Back to Archive![12 highlights from 2022]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

![PositiveMoney - Post]()

12 February 2013

Adair Turner: “Debt, Money and Mephistopheles: How do we get out of this mess?”

On the 6th of February, the chairman of the FSA, Adair Turner, gave a speech at Cass Business School, entitled “Debt, Money and Mephistopheles: How do we get out of this mess?” The subject of the speech was the way in which the economy might be brought out of recession.

On the 6th of February, the chairman of the FSA, Adair Turner, gave a speech at Cass Business School, entitled “Debt, Money and Mephistopheles: How do we get out of this mess?” The subject of the speech was the way in which the economy might be brought out of recession.

The following post is merely the author’s attempt to pick out some of the key points of Turner’s speech, and provide a brief commentary where required. It is not an analysis, and neither should it be taken that Positive Money agrees with all of what Turner is saying. Instead, the sole purpose of this post is to distill Turner’s 46-page speech into something a little more manageable, and in particular to highlight his thoughts on Overt Monetary Financing (OMF), which is in short creating money and spending it into circulation. If this sounds familiar, it’s because Positive Money has been advocating something similar since June 2010!

The speech actually details a whole range of other types of intervention, and is well worth reading for those who have the time (available here, watch the speech here)

Turner’s speech starts by noting that for monetary policy to achieve a specific target (e.g. growth, or low and stable inflation, or low unemployment, etc.) the correct tool is required:

“The question is by what means can we and should we seek to stimulate or constrain aggregate nominal demand. Before the crisis the consensus was that conventional monetary policy, operating through movements in the policy rate and thus effecting the price of credit/money, should be the dominant tool, with little or no role for discretionary fiscal policy and no need for measures focused directly on credit or money quantities. Post-crisis, a wide spectrum of policy tools is already in use or under debate.”

One such tool is: “overt money finance (OMF) of fiscal deficits – “helicopter money”, permanent monetisation of government debt.” Turner points out that such a policy was proposed by Milton Friedman in his 1948 paper, “A Monetary and Fiscal Framework for Economic Stability”:

“As the title implies, one of his concerns was which fiscal and monetary arrangements were most likely to produce macroeconomic stability – meaning a low and predictable rate of inflation, and as steady as possible growth in real GDP. He was also concerned with financial stability, which he perceived as important per se and because of its effects on wider economic stability.

His conclusion was that the government should allow automatic fiscal stabilisers to operate so as “to use automatic adjustments to the current income stream to offset at least in part, changes in other segments of aggregate demand”, and that it should finance any resulting government deficits entirely with pure fiat money, conversely withdrawing such money from circulation when fiscal surpluses were required to constrain over buoyant demand.

Thus he argued that, “the chief function of the monetary authority [would be] the creation of money to meet government deficits and the retirement of money when the government has a surplus”. Friedman argued that such an arrangement – i.e. public deficits 100% financed by money whenever they arose – would be a better basis for stability than arrangements that combined the issuance of interest bearing debt by governments to fund fiscal deficits and open market operations by central banks to influence the price of money.”

An important assumption in Friedman’s analysis, however, is that:

“all money is base money, i.e. that there is no private money creation … This in turn is because in Friedman’s proposal there are no fractional reserve banks. In Friedman’s proposal indeed, the absence of fractional reserve banks is not simply an assumption, but an essential element, with Friedman arguing for “a reform of the monetary and banking system to eliminate both the private creation and destruction of money and discretionary control of the growth of money by the central bank”.

This is, of course, the Positive Money proposal. Turner continues:

“Friedman thus saw in 1948 an essential link between the optimal approach to macroeconomic policy (fiscal and monetary) and issues of financial structure and financial stability. In doing so he was drawing on the work of economists such as Henry Simons and Irving Fisher who, writing in the mid-1930s, had reflected on the causes of the 1929 financial crash and subsequent Great Depression, and concluded that the central problem lay in the excessive growth of private credit in the run up to 1929 and its collapse thereafter… made possible by the ability of fractional reserve banks simultaneously to create private credit and private money”.

The ability for private banks to create money makes the current banking system inherently unstable. As Henry Simons, one of the original authors of the Chicago Plan (which the Positive Money proposals are based on) put it:

“in the very nature of the system, banks will flood the economy with money substitutes during booms and precipitate futile efforts at general liquidation afterwards”. He therefore argued that “private institutions have been allowed too much freedom in determining the character of our financial structure and in directing changes in the quantity of money and money substitutes”.

As Turner explains, this leads to a great paradox – one of the father figures in the Chicago school of economics, Henry Simons, “believed that financial markets in general and fractional reserve banks in particular were such special cases that fractional reserve banking should not only be tightly regulated but effectively abolished.”

