Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

28 April 2014

The debate on money reform goes mainstream

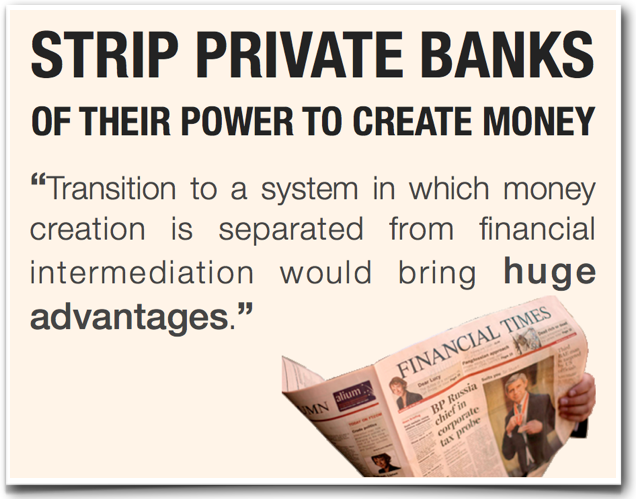

Martin Wolf’s recent article in the Financial Times has sparked a major debate in the mainstream media.

Martin Wolf’s recent article in the Financial Times has sparked a major debate in the mainstream media. The article discusses the nature of money and credit in the modern monetary system in which he suggests: “strip private banks of their power to create money”. There has been a significant backlash from critiques and many misunderstandings. But it is fantastic that this issue is finally getting attention and is being debated.

We’ll respond individually to the criticisms and misunderstandings. Now, here’s an overview of the latest articles – by the economists Paul Krugman, Ann Pettiffor, Warren Mosler and FT Alphaville reporter Izabella Kaminska:

Paul Krugman, American economist, the Nobel Laureate in Economic Sciences, Professor of Economics and International Affairs at the Woodrow Wilson School of Public and International Affairs at Princeton University, Centenary Professor at the London School of Economics, and an op-ed columnist for The New York Times.

OK, a genuinely interesting debate on financial reform is taking place. I’m not even sure where I stand. But it’s certainly worth talking about.

Atif Mian and Amir Sufi draw our attention to proposals to either mandate or create strong incentives for 100-percent reserve banking, coming from Martin Wolf and, more surprisingly, John Cochrane.

Wolf, unless I’m reading him wrong, seems to identify the whole issue with one particular form of short-term debt — bank deposits. This seems an oddly narrow view given the nature of the 2008 crisis, which involved very few runs on deposits but a massive run on shadow banking, especially repo — overnight lending that in a fundamental sense fulfilled the functions of deposit banking but also created the same kind of risks.

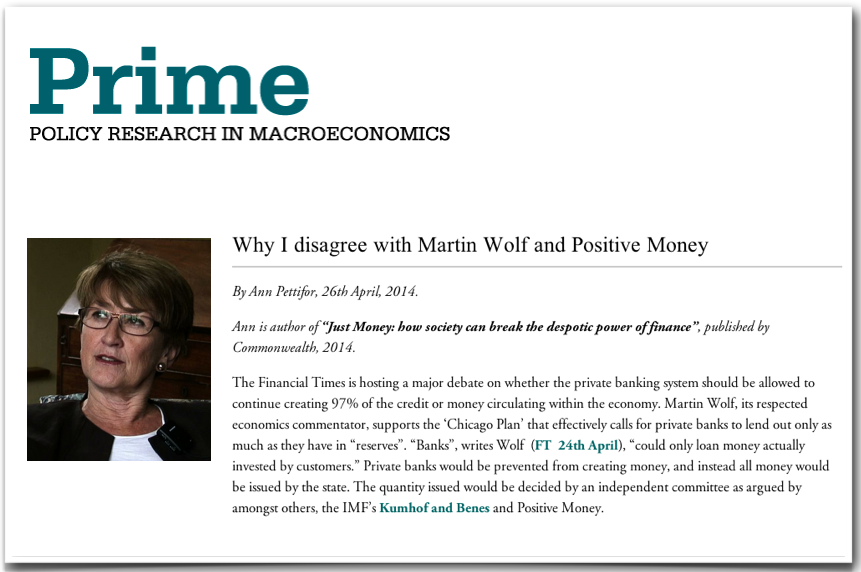

Ann Pettifor, Director of Policy Research in Macroeconomics (PRIME), Honorary Research Fellow at the Political Economy Research Centre at City University (CITYPERC) and a fellow of the New Economics Foundation, London.

Why I disagree with Martin Wolf and Positive Money

Because of the finance sector’s despotic power, about which I have been very vocal, many readers would expect me to support a proposal that prevents private banks from creating money, and to enthusiastically back the nationalization of money issuance. I do not however, and want to explain why.

