Emotions have been a widely explored research topic during the last couple of decades. In the field of Design, it has been used as a tool to inspire designers to develop products or services that foster human flourishing. The Delft Institute of Positive Design (DIOPD), led by Pieter Desmet and Anna Pohlmeyer, is one of the most prolific research groups in this area. Along with them, I was able to start researching on the emotional impact of saving money.

I was already familiarized with saving money, together with my wife, we had designed a collection of piggy banks called ‘BILLEGAS’. However, it wasn’t until I read Cahit Guven that I started thinking about saving money in a different way, not only as a tool to increase wealth but also as a strategy to boost well-being.

Guven (2012) stated that happier people were able to save more money, implying that since happier people have more control with spending and consuming, they are less likely to be in debt. In addition, he posits that happier people are more concerned with the future and the decision-making process, therefore they can save more.

Guvens’ conclusions kept me thinking about the fact that happier people were more interested in saving money. But what if it would be the other way around: What if, by saving money, people would become happier? So, if you are reading this, take a few minutes to ask yourself if saving money makes you happy?

Money and happiness

The relation between money and happiness hasn’t been always the best. There have been interesting approaches to defining the relation between happiness and money, more precisely, between happiness and consumption. (for an overview, see Stanca and Veenhoven, 2015). For example, money could be seen as a resource to achieve something meaningful. One idea is that if you have money (and you know how to spend it), you could engage in activities that help boost your well-being. It is not about the amount you have, rather than how you use it (Dunn & Norton, 2013).

Imagine you want to travel to the Caribbean, either you have the money to go or not. So if you don’t, there are a couple of things you can do, one of them is saving.

So let’s dig a bit more into that. Saving money is a way in which we can increase wealth, buy things, invest, or save for retirement. However, saving money is challenging. We need to be fully motivated, have the proper saving tools, and have some saving strategies.

Happy Savings experiment

In order to understand some ideas about saving money behavior, I run a qualitative research using the Positive Design Framework proposed by Desmet and Pohlmeyer (2013). The framework states that if a product wants to contribute to human flourishing it should be pleasurable to use, promote the pursuit of personal goals, and encourage virtuous behavior.

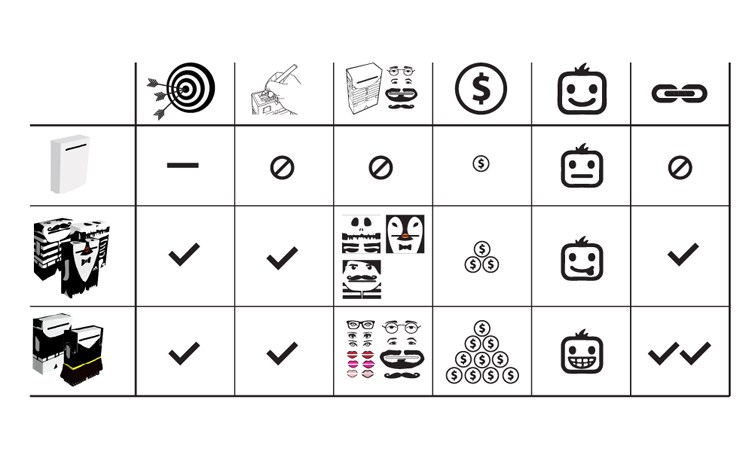

Under Pieter Desmet and Mafalda Casais’ supervision, we started a research that aimed to understand the role of design in contributing to saving money. We used the ‘BILLEGAS’ piggy banks as a case study, exploring different features of them. Including character creation, saving goal visualization and saving goal tangibility.

For the experiment, we asked fifteen participants to save money for three weeks in one of the piggy banks. There were three groups, each group with a different piggy bank:

In the first one, participants had a blank piggy bank and received no instructions to intervene in the piggy bank nor to choose a saving goal. In the second one, participants had a variety of BILLEGAS characters to choose from. they had to name their piggy bank and decide on a saving goal, which they had to write down. In the third one, participants had to create their own BILLEGAS piggy bank, give them a name and choose a saving intention. Along with the saving task, participants kept a diary to reflect upon their saving experience.

Effects of design Intervention on savings

Ownership and Appropriation

With this setup, we hypothesized that participants with a “stronger” link to the piggy bank, would be more motivated and committed to saving, and this would help them to meet their saving intentions.

Participants from the first group didn’t save much money, compared to the other groups. They claimed to feel no attachment to the piggy bank. Despite that, all intervene their piggy banks, even when we told them nothing about it. Most of them wrote their names claiming ownership. One of them wrote “Saving is Sexy” to enhance the piggy bank, but it didn’t make him save more money.

Another finding was how participants appropriated the piggy banks. Participants in group 3 created little avatars of themselves. This led to an interesting behavior, described as “mutual relationship” with the piggy banks, in which participants empowered it with the ability to take care of their savings, while they would “feed them” with money:

Ownership and appropriation strategies aimed to tackle the two types of happiness. The hedonic enjoyment was related to how people saved money by feeding the character. Changing the way they should collect their savings gave a higher meaning to the process. The eudemonia was related to bonding to the piggy bank by creating the character and setting a saving intention. The relationship created raised a sense of awareness and a feeling of having to take care of it, increasing a virtuous behaviour to the process of saving.

Outcome and overall feeling

This experiment allowed participants to experience a way to commit to their goals and save enough to accomplish them. One of the main reasons was the relation they forged with the piggy bank. Through embedding meaning on the piggy banks, participants felt engaged in saving money. Another important aspect was to have a tangible object that represented the saving goal. This helped to increase participants’ motivation, commitment, and money:

Even though the experiment was intended to withdraw qualitative insights, further studies could be run, on a larger scale, in order to find a quantitative relation between the findings and recommendations.

What’s next?

In the future, more ideas could be developed to improve the experience of saving money. For instance, exploring the ability to create saving networks, or the possibility to discover experiential value on future belongings. The concept of saving is incredibly powerful, because it allows us to savour, commit, gets disciplined, and make decisions according to the belongings/experiences we want to acquire. There is still a lot to do on how to improve how people save money. However, through design, the potential gains of saving can be amplified and made tangible, helping users to be more motivated to save money; it could also increase the level of commitment, engaging people in reflective processes about saving.

References

– Desmet, P. M., and Pohlmeyer, A. E. (2013) ‘Positive design: An introduction to design for subjective well-being’, International Journal of Design, 7, (3), pp.5-19.

– Dunn, E., and Norton, M. (2013) Happy money: The science of smarter spending. New York: Simon & Schuster.

– Guven, C. (2012). Reversing the question: Does happiness affect consumption and savings behavior?. Journal of Economic Psychology, 33(4), 701-717.

– Stanca, L., & Veenhoven, R. (2015). Consumption and happiness: Introduction to this special issue. International Review of Economics