Turner does not agree that the current banking system should be abolished, arguing that a) debt contracts have arisen naturally as a way of fulfilling human desires, and b) that the current banking system allows maturity transformation which is economically beneficial. As this post is merely an outline of the points Turner raises in his paper we will not delve too deeply into the counterarguments to his points, other than to note that both debt contracts and maturity transformation are possible under the Positive Money proposals (as well as the Chicago Plan), and as a result these are not grounds for rejecting monetary reform.

Moving on, in the next part of his speech Turner argues that: “The financial crisis of 2007 to 2008 occurred because we failed to constrain the financial system’s creation of private credit and money; we failed to prevent excessive leverage.” This is of course also the Positive Money explanation of the crisis, which derives directly from the work of economists such as Hyman Minsky.

Turner then goes on to point out that since the crisis banks are making new loans less quickly than old loans are being repaid, both as a result of banks not wanting to make new loans and also due to a lower demand for new loans from the private sector. This in turn:

“depresses both asset prices and nominal private demand, threatening economic activity and income, and making it more difficult for firms and individuals actually to achieve desired deleveraging. Such an attempted deleveraging was as Irving Fisher argued fundamental to the process by which the financial crisis of 1929 turned into the Great Depression. And as Richard Koo has argued, it is core to understanding the drivers of Japan’s low real growth and gradual price deflation over the past two decades.”

In Koo’s persuasive account, Japan from 1990 suffered a “balance sheet recession” in which the dominant driver of depressed demand and activity was private sector (and specifically corporate sector) attempts to repair balance sheets left overleveraged by the credit boom of the 1980s. In such “balance sheet recessions” Koo argues, the reduction of interest rates … has very limited ability to stimulate credit demand since firms’ financing decisions are driven by balance sheet considerations. As a result, Koo argues, economies in a deleveraging cycle will face deep recessions unless governments are willing to run large fiscal deficits…”

So while the Japanese experience would have been much worse without these deficits, they do not actually reduce the overall level of debt in an economy, instead they simply shift it from the private sector to the public sector. The problem is that public sector debt can also have negative effects if it gets too large, limiting the potential effectiveness of government spending financed by borrowing. As Turner notes:

“Post-crisis deleveraging, while essential for long-term financial stability, thus creates an immensely challenging macroeconomic environment.

Monetary policy acting through short or long term interest rates loses stimulative power.

Fiscal policy offsets may be constrained by long-term debt sustainability concerns.

And slow growth in nominal GDP makes it more difficult to achieve attempted deleveraging in the private sector, or to limit the growth of public debt as a % of GDP.

The danger in this environment is that other countries could suffer not just a few years of slow growth, but the sustained decades of slow growth and rising public debt burdens which Japan has suffered. It is in this environment that we have to consider the two questions posed earlier.

What are the appropriate targets of macroeconomic policy?

And what policy tools should we use to achieve them?”

In the next section of the speech Turner argues that it may be desirable to target some combination of growth and price changes with monetary policy (unlike the case today, where only the change in the price level (i.e. the inflation rate) is explicitly considered).

Moving on to look at the response to the crisis, Turner notes that:

“All of the policy levers [low interest rates, QE, funding for lending etc]… work through interest rate, credit and asset price channels. In different ways they induce agents to change behaviour – by substituting money for bonds: by reducing medium and long-term interest rates and stimulating a search for yield: by directly or indirectly reducing the cost of credit supply: or by enabling banks to supply a higher quantity of credit as a result of lower capital or liquidity ratios.

But the effectiveness of each of these transmission channels may be constrained if post-crisis deleveraging produces the “balance sheet recession” behaviours described by Richard Koo in Japan.”

In addition, Turner makes the point that many of the current policy levers have possible negative side effects. As well as potentially increasing the probability of complex forms of speculation and creating ‘beggar thy neighbour’ policies through their effects on the exchange rate, most of these policies can only increase demand if they incentivise the private sector to go further into debt. Yet:

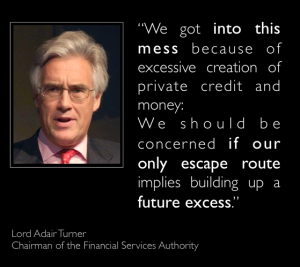

“We got into this mess because of excessive creation of private credit and money: we should be concerned if our only escape route implies building up a future excess.”

In short, he is saying that you can’t solve a debt crisis brought on by people being overly indebted, by getting the very same people to go further into debt. Thus:

“An exclusive reliance on monetary, credit subsidy, and macro-prudential policy levers to stimulate nominal demand thus carries significant long-term risks – a danger that, in seeking to escape from the deleveraging trap created by past excesses, we may build up future vulnerabilities”

With the current set of monetary tools unlikely to have the desired impact on growth, Turner looks at alternative measures to stimulate the economy (i.e. government spending/tax cuts). As he puts it:

“The argument for fiscal stimulus is that it operates in a more direct fashion, cutting taxes or increasing public expenditure, putting spending power directly into the hands of individuals or businesses.”

