The most powerful committee of financial regulators in the world, the Basel Committee, are asking the public’s opinion on how banks should deal with climate change. The deadline to respond to their survey is Wednesday 16th February. There’s just one comment box to fill in on the survey. There’s more detail below, but if you want to respond quickly, here’s what we suggest:

> Say why you think that financial regulators should set tough rules for the biggest polluting banks. Personalising your response means we can have more impact collectively.

> We recommend including these key points, and we encourage you to write them in your own words:

-

- The Basel Committee should act decisively now to prevent both a financial crash and climate collapse.

- Financial regulators need to take an equitable approach, and address the financial causes, not just the consequences, of climate change.

- Financial regulators should use the tools available to them which are effective in changing banks’ behaviour.

- The Committee should follow recommendations from across civil society and implement a One-for-One rule for stability: https://www.finance-watch.org/wp-content/uploads/2021/11/One-for-One-Joint-letter-BCBS.pdf

Please note the comment box has a size limit of about 2KB, which is about 400 words. Longer comments can be uploaded as documents, using the “Choose File” button.

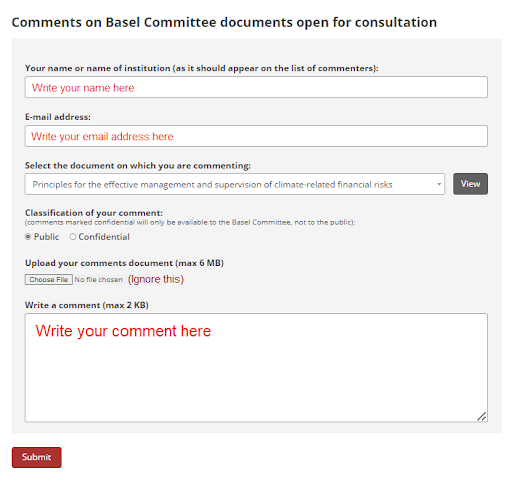

> This is what the survey page looks like. See instructions in red for submitting a short comment:

If you’d like to fill in the survey alongside others, and have a chance to ask more questions, we’re hosting a “response-writing Zoom workshop” on Tuesday between 5 – 6pm. We’ll talk through background information on the Committee, Consultation, and advise on how to respond. Click here to RSVP and we will send you a Zoom link.

Summary of the Positive Money research team’s response

The principles are a welcome step forward in addressing climate-related financial risks across jurisdictions for both supervisors and financial institutions. However, they do not adequately address the risks that they identify, therefore missing a pivotal opportunity to avert a climate-fuelled financial crisis.

As the principles focus entirely on the risk posed to individual financial institutions, BCBS fails to account for the macro-contribution of finance to the causes of climate change. In turn, the Committee will not address systemic risk through the application of these principles. This approach is not only ineffective but inequitable, as it will put the onus of responsibility for adapting to climate-related financial risk on climate-vulnerable countries, which are already facing severe losses without the available financial capacity to deal with them.

The Committee has recognised that climate-related financial risks are characterised by uncertainty, yet the principles propose using risk-based methodologies to identify and measure such risks before doing anything to address them. In other words, the principles encourage financial institutions and supervisors to wait and collect granular data before acting to change their behaviour. This does not operate on a timeline which follows the available climate science, and will contribute to higher transition and physical risks.

To effectively mitigate climate-related financial risks, the Committee should utilise Pillar 1 capital requirements. The use of higher capital requirements against fossil fuel exposures would have the dual effect of building sufficient capital buffers for an individual risk, and preventing the buildup of systemic risk by disincentivizing these investments. The Committee should follow recommendations from across civil society to introduce a One-for-One rule for stability: that every euro/dollar/ pound etc of financing provided to new fossil fuels must be matched by one euro/dollar/pound etc of financial institutions’ own funds. Where supervisors find that climate risk is excessively high, restrictions should be imposed on lending to certain categories of activities, in particular financing for new fossil fuel exploration and extraction.

_____________________________________________________________________________________

More background information

What is the BCBS consultation?

The Basel Committee on Banking Supervision (BCBS) is made up of central bankers and financial supervisors from the 28 most financially powerful countries in the world. It sets the international standards for how all major banks are regulated. Largely due to hard fought campaigns from across civil society, the BCBS has now recognised that the financial system is at risk of huge losses due to climate change. They have released a high level document, which will shape the decisions made by both banks and regulators in addressing climate risk. The BCBS wants to hear how their plan can be improved by the 16th February.

How can you make an impact with your response?

The BCBS will receive responses from banks with huge lobbying budgets all over the world, trying to stop substantial environmental regulation. However, since 2008, we have all become sharply aware that the decisions made by financial elites ultimately have painful impacts on our everyday lives. With the climate crisis already destroying so many lives and livelihoods, it’s more important than ever that as many members of the public as possible have our voices heard. There’s no need for expertise on financial regulation, and you only need to write an answer in the one comment box. Share why you think it’s important that banks be given strong rules to protect our planet.

What are the problems with the Basel Committee’s current proposed approach? What should it do instead?

Unfair: The principles recognise that climate change will cause losses for individual banks, but they do nothing to address how the financial system as a whole is contributing to climate change. Banks which are invested in climate destructive activities, such as the exploration and extraction of new fossil fuels, will not be required to change their behaviour. Instead, responsibility for coping with climate-risk will fall on vulnerable countries which have less financial capacity to shoulder the burden. The BCBS needs to adopt an equitable approach which confronts the financial causes, not just consequences, of climate change.

Low impact: The BCBS is planning to use complex financial modelling to predict the unpredictable, rather than using tools which have a proven track record of impact. Researchers are clear that the outcomes of climate change will be characterised by “radical uncertainty”, or, in other words, potentially catastrophic outcomes which are unpredictable in their nature. In this context, regulators need to use the tools available to them which have proven to be effective: require financial institutions to hold more capital against their investments in carbon intensive activities. Groups from across civil society are calling for the BCBS to introduce a One-for-One rule: that every euro/dollar/pound etc. of financing provided to new fossil fuels must be matched by one euro/dollar/pound etc. of banks’ own funds. Where the risks are particularly high, BCBS should also consider outright limits on lending to environmentally destructive activities.

Too slow: The longer regulators wait to act on climate change, the more climate risks will grow. As the principles encourage regulators to collect more data before taking meaningful action, they will create a false sense of security, and themselves contribute to a build up of systemic risk. Rather than waiting years for the collection of imperfect data, BCBS needs to encourage regulators to act now on the available data they do have.

Above is a summary of the Positive Money research and policy team’s submission. You can also read more explanation from our allies at Finance Watch and see their answer prompts.