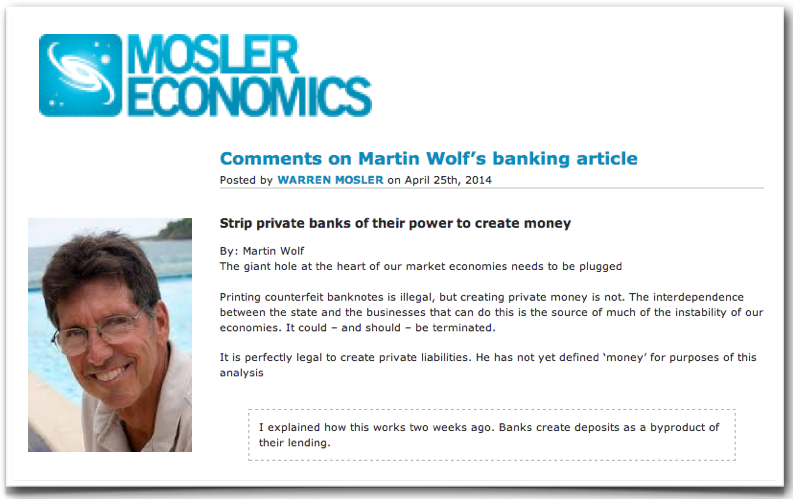

Warren Mosler, American economist and theorist, president and founder of Mosler Automotive, and co-founder of the Center for Full Employment And Price Stability at the University of Missouri-Kansas City.

Comments on Martin Wolf’s banking article

Yes, a 100% capital requirement, for example, would effectively limit lending. But, given the rest of today’s institutional structure, that would also dramatically reduce aggregate demand -spending/sales/output/employment, etc.- which is already far too low to sustain anywhere near full employment levels of output.

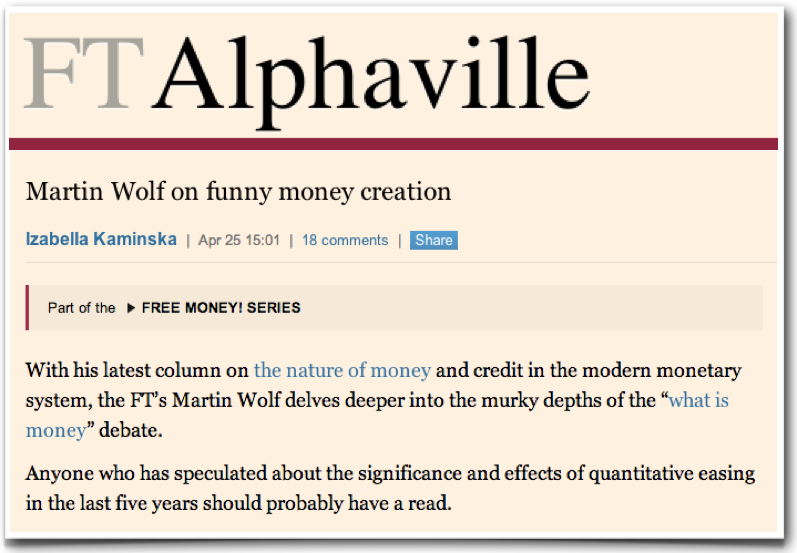

Izabella Kaminska, financial reporter at FT Alphaville discusses the issues in two articles:

Martin Wolf on funny money creation

With his latest column on the nature of money and credit in the modern monetary system, the FT’s Martin Wolf delves deeper into the murky depths of the “what is money” debate.

Anyone who has speculated about the significance and effects of quantitative easing in the last five years should probably have a read.

In the piece, Wolf comes out in favour of the endogenous theory of money supply and explains why it is that banks, through their power to issue private money directly, influence the economy in a very different way than is traditionally accepted.

On the elimination of privately issued money

As Martin Wolf has eloquently argued this week, yes, there is a clear-cut and urgent need for state e-money issuance.

But the case for expanding the central bank balance-sheet to the population — something which can easily be done via the issuance of sovereign e-money — does not in our opinion necessarily demand the elimination of private money issuance along with it. More than likely both forms of money can co-exist quite healthily.

We’ll respond individually to the criticisms and misunderstandings. In the meantime, most of them are covered briefly in our Frequently Asked Questions, e.g.:

Is Positive Money reform proposal the same idea as “monetarism” in the 1980s?

Wouldn’t these reforms make it difficult for banks to lend?

How will the reforms affect the Business loans?

Why so radical? Surely regulation is the answer?

What is the problem with debt? …Debt can be a good thing…

Isn’t the idea of a Money Creation Committee still very much open to corruption?

Isn’t the Money Creation Committee just a way of giving power to a group of unelected bureaucrats?