However, if public levels of debt are already high, then this increase in government spending may not be as effective as it otherwise might be. The answer, Turner contends, is “overt money finance” (OMF). OMF (as outlined by Ben Bernanke in a 2003 speech, “Some thoughts on monetary policy in Japan”) would work in the following way:

“He proposed “a tax cut for households and businesses that is explicitly coupled with incremental BoJ purchases of government debt, so that the tax cut is in effect financed by money creation”

He suggested that it should be made clear “that much or all of the increase in the money stock is viewed as permanent”

He argued that consumers and businesses would likely be willing to spend their tax cut receipts since “no current or future debt service burden has been created to imply future taxes”…

And he argued that the policy would likely produce a fall in the Japanese government debt to GDP ratio, since the nominal debt burden would remain unchanged while “nominal GDP would rise owing to increased nominal spending”

And while his main illustrative proposal was for a tax cut, he noted that the same principle of a money financed fiscal stimulus “could also support spending programs, to facilitate industrial restructuring, for instance””

Bernanke’s description of a money financed deficit thus makes clear its potential advantages over either pure monetary policy or pure funded fiscal deficits as a means of stimulating nominal demand:

Compared with the [other] monetary policy options … it is more direct and certain in its first order effect. Monetary, credit support, and macroprudential policy levers work through the indirect mechanism of stimulating changes in private sector borrower and investor behaviours, and may therefore be ineffective if behaviour is driven by deleveraging during a balance sheet recession”. OMF, because it finances an increased fiscal deficit, results in a direct input to what Friedman labelled “the income stream”. As Bernanke notes, this means “that the health of the banking sector is irrelevant to this means of transmitting the expansionary effects”, making concerns about “broken channels of monetary transmission” irrelevant.

But unlike the funded fiscal policy stimulus considered in Section 6, the stimulative effect of a money financed increase in fiscal deficit will not be offset by crowding out or Ricardian equivalence effects, since no new interest bearing debt needs to be publicly issued, and no increased debt burden has to be serviced in future.

As a result, OMF is bound to be at least or more stimulative than an increase in funded fiscal deficits. As Friedman put it in 1948 “the reason given for using interest bearing securities [i.e. for running a funded fiscal deficit] is that in a period of unemployment it is less deflationary to issue securities than to raise taxes. That is true. But it is still less deflationary to issue money.”

Essentially, therefore, OMF is a combination of fiscal and monetary policy levers; and the fiscal aspect of its character seems to make it quite distinct from QE which is unaccompanied by increased fiscal deficits and is intended to be reversed at some future date.”

Turner then points out that in fact QE, if it is never reversed, would be similar (but not identical) to OMF.

Of course, many would argue that government creation of money is bound to be highly inflationary. Turner addresses these points as follows:

“There is, moreover, no inherent technical reason (as against political economy reason) to believe that OMF will be more inflationary than any other policy stimulus, or that it will produce hyperinflation

It is no more inflationary than other policy levers provided the “independence” hypothesis holds. If spare capacity exists and if price and wage formation process are flexible, the impetus to nominal demand induced by OMF will have a real output as well as a price effect, and in the same proportion as if nominal demand were stimulated by other policy levers. Conversely if these conditions do not apply, the additional nominal stimulus will produce solely a price effect whether it is stimulated by OMF or by any other policy lever.

And the impacts on nominal demand and thus potentially on inflation will depend on the scale of the operation: a “helicopter drop” of £1bn would have a trivial effect on nominal GDP: a drop of £100bn a very significant effect and as a result create greater danger of inflation. And if the stimulative effect of OMF subsequently proved greater than anticipated or desired, it could be offset by future policy tightening, whether in the extreme form of Friedman’s “money withdrawing fiscal surpluses” or through the tightening of bank capital or reserve requirements.

The idea that OMF is inherently any more inflationary than the other policy levers by which we might attempt to stimulate demand is therefore without any technical foundation.”

Turner recognises however that while there are no technical reasons to believe that money creation will be inflationary if done right, there is the risk that governments will abuse their power and create too much money:

“But while the use of OMF is clearly technically compatible with sustained low inflation, there are strong political economy reasons for treating OMF as a potential poison, as Friedman recognised in his 1948 article:

“The proposal has of course its dangers. Explicit control of the quantity of money by government and the explicit creation of money to support actual government deficits may establish a climate favourable to irresponsible government action and to inflation”.”

As a result money creation has become somewhat a taboo subject, and the challenge is:

“therefore to take the possibility of OMF out of the taboo box, to consider whether and under what circumstances it can play an appropriate role, but to ensure that we have in place the rules and institutional authorities which would constrain its misuse.”

