The danger of allowing private banks to create money with no oversight was ruthlessly exposed in 2008, when unfettered credit expansion led to the worst financial crash this generation has ever seen.

When private banks have so much to gain from profit-making money creation, and so few checks and balances on that power, it’s easy to see how this system fails to serve the public interest. Wealth and prosperity become concentrated in the hands of those who have the power to create money from nothing, whilst investment flows primarily into activities that bear the most profit – regardless of risk or social utility.

Taking control of the money supply back into public hands therefore seems a sensible and rational way of making banks serve the public interest, as well as allowing for more transparency, scrutiny and accountability in that process.

Such a radical idea has the potential to revolutionise the banking system, and the society that that system is meant to serve. But revolutions rarely come easily, particularly when they seek to undermine the huge power, influence and vested interest of something so big and incumbent as today’s banking system. As a result, it’s imperative that we work in as many ways as possible to make banking work in the public interest in the current system in the interim.

One such way is the promotion of models of banking that act more ethically and sustainably – that is, they act in the interest of their stakeholders, the public. Such “stakeholder banking” is not new or even niche – indeed, stakeholder banking is prevalent across the developed world, from the USA to Germany, France to Japan.

Stakeholder banks are more accountable, less risky, and invest more productively. For example, across Europe stakeholder banks on average lend 66% of their assets into the real and productive economies, compared to only 37% from too big to fail shareholder banks.

In Britain, we face a huge current account deficit, a £6 billion yearly shortfall in credit for SMEs, and chronic centralisation of our economy in London and away from regional investment and local economic activity. As a result, it’s more than just an international anachronism that we do not have a stakeholder banking sector to speak of – it’s a complete travesty that is robbing the public of a safer, more sustainable and socially useful way of doing banking.

The tragic irony to all of this is that we already own a huge bank, which we bought at great expense – it’s called RBS, which is now worth only three fifths of what we paid for it. So why sell it back to the people that caused the crisis in the first place, unreformed and with the same structural disposition to create and allocate credit inappropriately and in service of private interests, when the UK is screaming out for public interest banking?

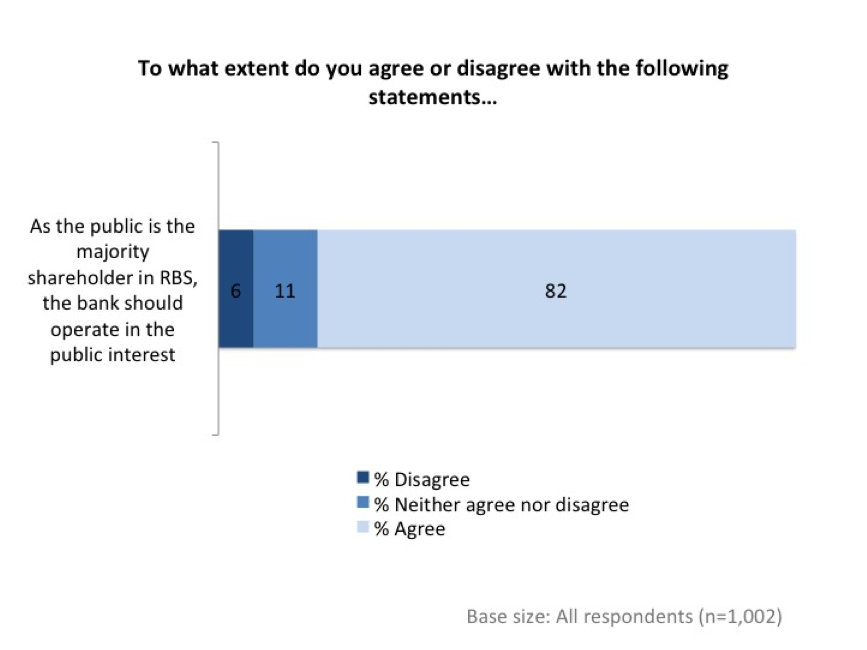

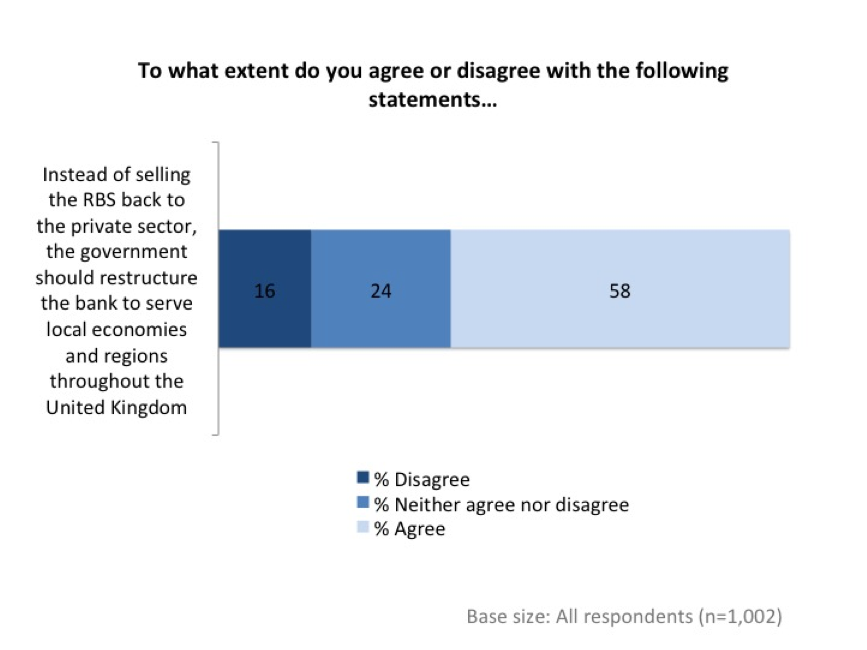

Indeed, recent polling research conducted for Move Your Money suggests that 82% of the public agree that RBS should work in the public interest, whilst 58% agree that the bank should be restructured to serve local and regional economies.

There is copious evidence that shows that this type of banking works in favour of society and the economy, what’s lacking is the political will to institute such reform – or even to undertake a formal assessment of all the options for the future of RBS. That’s why Move Your Money has launched a new campaign in favour of public-interest stakeholder banking, and arguing for a full, independent and public review into all the options for the future of RBS.

As we have seen time and time again, such drastic changes are unlikely to ever come to fruition on their own. Instead, they need the active participation and actions of committed members of the public to force these changes up the political agenda. Working on the local level to build political pressure, we’re helping communities to fight branch closures that boost private profits but abandon the public interest, whilst assisting others to organise locally to lobby their MPs for change.

So join us if you want to help make a bank that we already own work in the public interest, and to make RBS become the Royal Bank of Our Own.