte notes: “…though the market has plunged since June, it is only back to March levels. Anyone who invested in Chinese equities a year ago would have more than doubled their money.”

This is not to say that all is well with the Chinese economy, however, it does suggest caution is warranted when panicking specifically about the recent Chinese stock market plunge. A much greater cause for concern is the huge build-up of Chinese debt and how it used – for which the stock market bubble is more likely a corollary.

Conclusion

To fully understand what is happening in China it is necessary to look at how banks create new money and how this new money is used. Local government agencies and SOEs are primarily assessed on their ability to generate economic growth. This incentive structure has prompted SOEs and local governments to borrow increasing amounts of money from banks in order to hit short-term growth targets. Accordingly, “…incentives are more aligned with investing heavily than they are with investing productively, leading to overinvestment and over indebtedness”. Lower interest rates and reserve ratios, combined with the moral hazard generated by an unspoken guarantee of banks to provide loans, stand behind this misaligned incentive structure.

The recent stock market bubble seems more like a symptom of the increasing mountain of debt used to prop up Chinese growth, rather than the cause of any breakdown in the real economy. More likely, it is the vast amount of debt used unproductively that will be the cause for concern moving forwards. China is clearly going to need to strike a delicate balance between maintaining growth, relying less on exports, and reducing its dependence on debt.