Of course, Positive Money explicitly recognises that the Government might be tempted to act irresponsibly with its money creation power, which is why in our reforms the decision over how much money is to be created (which is taken by a completely independent committee) is split from the decision over how the money is to be spent (which is taken by government). Turner himself comes to a similar conclusion, quoting Mervyn King (when he was governor of the Bank of England) as having said:

“it is important to distinguish between “good” and “bad” money creation. “Good” money creation is where an independent central bank creates enough money in the economy to achieve price stability. “Bad” money creation is where the government chooses the amount of money that is created in order to finance its expenditure”

Turner then goes on to point out that without OMF, decades of depression may result, and therefore: “Monetisation is not inherently evil, but a potentially necessary tool in these circumstances.” Looking at historical episodes, he then questions whether things would have been different if governments had thought to spend money into circulation:

“If Herbert Hoover had known in 1931 that OMF was possible, the US Great Depression would have been less severe.

If Germany’s Chancellor Brüning had known then that it was possible the history of Germany and of Europe in the 1930s might have been less awful. Hitler’s electoral breakthroughs from a 2.6% vote in the elections of May 1928 to 37.4% in the election of July 1932 were achieved against a backdrop of rapid price falls not inflation.

And while Japan’s deflationary experience of the last 20 years has been far less severe than that of the 1930s, (as a result, Koo argues, of fiscal deficits that were effective despite being funded) there is a very strong case that Bernanke was right and that if Japan had deployed OMF 10 or 15 years ago, it would be in a much better position today, with a higher price level, a higher level of real GDP, and a lower government debt burden as a % of GDP, but with inflation still at low though positive levels. And it is possible that there are no other policy levers that could have achieved this.”

Finally, he concludes with 9 points, which are worth reading in full:

“1. Leverage and the credit cycle matter a lot.

The level of leverage in both the real economy and the financial system are crucial variables which we dangerously ignored pre-crisis.

… future macro-prudential policy should reflect a judgment on maximum desirable levels of cross economy leverage, as well as on desirable growth rates of credit. A wide range of policy levers may be required to contain leverage.

2. Banks are different: the arguments for free markets – strong in other sectors of the economy – do not apply: private credit and money creation are fundamental drivers of both financial and macroeconomic instability and need to be tightly regulated.

3. Financial crises that result from excess leverage are followed by long periods of deleveraging which depress nominal demand, and which change fundamentally the context within which appropriate macro-demand policy must be designed and implemented.

4. In that context there is a good case for a temporary shift away from a pure inflation rate target: state contingent policy rules such as currently applied by the Federal Reserve, or a policy target which for a period of time takes account of nominal GDP growth rates or levels have attractions.

…. but simply changing the targets without also changing policy tools, may in some circumstances be insufficient to ensure optimal policy.

5. In a deleveraging cycle, monetary policy levers alone – whether conventional or unconventional – may be insufficiently powerful and / or have adverse longterm side effects for financial stability. If we got into this mess through excess private leverage we should be wary of escape strategies that depend on creating more private debt.

6. Fiscal multipliers are likely to be higher when interest rates are at the zero bound, and when monetary authorities are pre-committed to accommodative policy in future.

… but long term debt sustainability must be recognised as a significant constraint.

7. Governments and central banks together never run out of ammunition to create nominal demand: overt permanent money finance (OPMF) can always achieve that and is the only policy lever certain to do so.

… and in some circumstances OPMF may have fewer adverse side effects than the use of pure monetary policy levers (conventional or unconventional)

… and in technical terms OPMF carries no more inflationary risks than other policy levers.

8. But the political economy risks of OPMF are very great. … strong disciplines and rules are therefore essential to ensure that excessive use does not turn OPMF from a useful medicine to a dangerous poison.

… but such disciplines and rules, based on independent central bank judgement and clear inflation or other targets, can be designed.

9. We should therefore cease treating overt money finance as a taboo subject. … and if we continue to do so, we increase the danger that overt money finance may be deployed too late to be effective or safe, or deployed in an undisciplined fashion, increasing the long term risks to financial and macrostability.”

He finishes the paper by pointing out that Irving Fisher and Henry Simons correctly pointed out that:

“uncontrolled creation of bank credit and money can be a major driver of financial instability and subsequent economic harm, even when the creation of irredeemable fiat money is tightly controlled, with fiscal deficits small or non-existent and inflation low.

This suggests two conclusions:

First, that in the deflationary, deleveraging downswing of the economic cycle, we may need to be a little bit more relaxed about the creation, within disciplined limits, of additional irredeemable fiat base money.

But second, that in the upswing of the cycle we should have been massively more worried than we were pre-crisis about the excessive creation of private debt and private money; and, that we should be wary of relying on a resurgence of private debt and leverage as our means of escape from the mess into which excessive debt creation landed us.”